Academic Profile

Statistics

Similar Authors

Papers on arXiv

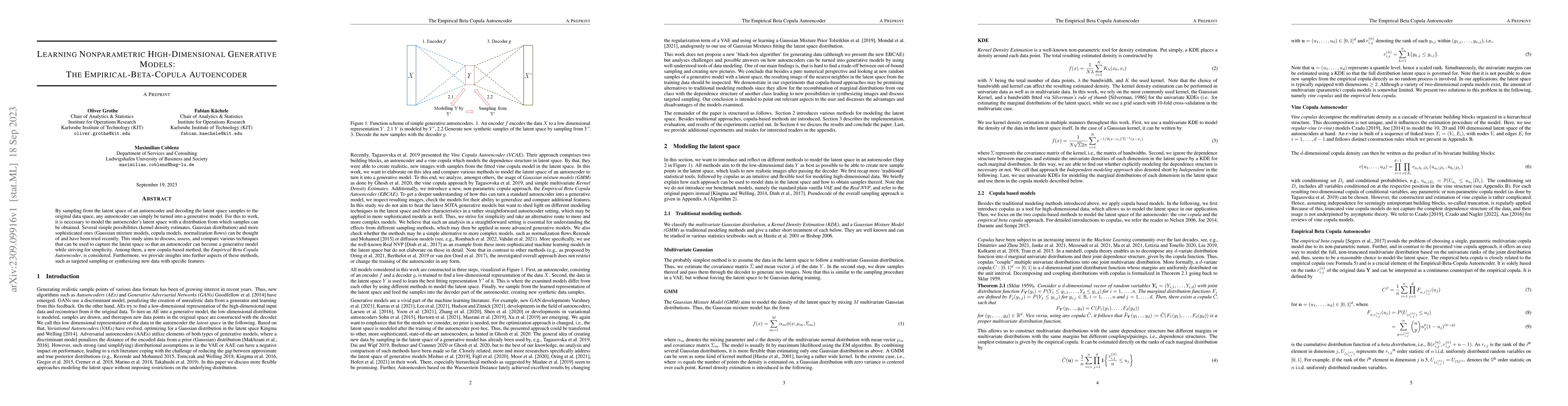

By sampling from the latent space of an autoencoder and decoding the latent space samples to the original data space, any autoencoder can simply be turned into a generative model. For this to work, ...

Modeling price risks is crucial for economic decision making in energy markets. Besides the risk of a single price, the dependence structure of multiple prices is often relevant. We therefore propos...

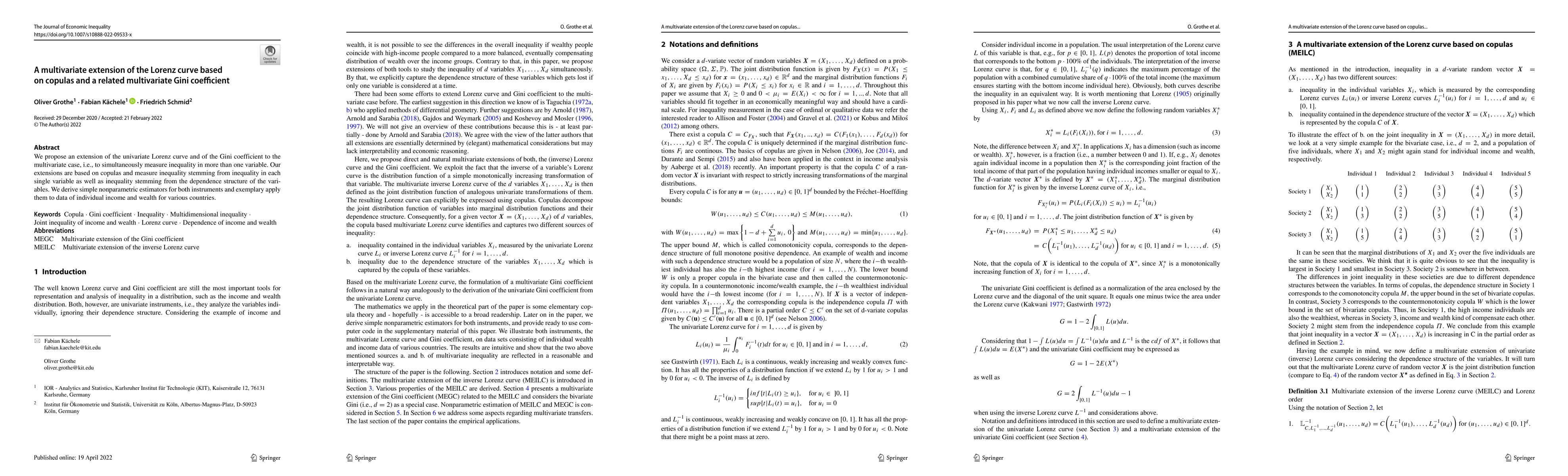

We propose an extension of the univariate Lorenz curve and of the Gini coefficient to the multivariate case, i.e., to simultaneously measure inequality in more than one variable. Our extensions are ...