Academic Profile

Statistics

Similar Authors

Papers on arXiv

Although linear and quadratic discriminant analysis are widely recognized classical methods, they can encounter significant challenges when dealing with non-Gaussian distributions or contaminated da...

Expectation-Maximization (EM) algorithm is a widely used iterative algorithm for computing maximum likelihood estimate when dealing with Gaussian Mixture Model (GMM). When the sample size is smaller...

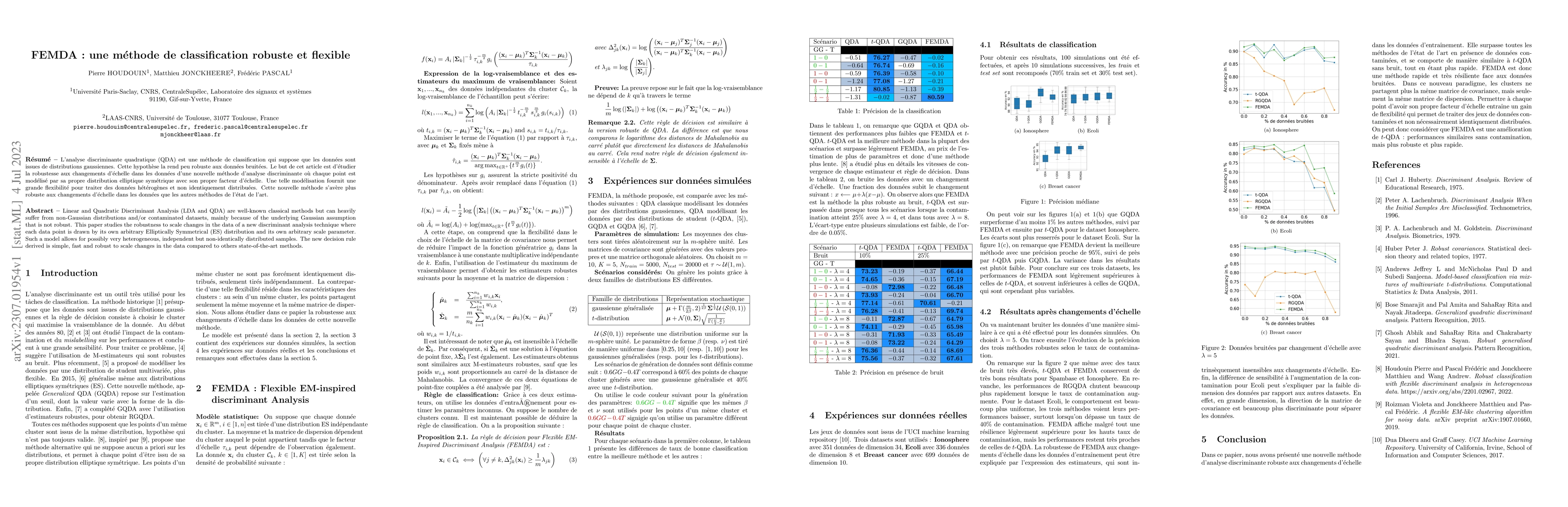

Linear and Quadratic Discriminant Analysis (LDA and QDA) are well-known classical methods but can heavily suffer from non-Gaussian distributions and/or contaminated datasets, mainly because of the u...

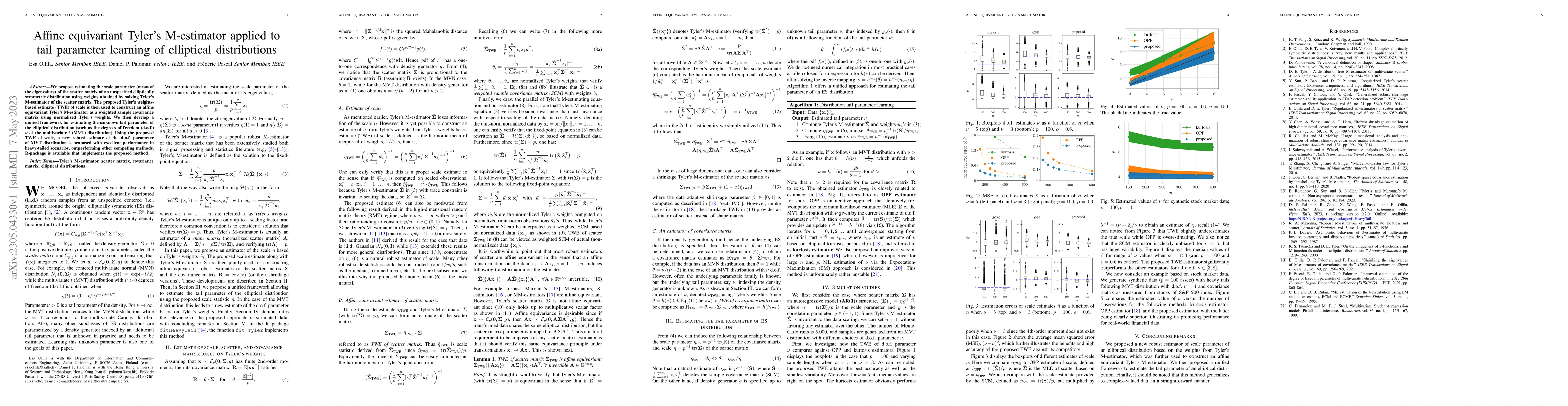

We propose estimating the scale parameter (mean of the eigenvalues) of the scatter matrix of an unspecified elliptically symmetric distribution using weights obtained by solving Tyler's M-estimator ...

