Academic Profile

Statistics

Similar Authors

Papers on arXiv

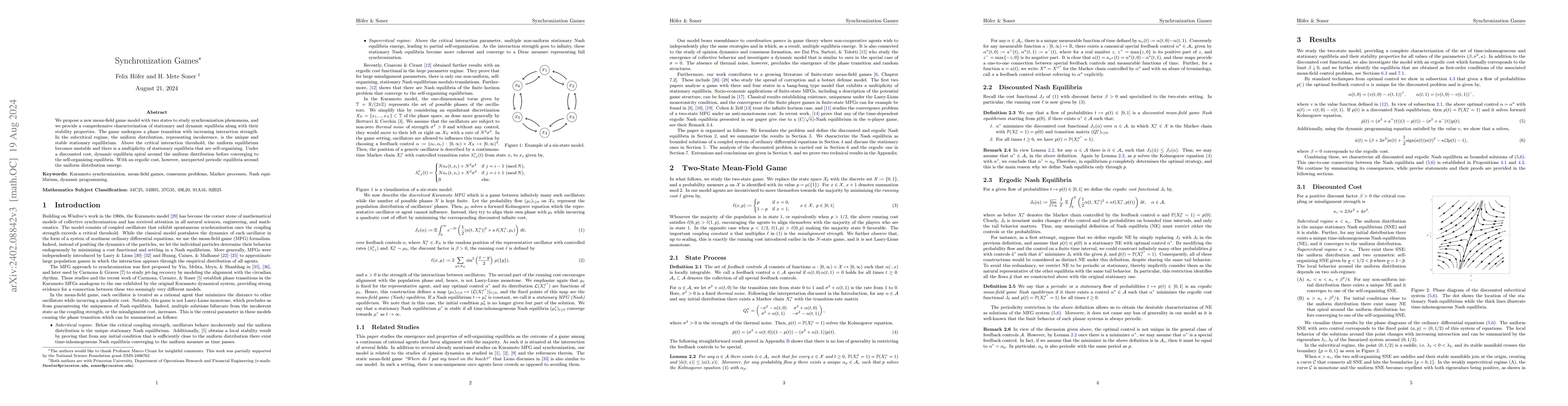

We propose a new mean-field game model with two states to study synchronization phenomena, and we provide a comprehensive characterization of stationary and dynamic equilibria along with their stabi...

Dynamic programming equations for mean field control problems with a separable structure are Eikonal equations on the Wasserstein space. Standard differentiation using linear derivatives yield a dir...

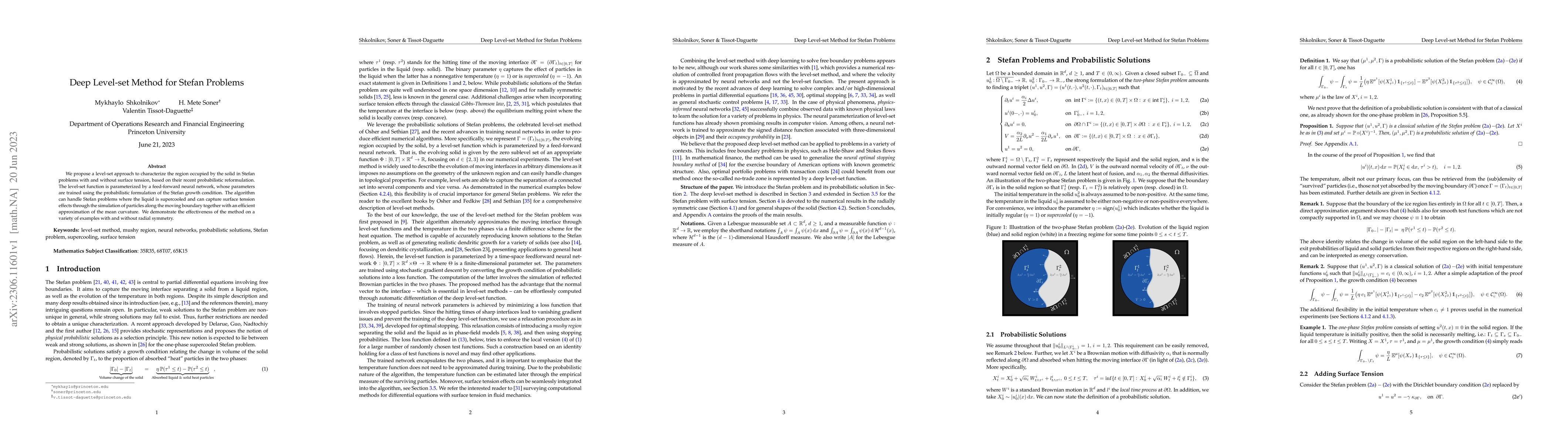

We propose a level-set approach to characterize the region occupied by the solid in Stefan problems with and without surface tension, based on their recent probabilistic reformulation. The level-set...

