Academic Profile

Statistics

Similar Authors

Papers on arXiv

We study online learning in episodic constrained Markov decision processes (CMDPs), where the goal of the learner is to collect as much reward as possible over the episodes, while guaranteeing that ...

Autoregressive processes naturally arise in a large variety of real-world scenarios, including stock markets, sales forecasting, weather prediction, advertising, and pricing. When facing a sequentia...

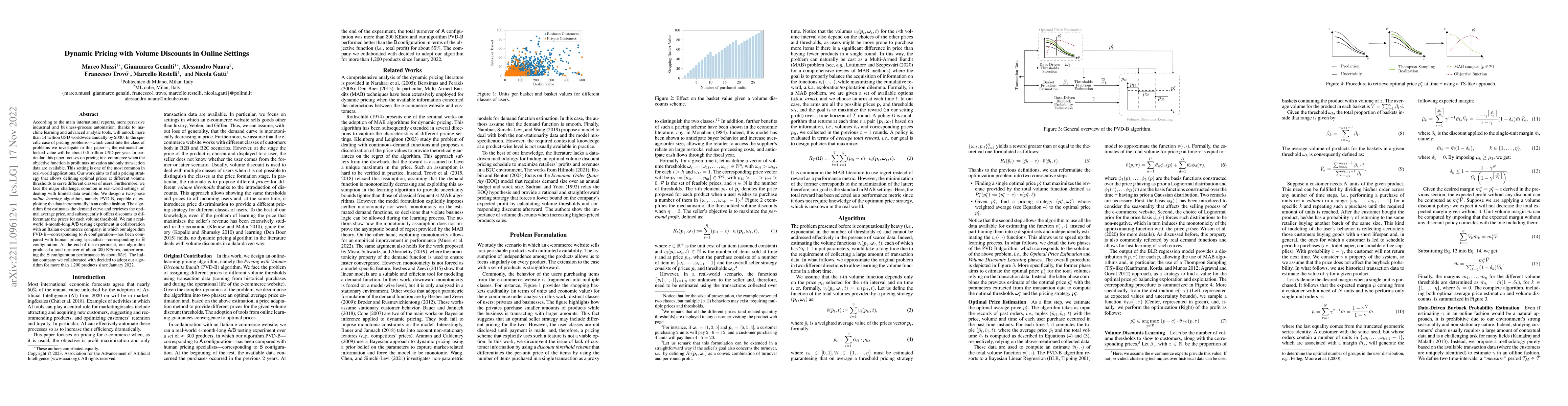

According to the main international reports, more pervasive industrial and business-process automation, thanks to machine learning and advanced analytic tools, will unlock more than 14 trillion USD ...

Rested and Restless Bandits are two well-known bandit settings that are useful to model real-world sequential decision-making problems in which the expected reward of an arm evolves over time due to t...

Regret minimization in stochastic non-stationary bandits gained popularity over the last decade, as it can model a broad class of real-world problems, from advertising to recommendation systems. Exist...

This paper initiates the study of data-dependent regret bounds in constrained MAB settings. These bounds depend on the sequence of losses that characterize the problem instance. Thus, they can be much...

Algorithmic \emph{replicability} has recently been introduced to address the need for reproducible experiments in machine learning. A \emph{replicable online learning} algorithm is one that takes the ...

Network routers that enforce Quality-of-Service (QoS) guarantees must decide, at every clock cycle, which expiring packet of information to transmit, even when the value of the packet is unknown until...