Academic Profile

Statistics

Similar Authors

Papers on arXiv

In Bayesian inference, predictive distributions are typically in the form of samples generated via Markov chain Monte Carlo (MCMC) or related algorithms. In this paper, we conduct a systematic analy...

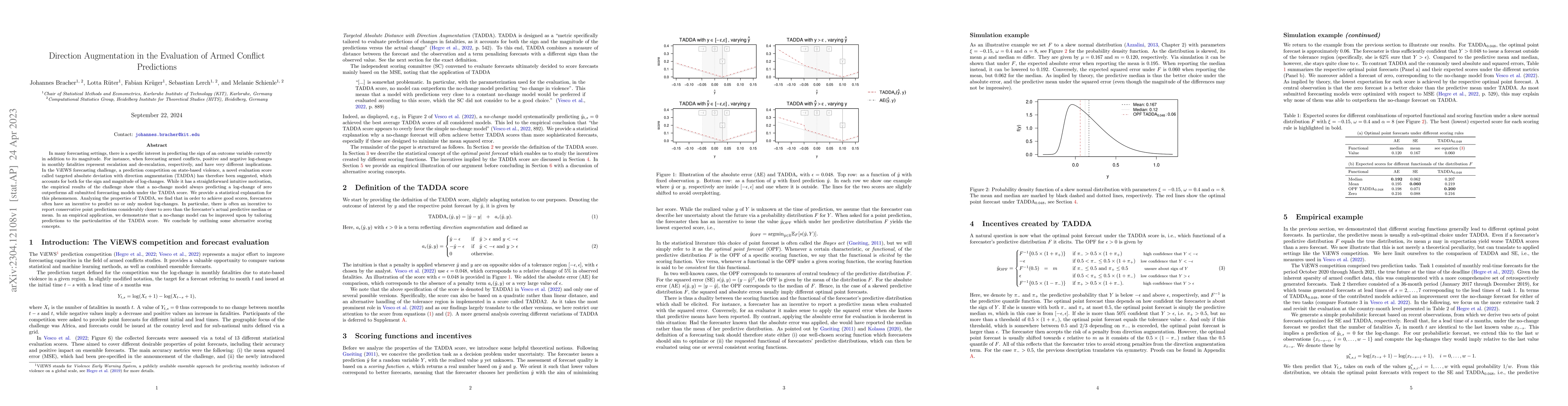

In many forecasting settings, there is a specific interest in predicting the sign of an outcome variable correctly in addition to its magnitude. For instance, when forecasting armed conflicts, posit...

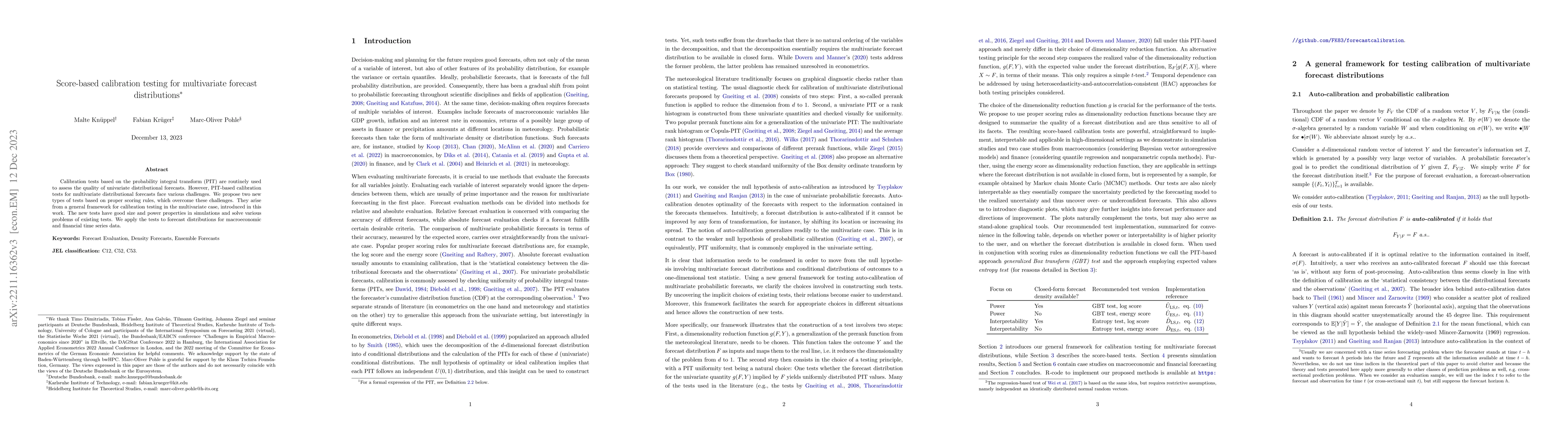

Calibration tests based on the probability integral transform (PIT) are routinely used to assess the quality of univariate distributional forecasts. However, PIT-based calibration tests for multivar...

We report on a course project in which students submit weekly probabilistic forecasts of two weather variables and one financial variable. This real-time format allows students to engage in practica...

The fixed-event forecasting setup is common in economic policy. It involves a sequence of forecasts of the same (`fixed') predictand, so that the difficulty of the forecasting problem decreases over...

