Academic Profile

Statistics

Similar Authors

Papers on arXiv

The covariance function of a Gauss-Markov process evaluated at points $(s,t)$ admits a representation as a product of a function of $\min(s,t)$ and a function of $\max(s,t)$. We call these functions...

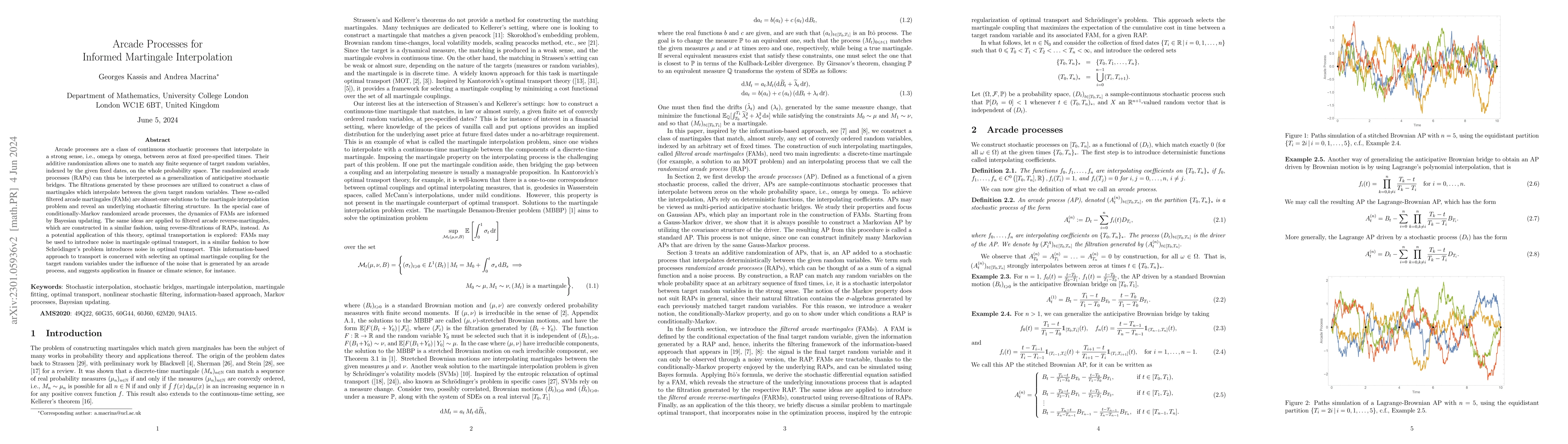

Arcade processes are a class of continuous stochastic processes that interpolate in a strong sense, i.e., omega by omega, between zeros at fixed pre-specified times. Their additive randomization all...

Randomized arcade processes are a class of continuous stochastic processes that interpolate in a strong sense, i.e., omega by omega, between any given ordered set of random variables, at fixed pre-spe...