Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper, we propose fitting unobserved component models to represent the dynamic evolution of bivariate systems of centre and log-range temperatures obtained monthly from minimum/maximum tempe...

In this paper, we survey recent econometric contributions to measure the relationship between economic activity and climate change. Due to the critical relevance of these effects for the well-being ...

In a globalised world, inflation in a given country may be becoming less responsive to domestic economic activity, while being increasingly determined by international conditions. Consequently, unders...

In this paper, we propose a computationally simple estimator of the asymptotic covariance matrix of the Principal Components (PC) factors valid in the presence of cross-correlated idiosyncratic compon...

We analyse economic growth vulnerability of the four largest Euro Area (EA) countries under stressed macroeconomic and financial conditions. Vulnerability, measured as a lower quantile of the growth d...

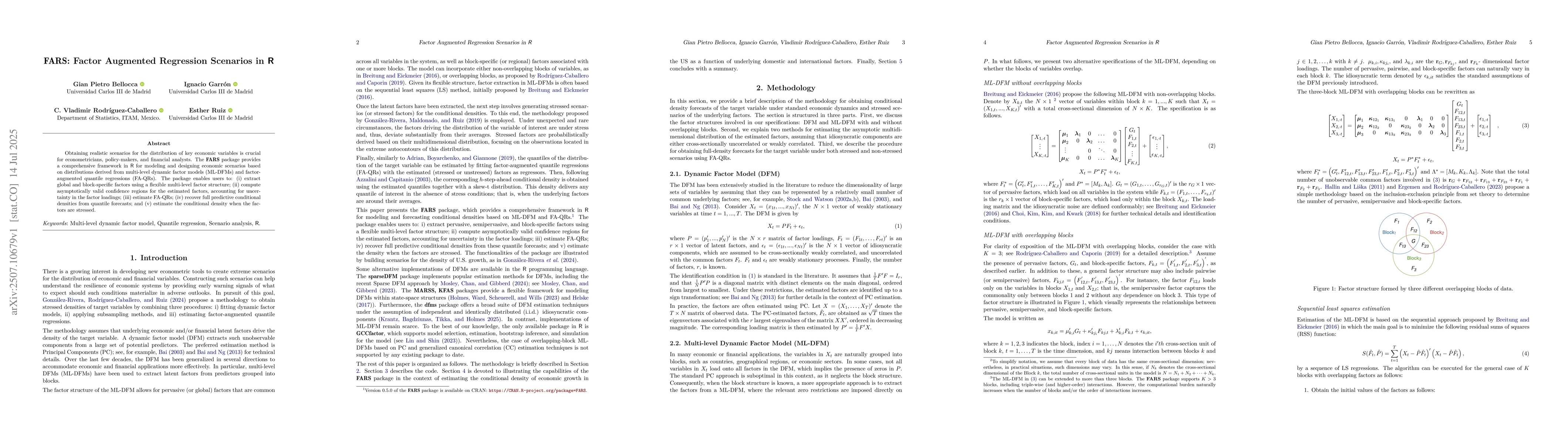

Obtaining realistic scenarios for the distribution of key economic variables is crucial for econometricians, policy-makers, and financial analysts. The FARS package provides a comprehensive framework ...

Factor extraction from systems of variables with a large cross-sectional dimension, $N$, is often based on either Principal Components (PC)-based procedures, or Kalman filter (KF)-based procedures. Me...

The research question we answer in this paper is whether the asymptotic distribution derived by Bai (2003) for Principal Components (PC) factors in dynamic factor models (DFMs) can approximate the emp...