Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper we study neural networks and their approximating power in panel data models. We provide asymptotic guarantees on deep feed-forward neural network estimation of the conditional mean, bu...

We suggest a new single-equation test for Uncovered Interest Parity (UIP) based on a dynamic regression approach. The method provides consistent and asymptotically efficient parameter estimates, and...

In this paper we develop inference for high dimensional linear models, with serially correlated errors. We examine Lasso under the assumption of strong mixing in the covariates and error process, al...

Least squares regression with heteroskedasticity consistent standard errors ("OLS-HC regression") has proved very useful in cross section environments. However, several major difficulties, which are...

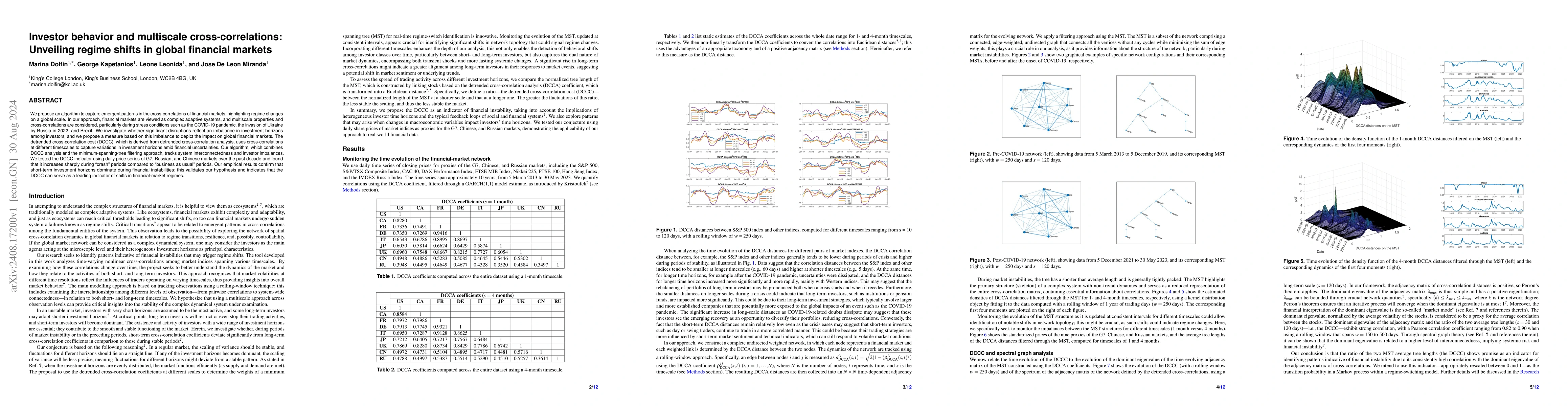

We propose an algorithm to capture emergent patterns in the cross-correlations of financial markets, highlighting regime changes on a global scale. In our approach, financial markets are viewed as com...

In this paper we examine the existence of heterogeneity within a group, in panels with latent grouping structure. The assumption of within group homogeneity is prevalent in this literature, implying t...

This paper analyzes realized return behavior across a broad set of crypto assets by estimating heterogeneous exposures to idiosyncratic and systematic risk. A key challenge arises from the latent natu...

This paper introduces and analyzes a framework that accommodates general heterogeneity in regression modeling. It demonstrates that regression models with fixed or time-varying parameters can be estim...

We introduce a multiscale measure of network instability based on the joint use of Detrended Cross-Correlation Analysis (DCCA) and Minimum Spanning Tree (MST) filtering. The proposed metric, the Elast...

High-dimensional regression specification and analysis is a complex and active area of research in statistics, machine learning, and econometrics. This paper proposes a new approach, Boosting with Mul...

We study spillover effects in corporate toxic emissions using a heterogeneous panel network of U.S. industrial facilities from 2000-2023. Rather than imposing a network structure a priori, we uncover ...

This paper examines how firm-level determinants of industrial emissions evolve over time as firms adapt to environmental regulation, economic conditions, and organisational constraints. Using a panel ...

We develop a novel methodology for estimation and inference in high-dimensional panel network models with latent dual structures. The framework allows outcomes to be affected simultaneously by positiv...