Academic Profile

Statistics

Similar Authors

Papers on arXiv

Risk evaluation is a forecast, and its validity must be backtested. Probability distribution forecasts are used in this work and allow for more powerful validations compared to point forecasts. Our ...

For many financial applications, it is important to have reliable and tractable models for the behavior of assets and indexes, for example in risk evaluation. A successful approach is based on ARCH ...

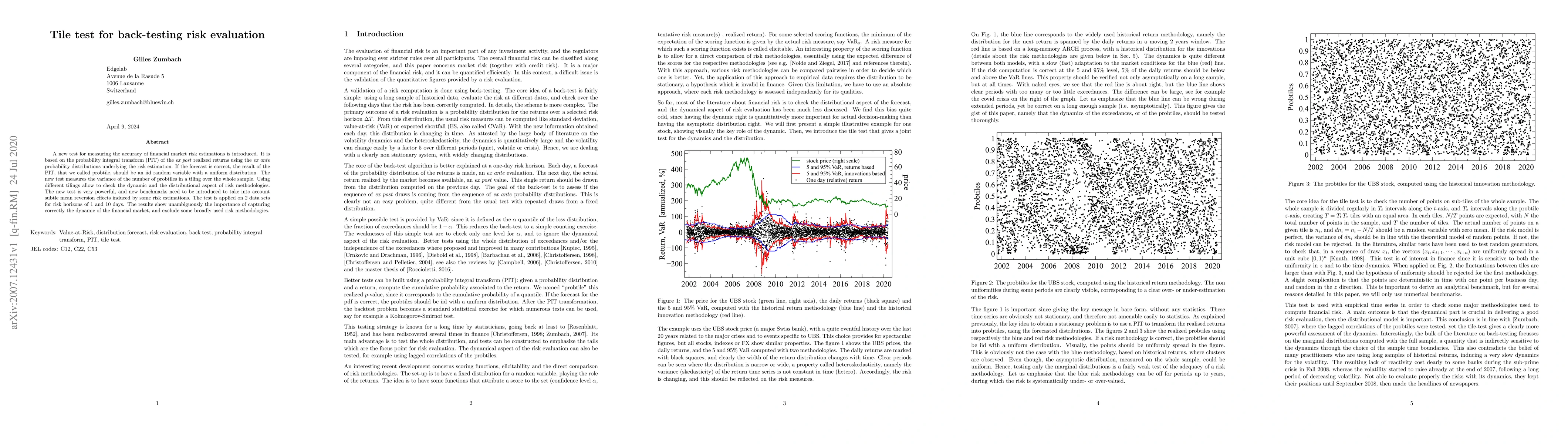

A new test for measuring the accuracy of financial market risk estimations is introduced. It is based on the probability integral transform (PIT) of the ex post realized returns using the ex ante pr...

For long term investments, model portfolios are defined at the level of indexes, a setup known as Strategic Asset Allocation (SAA). The possible outcomes at a scale of a few decades can be obtained by...