Academic Profile

Statistics

Similar Authors

Papers on arXiv

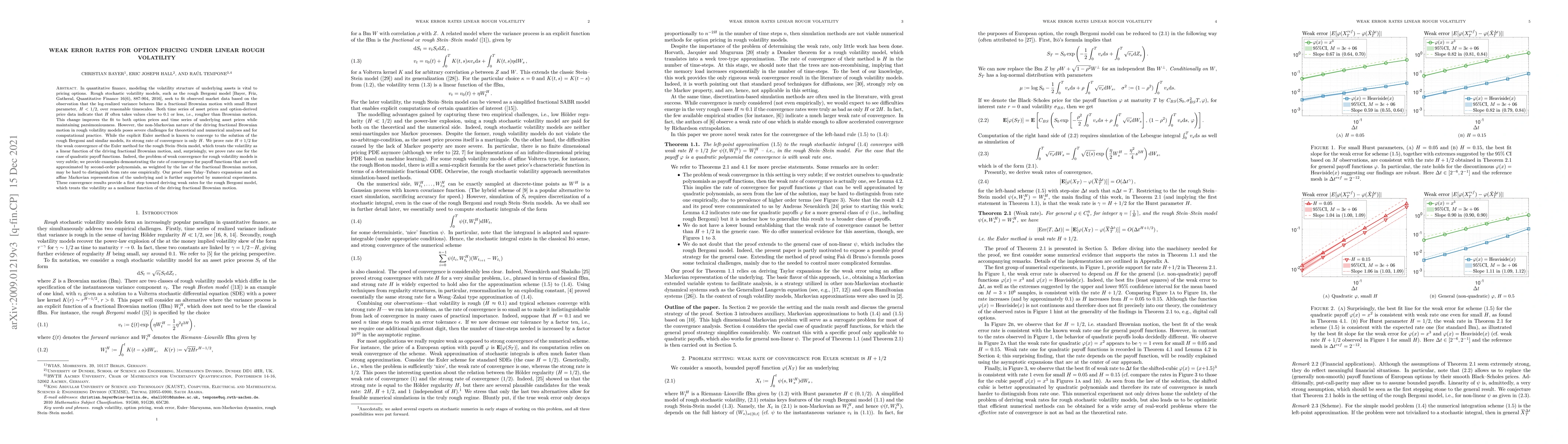

In quantitative finance, modeling the volatility structure of underlying assets is vital to pricing options. Rough stochastic volatility models, such as the rough Bergomi model [Bayer, Friz, Gathera...

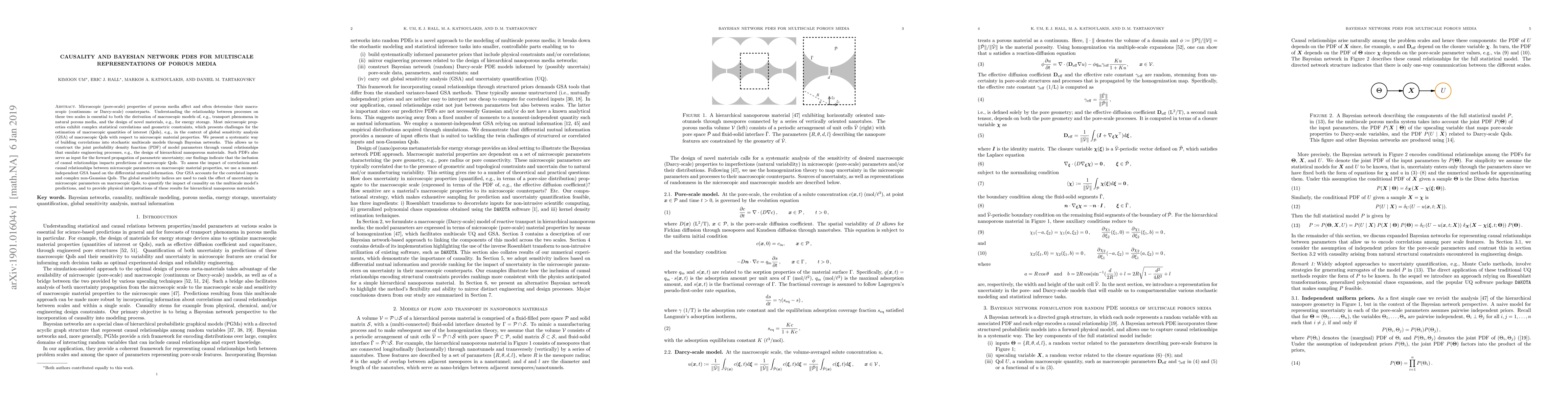

Microscopic (pore-scale) properties of porous media affect and often determine their macroscopic (continuum- or Darcy-scale) counterparts. Understanding the relationship between processes on these t...

We study adversarial learning when the target distribution factorizes according to a known Bayesian network. For interpolative divergences, including $(f,Γ)$-divergences, we prove a new infimal subadd...