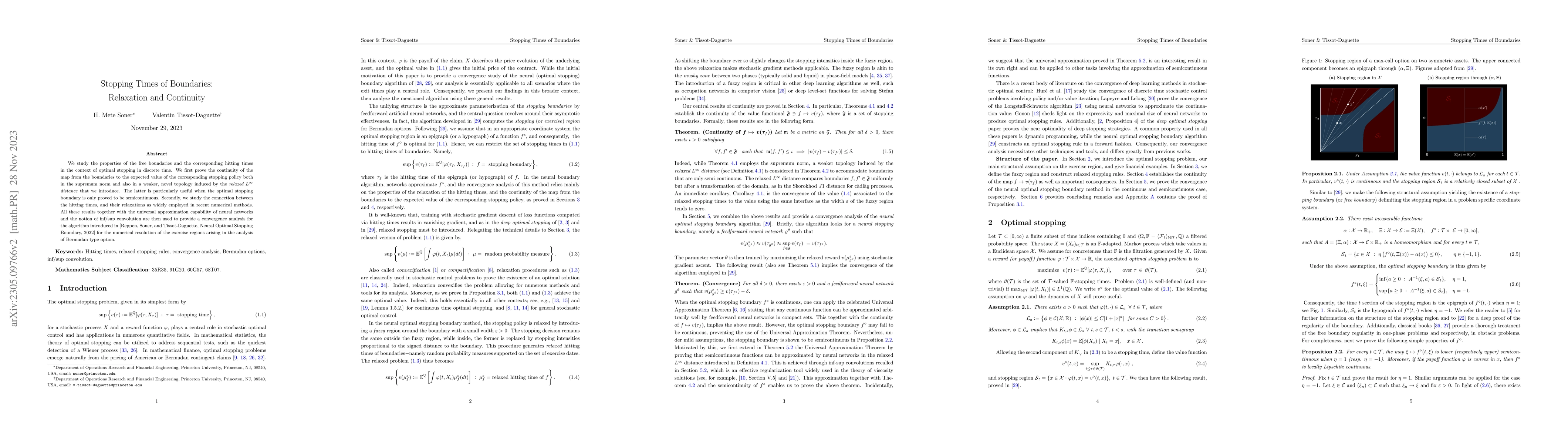

We study the properties of the free boundaries and the corresponding hitting times in the context of optimal stopping in discrete time. We first prove the continuity of the map from the boundaries t...

An optimal control problem in the space of probability measures, and the viscosity solutions of the corresponding dynamic programming equations defined using the intrinsic linear derivative are stud...

The classical Kuramoto model is studied in the setting of an infinite horizon mean field game. The system is shown to exhibit both synchronization and phase transition. Incoherence below a critical ...

This paper outlines, and through stylized examples evaluates a novel and highly effective computational technique in quantitative finance. Empirical Risk Minimization (ERM) and neural networks are k...

A method based on deep artificial neural networks and empirical risk minimization is developed to calculate the boundary separating the stopping and continuation regions in optimal stopping. The alg...

Many modern computational approaches to classical problems in quantitative finance are formulated as empirical loss minimization (ERM), allowing direct applications of classical results from statist...

We study a class of non linear integro-differential equations on the Wasserstein space related to the optimal control of McKean--Vlasov jump-diffusions. We develop an intrinsic notion of viscosity s...

We obtain a dual representation of the Kantorovich functional defined for functions on the Skorokhod space using quotient sets. Our representation takes the form of a Choquet capacity generated by m...

We propose a model in which dividend payments occur at regular, deterministic intervals in an otherwise continuous model. This contrasts traditional models where either the payment of continuous div...

We reconsider the microeconomic foundations of financial economics. Motivated by the importance of Knightian Uncertainty in markets, we present a model that does not carry any probabilistic structur...

We consider the optimal control of occupied processes which record all positions of the state process. Dynamic programming yields nonlinear equations on the space of positive measures. We develop the ...

We consider a mean-field optimal control problem with general dynamics including common noise and jumps and show that its minimizers are Nash equilibria of an associated mean-field game of controls. T...

We analyze an algorithm to numerically solve the mean-field optimal control problems by approximating the optimal feedback controls using neural networks with problem specific architectures. We approx...

This paper studies Mean Field Games (MFGs) in which agent dynamics are given by jump processes of controlled intensity, with mean-field interaction via the controls and affecting the jump intensities....

We study dynamic finite-player and mean-field stochastic games within the framework of Markov perfect equilibria (MPE). Our focus is on discrete time and space structures without monotonicity. Unlike ...

We study Markov perfect equilibria in continuous-time dynamic games with finitely many symmetric players. The corresponding Nash system reduces to the Nash-Lasry-Lions equation for the common value fu...

We give a new formulation of the relative arbitrage problem from stochastic portfolio theory that asks for a time horizon beyond which arbitrage relative to the market exists in all ``sufficiently vol...