Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper introduces the $\sigma$-Cell, a novel Recurrent Neural Network (RNN) architecture for financial volatility modeling. Bridging traditional econometric approaches like GARCH with deep learn...

Volatility models of price fluctuations are well studied in the econometrics literature, with more than 50 years of theoretical and empirical findings. The recent advancements in neural networks (NN...

Volatility prediction for financial assets is one of the essential questions for understanding financial risks and quadratic price variation. However, although many novel deep learning models were r...

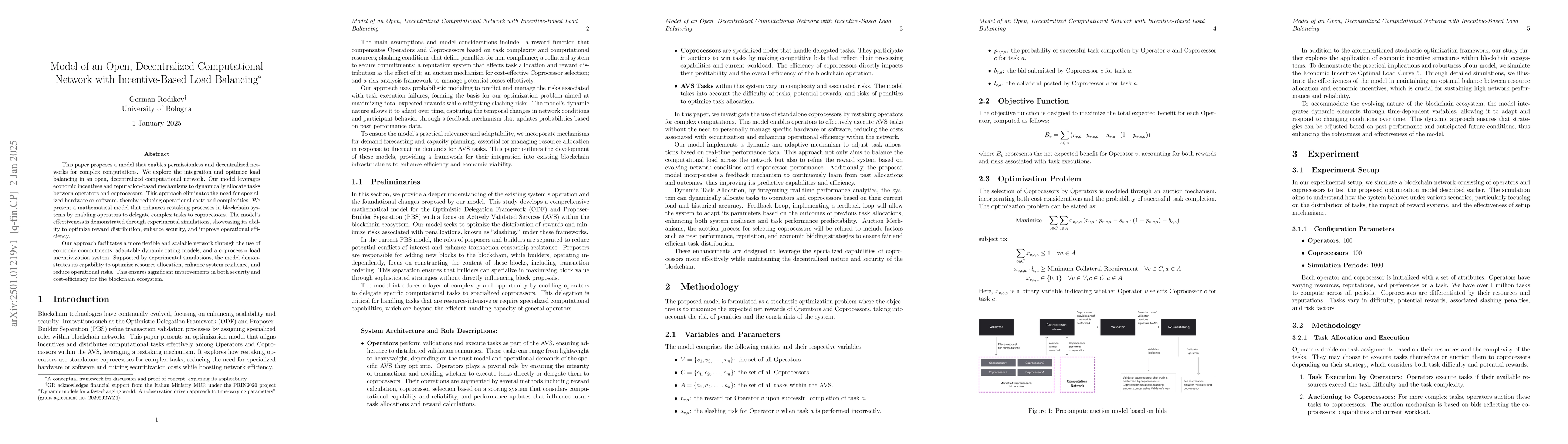

This paper proposes a model that enables permissionless and decentralized networks for complex computations. We explore the integration and optimize load balancing in an open, decentralized computatio...

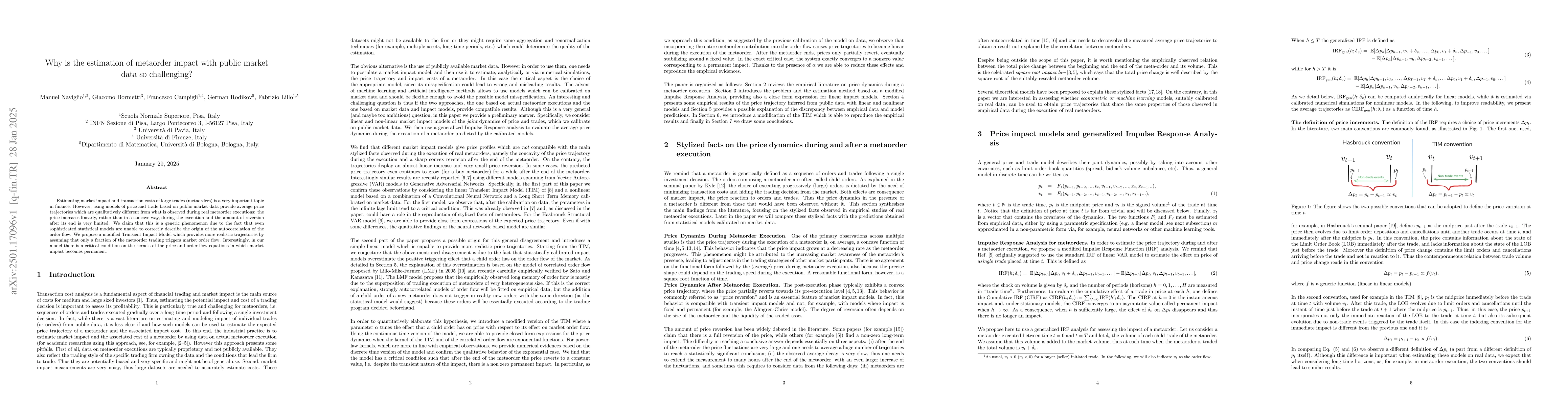

Estimating market impact and transaction costs of large trades (metaorders) is a very important topic in finance. However, using models of price and trade based on public market data provide average p...