2

arXiv Papers

5

Total Publications

Profile

Academic Profile

Metrics

Statistics

2

arXiv Papers

5

Total Publications

Network

Similar Authors

Publications

Papers on arXiv

arXiv

Interpreting and predicting the economy flows: A time-varying parameter

global vector autoregressive integrated the machine learning model

The paper proposes a time-varying parameter global vector autoregressive (TVP-GVAR) framework for predicting and analysing developed region economic variables. We want to provide an easily accessibl...

arXiv

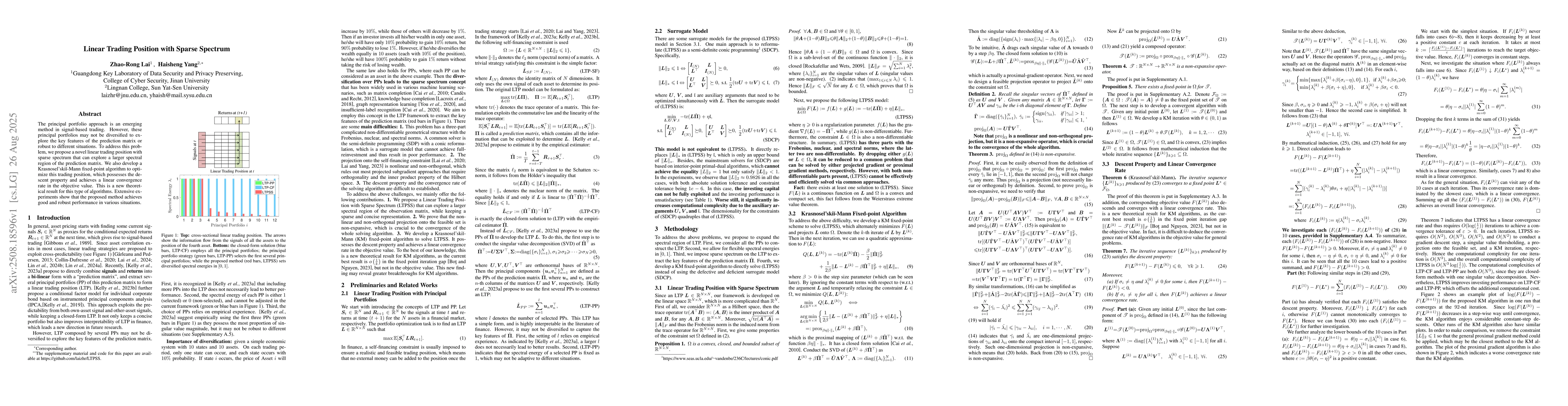

Linear Trading Position with Sparse Spectrum

The principal portfolio approach is an emerging method in signal-based trading. However, these principal portfolios may not be diversified to explore the key features of the prediction matrix or robus...