Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper develops a semi-parametric procedure for estimation of unconditional quantile partial effects using quantile regression coefficients. The estimator is based on an identification result sh...

This paper studies the network structure and fragmentation of the Argentinean interbank market. Both the unsecured (CALL) and the secured (REPO) markets are examined, applying complex network analys...

This paper studies the unconditional effects of a general policy intervention, which includes location-scale shifts and simultaneous shifts as special cases. The location-scale shift is intended to ...

A new Stata command, ldvqreg, is developed to estimate quantile regression models for the cases of censored (with lower and/or upper censoring) and binary dependent variables. The estimators are imp...

We study the diffusion of shocks in the global financial cycle and global liquidity conditions to emerging and developing economies. We show that the classification according to their external trade...

The `paradox of progress' is an empirical regularity that associates more education with larger income inequality. Two driving and competing factors behind this phenomenon are the convexity of the `...

This paper proposes an empirical method to implement the recentered influence function (RIF) regression of Firpo, Fortin and Lemieux (2009), a relevant method to study the effect of covariates on ma...

This paper develops a first-stage linear regression representation for the instrumental variables (IV) quantile regression (QR) model. The quantile first-stage is analogous to the least squares case...

Linear regressions with endogeneity are widely used to estimate causal effects. This paper studies a statistical framework that has two common issues, endogeneity of the regressors, and heteroskedasti...

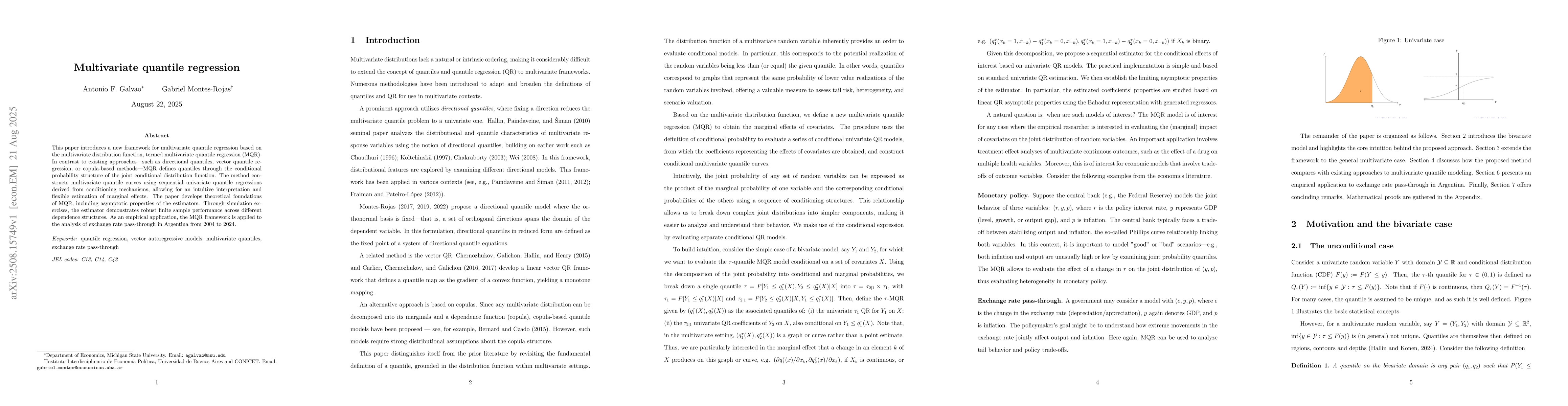

This paper introduces a new framework for multivariate quantile regression based on the multivariate distribution function, termed multivariate quantile regression (MQR). In contrast to existing appro...

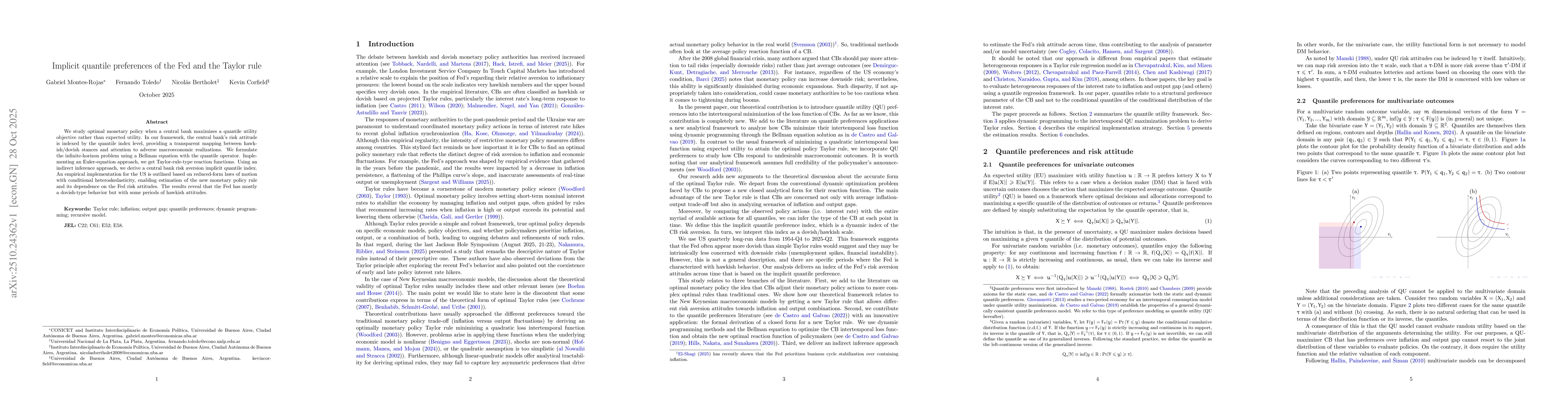

We study optimal monetary policy when a central bank maximizes a quantile utility objective rather than expected utility. In our framework, the central bank's risk attitude is indexed by the quantile ...