Academic Profile

Statistics

Similar Authors

Papers on arXiv

For the kernel estimator of the quantile density function (the derivative of the quantile function), I show how to perform the boundary bias correction, establish the rate of strong uniform consiste...

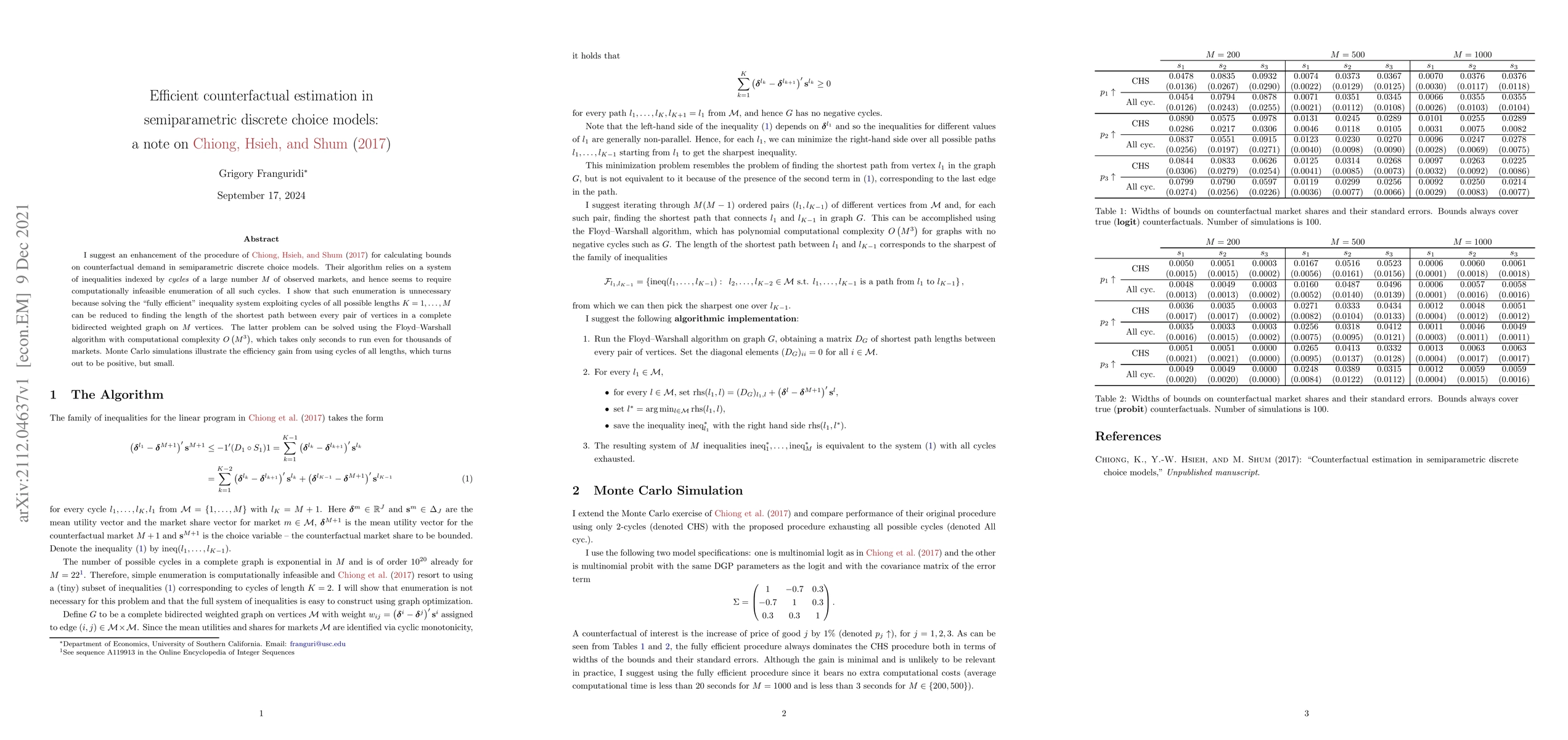

I suggest an enhancement of the procedure of Chiong, Hsieh, and Shum (2017) for calculating bounds on counterfactual demand in semiparametric discrete choice models. Their algorithm relies on a syst...

In a classical model of the first-price sealed-bid auction with independent private values, we develop nonparametric estimation and inference procedures for a class of policy-relevant metrics, such ...

We study the bias of classical quantile regression and instrumental variable quantile regression estimators. While being asymptotically first-order unbiased, these estimators can have non-negligible...

It has long been established that, if a panel dataset suffers from attrition, auxiliary (refreshment) sampling restores full identification under additional assumptions that still allow for nontrivial...

Given a differentially private unbiased estimate $\tilde{q}=q(D) +\nu$ of a statistic $q(D)$, we wish to obtain unbiased estimates of functions of $q(D)$, such as $1/q(D)$, solely through post-process...

We show how to identify the distributions of the error components in the two-way dyadic model $y_{ij}=c+\alpha_i+\eta_j+\varepsilon_{ij}$. To this end, we extend the lemma of Kotlarski (1967), mimicki...

We consider a generalized method of moments framework in which a part of the data vector is missing for some units in a completely unrestricted, potentially endogenous way. In this setup, the paramete...

In panel data subject to nonignorable attrition, auxiliary (refreshment) sampling may restore full identification under weak assumptions on the attrition process. Despite their generality, these ident...

Partial identification often arises when the joint distribution of the data is known only up to its marginals. We consider the corresponding partially identified GMM model and develop a methodology fo...