Academic Profile

Statistics

Similar Authors

Papers on arXiv

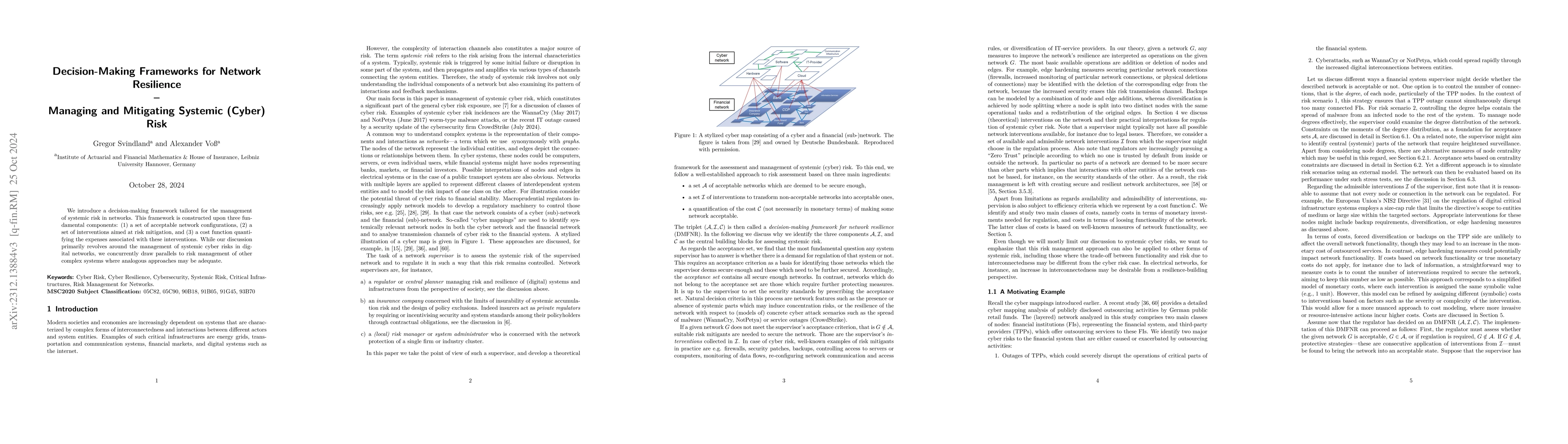

We introduce a novel class of risk measures designed for the management of systemic risk in networks. In contrast to prevailing approaches, these risk measures target the topological configuration o...

This paper assumes a robust, in general not dominated, probabilistic framework and provides necessary and sufficient conditions for a bipolar representation of subsets of the set of all quasi-sure e...

Based on classical contagion models we introduce an artificial cyber lab: the digital twin of a complex cyber system in which possible cyber resilience measures may be implemented and tested. Using ...

The paper provides a comprehensive overview of modeling and pricing cyber insurance and includes clear and easily understandable explanations of the underlying mathematical concepts. We distinguish ...

We analyze the limiting behavior of the risk premium associated with the Pareto optimal risk sharing contract in an infinitely expanding pool of risks under a general class of law-invariant risk mea...

In this paper we analyse in the framework of constructive mathematics (BISH) the validity of Farkas' lemma and related propositions, namely the Fredholm alternative for solvability of systems of lin...

We discuss when law-invariant convex functionals "collapse to the mean". More precisely, we show that, in a large class of spaces of random variables and under mild semicontinuity assumptions, the e...

Robust models in mathematical finance replace the classical single probability measure by a sufficiently rich set of probability measures on the future states of the world to capture (Knightian) unc...

We establish general versions of a variety of results for quasiconvex, lower-semicontinuous, and law-invariant functionals. Our results extend well-known results from the literature to a large class...

This paper assumes a robust stochastic model where a set $\mathcal{P}$ of probability measures replaces the single probability measure of dominated models. We introduce and study $\mathcal{P}$-sensiti...