Academic Profile

Statistics

Similar Authors

Papers on arXiv

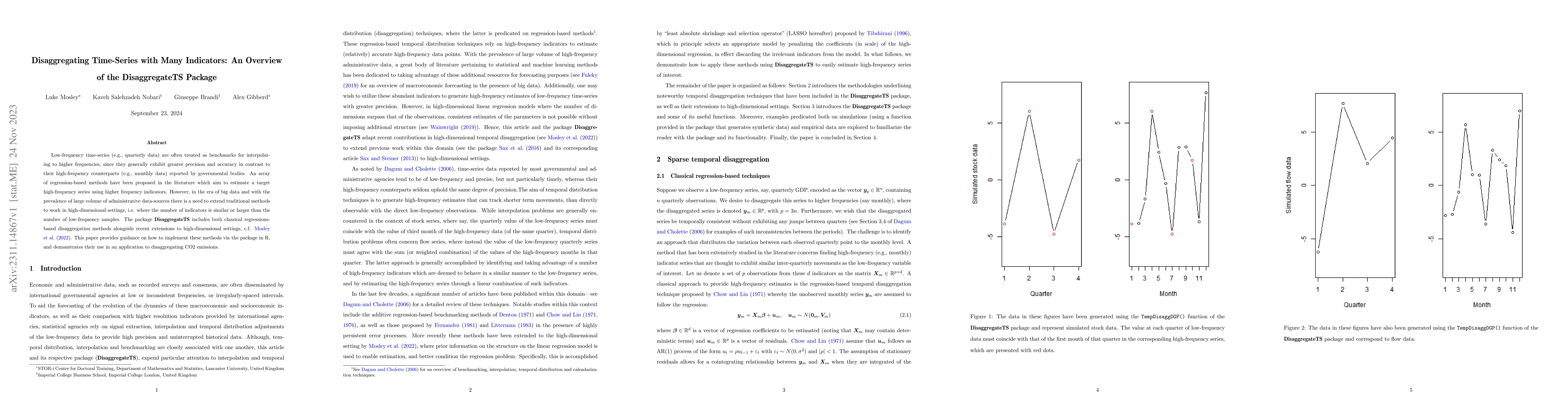

Low-frequency time-series (e.g., quarterly data) are often treated as benchmarks for interpolating to higher frequencies, since they generally exhibit greater precision and accuracy in contrast to t...

Pricing derivatives goes back to the acclaimed Black and Scholes model. However, such a modeling approach is known not to be able to reproduce some of the financial stylized facts, including the dyn...

Multilayer networks proved to be suitable in extracting and providing dependency information of different complex systems. The construction of these networks is difficult and is mostly done with a s...

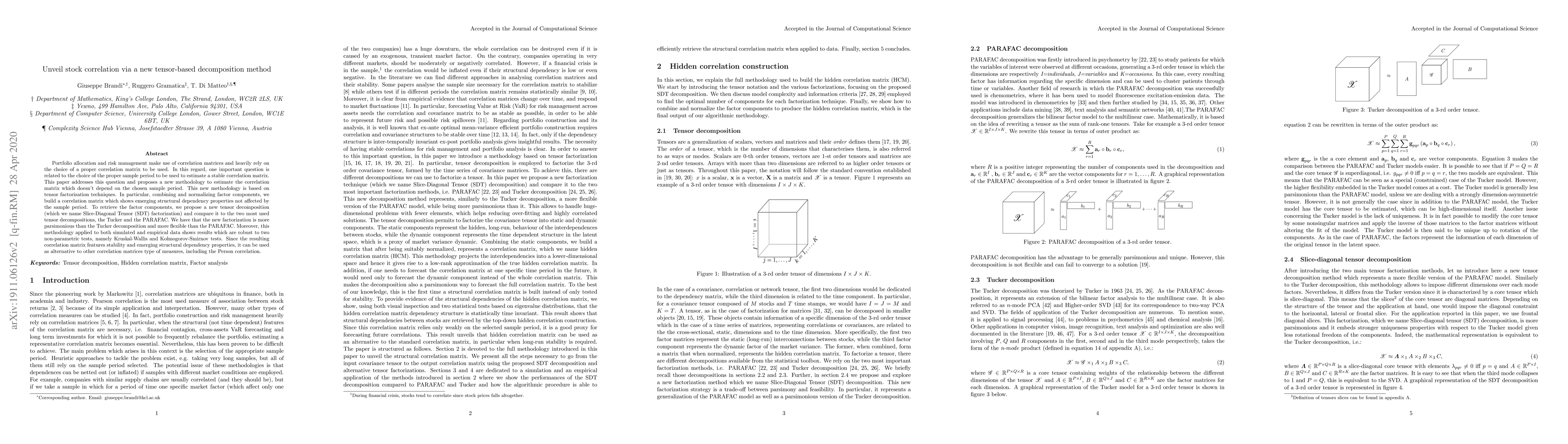

The analysis of multidimensional data is becoming a more and more relevant topic in statistical and machine learning research. Given their complexity, such data objects are usually reshaped into mat...

Portfolio allocation and risk management make use of correlation matrices and heavily rely on the choice of a proper correlation matrix to be used. In this regard, one important question is related ...

The rough Bergomi (rBergomi) model, characterised by its roughness parameter $H$, has been shown to exhibit multiscaling behaviour as $H$ approaches zero. Multiscaling has profound implications for fi...