Modeling price risks is crucial for economic decision making in energy markets. Besides the risk of a single price, the dependence structure of multiple prices is often relevant. We therefore propos...

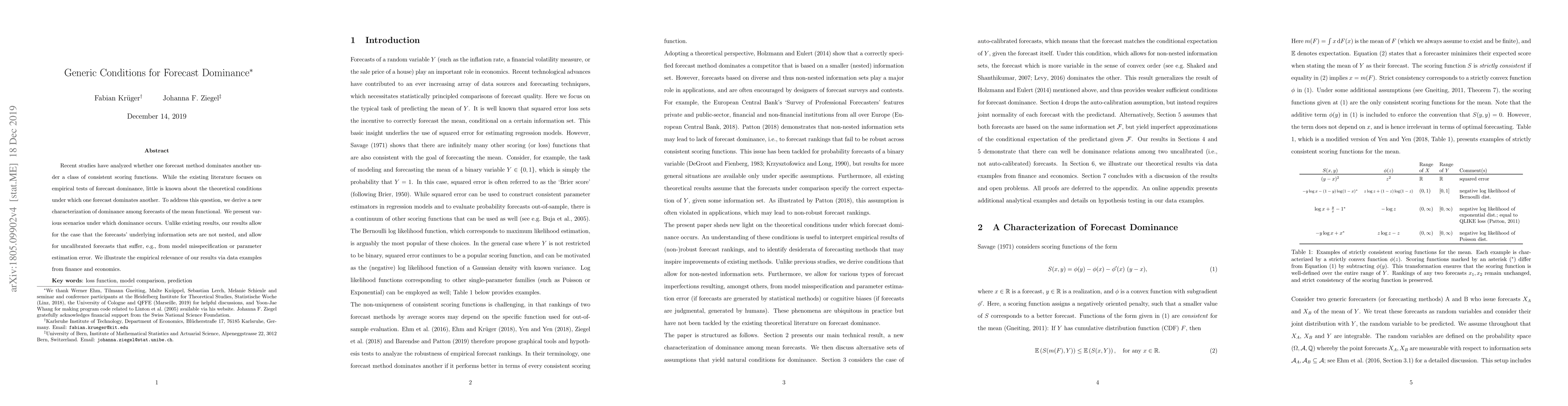

Recent studies have analyzed whether one forecast method dominates another under a class of consistent scoring functions. While the existing literature focuses on empirical tests of forecast dominan...

Since their introduction by Breiman, Random Forests (RFs) have proven to be useful for both classification and regression tasks. The RF prediction of a previously unseen observation can be represented...

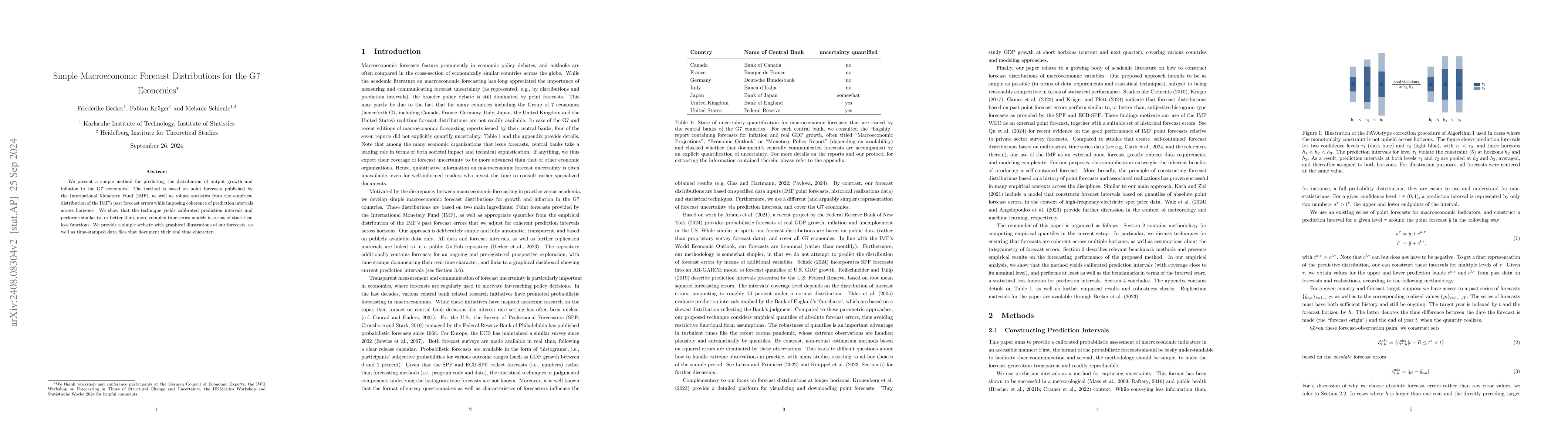

We present a simple method for predicting the distribution of output growth and inflation in the G7 economies. The method is based on point forecasts published by the International Monetary Fund (IMF)...

The variance of a linearly combined forecast distribution (or linear pool) consists of two components: The average variance of the component distributions (`average uncertainty'), and the average squa...