Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper we study short-time behavior of the at-the-money implied volatility for Inverse and Quanto Inverse European options with fixed strike price. The asset price is assumed to follow a gene...

In this paper we study the short-time behavior of the at-the-money implied volatility for European and arithmetic Asian call options with fixed strike price. The asset price is assumed to follow the...

We consider the following stochastic heat equation \begin{equation*} \partial_t u(t\,,x) = \tfrac12 \partial^2_x u(t\,,x) + b(u(t\,,x)) + \sigma(u(t\,,x)) \dot{W}(t\,,x), \end{equation*} defined f...

In this paper we study the short-time behavior of the at-the-money implied volatility for arithmetic Asian options with fixed strike price. The asset price is assumed to follow the Black-Scholes mod...

We consider a real-valued diffusion process with a linear jump term driven by a Poisson point process and we assume that the jump amplitudes have a centered density with finite moments. We show uppe...

We aim at estimating the invariant density associated to a stochastic differential equation with jumps in low dimension, which is for $d=1$ and $d=2$. We consider a class of jump diffusion processes...

The purpose of this paper is extend recent results of Bonder-Groisman and Foondun-Nualart to the stochastic wave equation. In particular, a suitable integrability condition for non-existence of glob...

We study the following equation \begin{equation*} \frac{\partial u(t,\,x)}{\partial t}= \Delta u(t,\,x)+b(u(t,\,x))+\sigma \dot{W}(t,\,x),\quad t>0, \end{equation*} where $\sigma$ is a positive cons...

We study a continuous-time approximation of the stochastic gradient descent process for minimizing the expected loss in learning problems. The main results establish general sufficient conditions for ...

We consider the solution of an additive fractional stochastic differential equation (SDE) and, leveraging continuous observations of the process, introduce a methodology for estimating its stationary ...

We consider the stochastic partial differential equation, $\partial_t u = \tfrac12 \partial^2_x u + b(u) + \sigma(u) \dot{W},$ where $u=u(t\,,x)$ is defined for $(t\,,x)\in(0\,,\infty)\times\mathbb{R}...

Using Chen-Stein method in combination with size-biased couplings, we obtain the multivariate Poisson approximation in terms of the Wasserstein distance. As applications, we study the multivariate Poi...

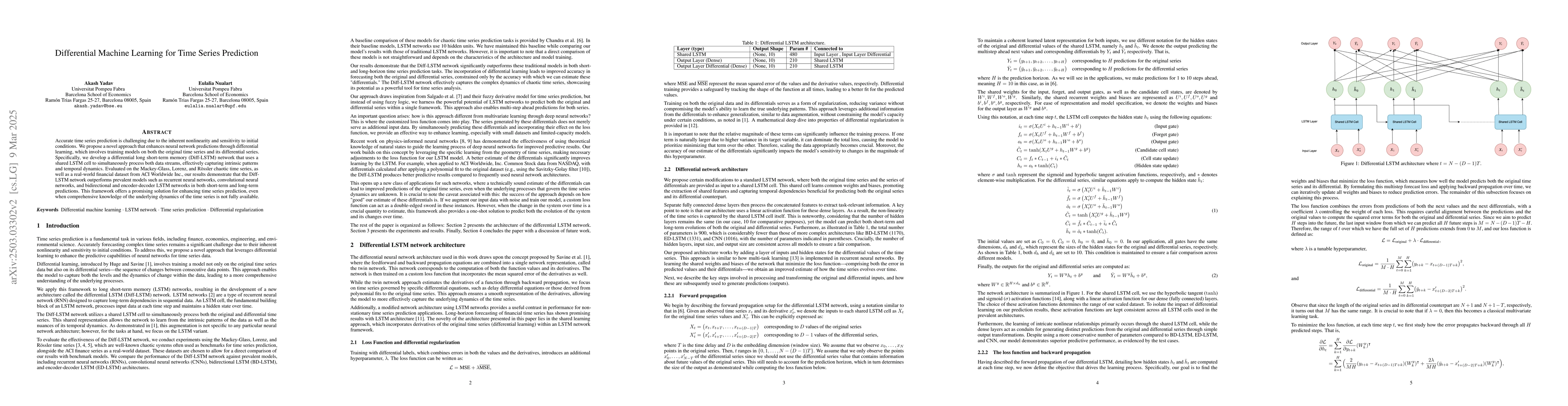

Accurate time series prediction is challenging due to the inherent nonlinearity and sensitivity to initial conditions. We propose a novel approach that enhances neural network predictions through diff...

We consider a parabolic stochastic partial differential equation (SPDE) on $[0\,,1]$ that is forced with multiplicative space-time white noise with a bounded and Lipschitz diffusion coefficient and a ...