Academic Profile

Statistics

Similar Authors

Papers on arXiv

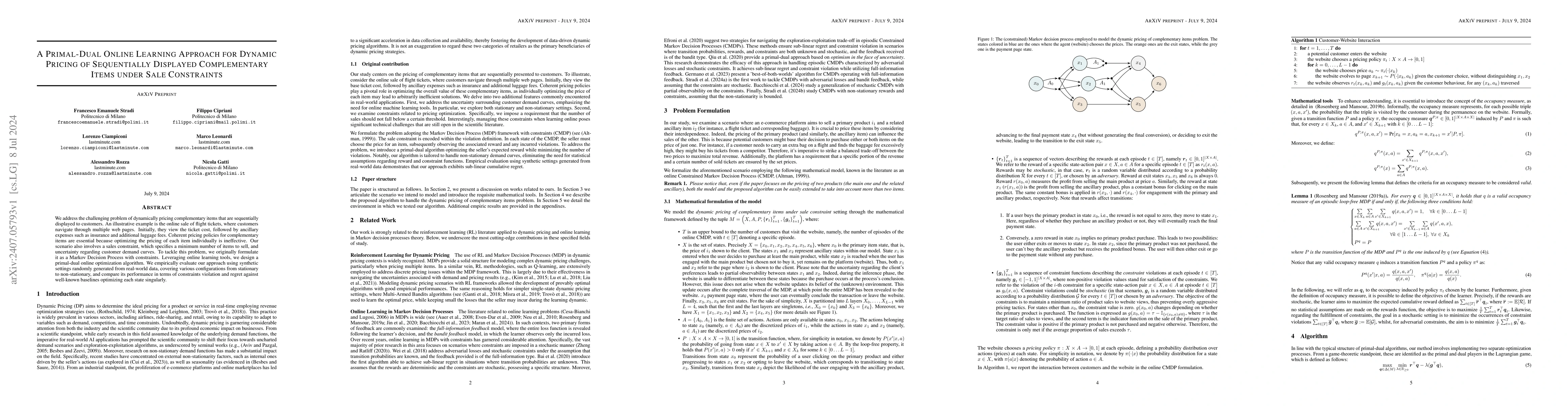

We address the challenging problem of dynamically pricing complementary items that are sequentially displayed to customers. An illustrative example is the online sale of flight tickets, where customer...

In constrained Markov decision processes (CMDPs) with adversarial rewards and constraints, a well-known impossibility result prevents any algorithm from attaining both sublinear regret and sublinear...

We study online learning problems in constrained Markov decision processes (CMDPs) with adversarial losses and stochastic hard constraints. We consider two different scenarios. In the first one, we ...

In Bayesian persuasion, an informed sender strategically discloses information to a receiver so as to persuade them to undertake desirable actions. Recently, a growing attention has been devoted to ...

We study online learning in episodic constrained Markov decision processes (CMDPs), where the goal of the learner is to collect as much reward as possible over the episodes, while guaranteeing that ...

We study online learning in \emph{constrained MDPs} (CMDPs), focusing on the goal of attaining sublinear strong regret and strong cumulative constraint violation. Differently from their standard (weak...

We study online learning in constrained Markov decision processes (CMDPs) in which rewards and constraints may be either stochastic or adversarial. In such settings, Stradi et al.(2024) proposed the f...

This paper initiates the study of data-dependent regret bounds in constrained MAB settings. These bounds depend on the sequence of losses that characterize the problem instance. Thus, they can be much...

We study online decision making problems under resource constraints, where both reward and cost functions are drawn from distributions that may change adversarially over time. We focus on two canonica...

We study \emph{online episodic Constrained Markov Decision Processes} (CMDPs) under both stochastic and adversarial constraints. We provide a novel algorithm whose guarantees greatly improve those of ...

Algorithmic \emph{replicability} has recently been introduced to address the need for reproducible experiments in machine learning. A \emph{replicable online learning} algorithm is one that takes the ...

We study the constrained variant of the \emph{multi-armed bandit} (MAB) problem, in which the learner aims not only at minimizing the total loss incurred during the learning dynamic, but also at contr...

We design the first regret guarantees for robust dynamic pricing that decouple the dependence on the corruption $C$ and the time horizon $T$. In dynamic pricing, a seller with unlimited supply of a go...

We study \emph{multi-armed bandits} (MABs) augmented with \emph{best-action queries}, in which the learner may additionally query an oracle that reveals the best arm in the current round. This setting...

Online resource allocation (ORA) is a fundamental framework for sequential decision-making problems under budget constraints, with applications ranging from online advertising to revenue management. I...

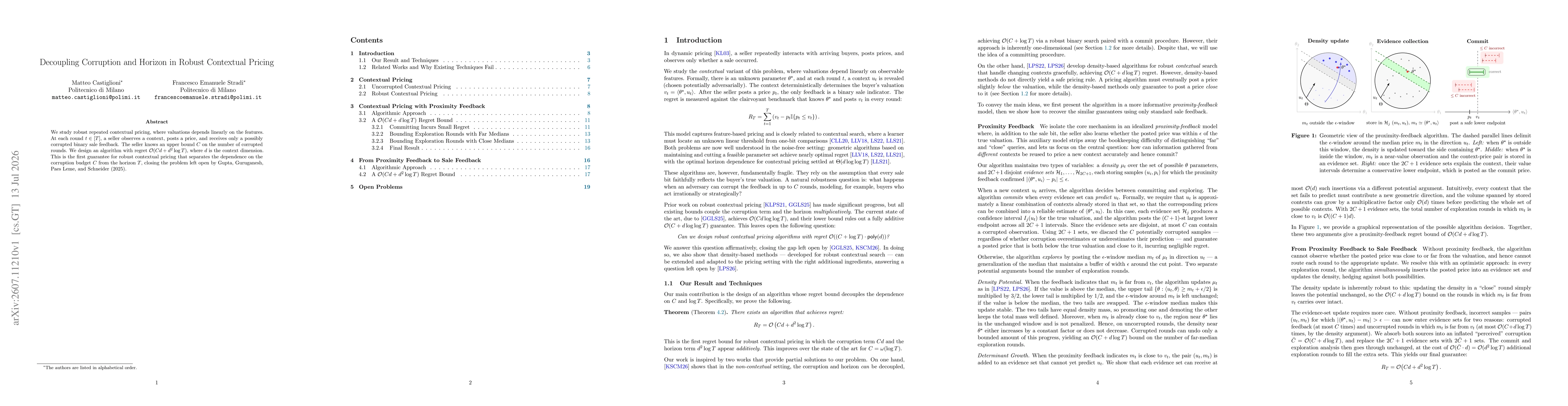

We study robust repeated contextual pricing, where valuations depends linearly on the features. At each round $t\in[T]$, a seller observes a context, posts a price, and receives only a possibly corrup...