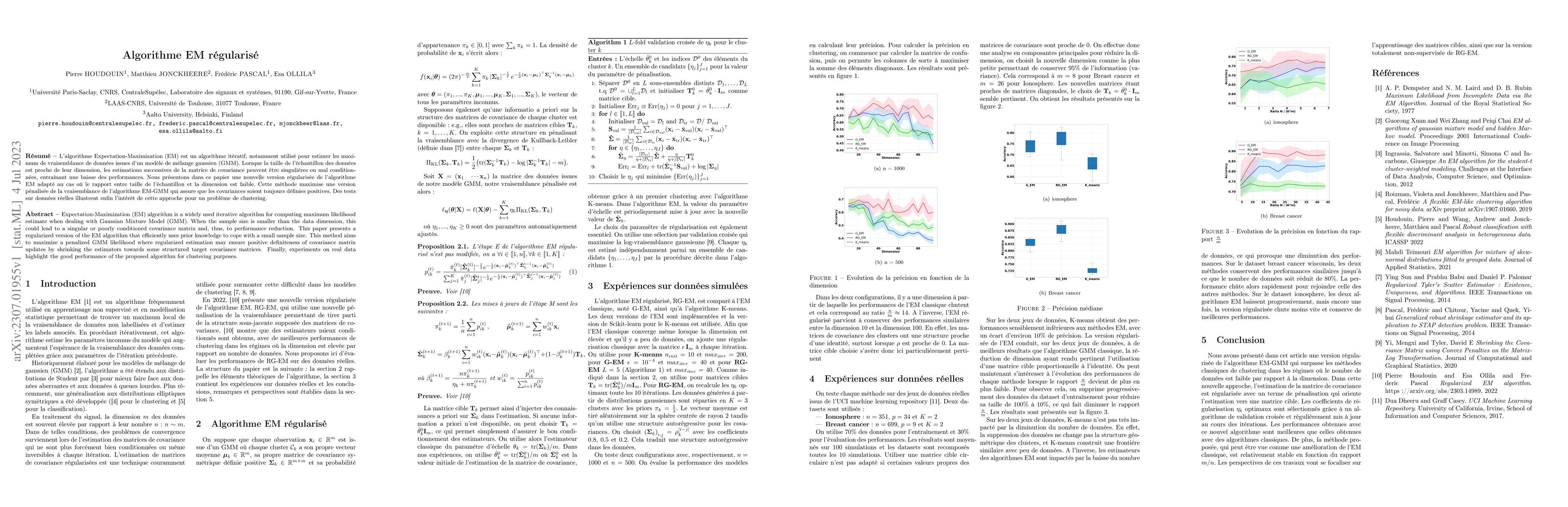

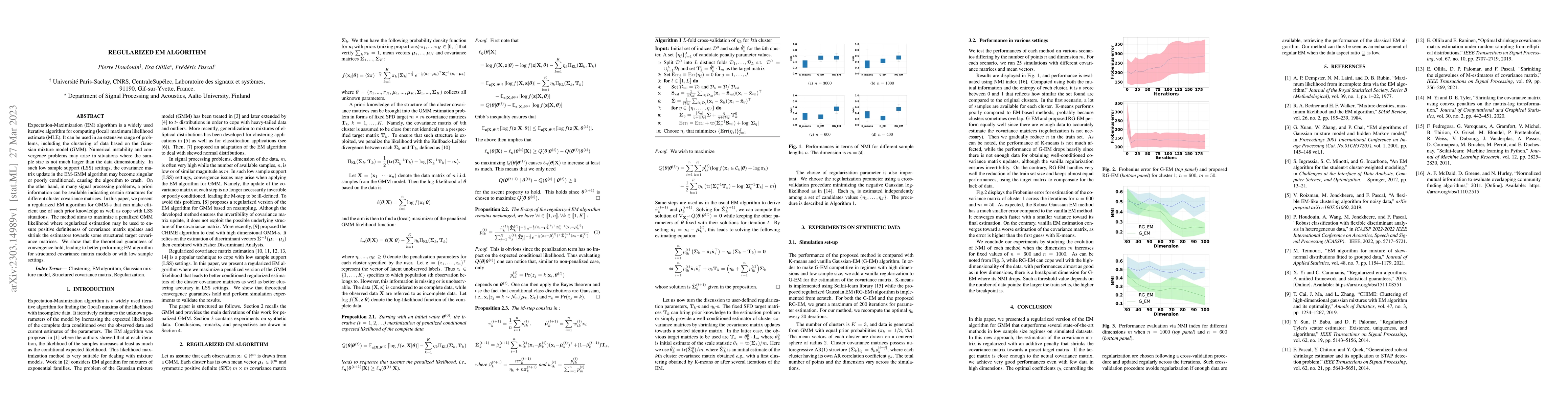

Expectation-Maximization (EM) algorithm is a widely used iterative algorithm for computing (local) maximum likelihood estimate (MLE). It can be used in an extensive range of problems, including the ...

A popular regularized (shrinkage) covariance estimator is the shrinkage sample covariance matrix (SCM) which shares the same set of eigenvectors as the SCM but shrinks its eigenvalues toward its gra...

The eigenvalue decomposition (EVD) parameters of the second order statistics are ubiquitous in statistical analysis and signal processing. Notably, the EVD of robust scatter $M$-estimators is a popu...