Academic Profile

Statistics

Similar Authors

Papers on arXiv

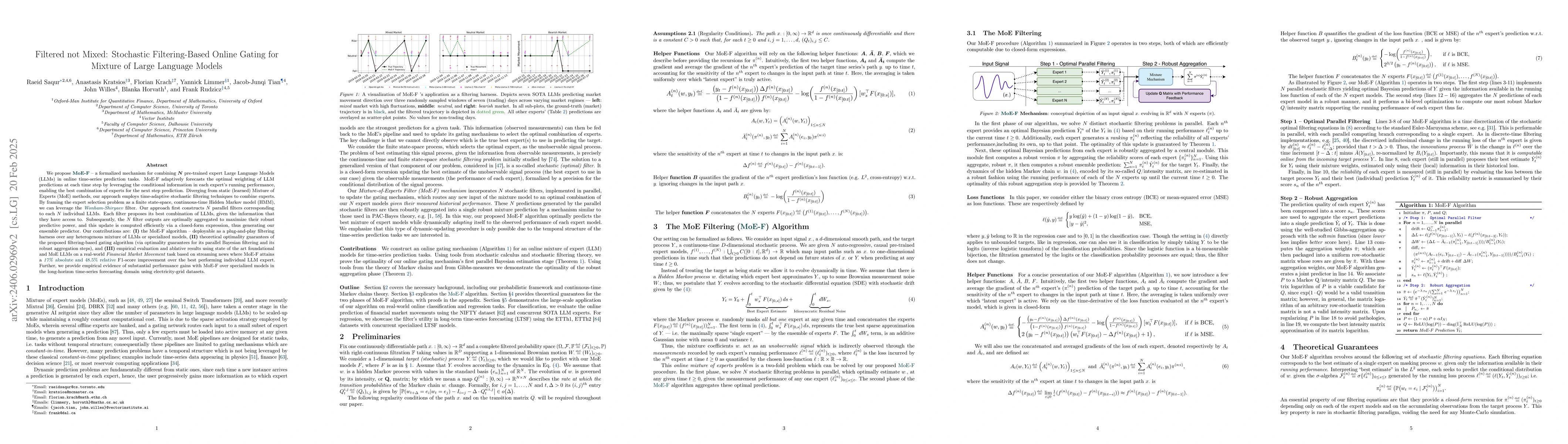

We propose MoE-F -- a formalised mechanism for combining $N$ pre-trained expert Large Language Models (LLMs) in online time-series prediction tasks by adaptively forecasting the best weighting of LL...

Robust utility optimization enables an investor to deal with market uncertainty in a structured way, with the goal of maximizing the worst-case outcome. In this work, we propose a generative adversa...

We propose an optimal iterative scheme for federated transfer learning, where a central planner has access to datasets ${\cal D}_1,\dots,{\cal D}_N$ for the same learning model $f_{\theta}$. Our obj...

The Path-Dependent Neural Jump Ordinary Differential Equation (PD-NJ-ODE) is a model for predicting continuous-time stochastic processes with irregular and incomplete observations. In particular, th...

This paper studies the problem of forecasting general stochastic processes using a path-dependent extension of the Neural Jump ODE (NJ-ODE) framework \citep{herrera2021neural}. While NJ-ODE was the ...

This paper presents the benefits of using randomized neural networks instead of standard basis functions or deep neural networks to approximate the solutions of optimal stopping problems. The key id...

The robust PCA of covariance matrices plays an essential role when isolating key explanatory features. The currently available methods for performing such a low-rank plus sparse decomposition are ma...

The Lipschitz constant is an important quantity that arises in analysing the convergence of gradient-based optimization methods. It is generally unclear how to estimate the Lipschitz constant of a c...

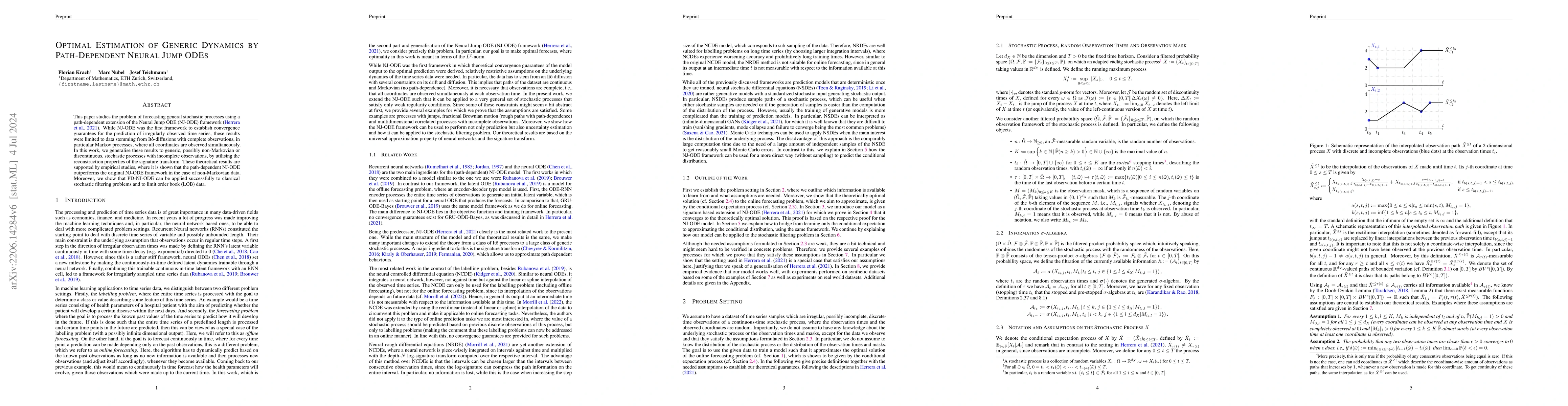

The Path-dependent Neural Jump ODE (PD-NJ-ODE) is a model for online prediction of generic (possibly non-Markovian) stochastic processes with irregular (in time) and potentially incomplete (with respe...

Neural Jump ODEs model the conditional expectation between observations by neural ODEs and jump at arrival of new observations. They have demonstrated effectiveness for fully data-driven online foreca...

Detecting anomalies in irregularly sampled multi-variate time-series is challenging, especially in data-scarce settings. Here we introduce an anomaly detection framework for irregularly sampled time-s...

In this work, we explore how Neural Jump ODEs (NJODEs) can be used as generative models for It\^o processes. Given (discrete observations of) samples of a fixed underlying It\^o process, the NJODE fra...