Academic Profile

Statistics

Similar Authors

Papers on arXiv

The objective of this paper is to establish the decomposition theorem for supermartingales under the $G$-framework. We first introduce a $g$-nonlinear expectation via a kind of $G$-BSDE and the asso...

In this paper, we study the backward stochastic differential equations driven by G-Brownian motion with double mean reflections, which means that the constraints are made on the law of the solution....

In this paper, we establish propagation of chaos (POC) for doubly mean reflected backward stochastic differential equations (MRBSDEs). MRBSDEs differentiate the typical RBSDEs in that the constraint...

In this paper, we study the backward stochastic differential equation (BSDE) with two nonlinear mean reflections, which means that the constraints are imposed on the distribution of the solution but...

In this paper, we study the Skorokhod problem with two constraints, where the constraints are in a nonlinear fashion. We prove the existence and uniqueness of the solution and also provide the expli...

In this paper, we study the mean reflected stochastic differential equations driven by G- Brownian motion, where the constraint depends on the distribution of the solution rather than on its paths. ...

In this paper, we consider the reflected backward stochastic differential equations driven by G-Brownian motion (reflected G-BSDEs) whose coefficients satisfy the beta-order Mao's condition. The uni...

We characterize optimal consumption policies in a recursive intertemporal utility framework with local substitution. We establish existence and uniqueness and a version of the Kuhn-Tucker theorem ch...

Due to the importance of the Cox-Ingersoll-Ross process in different areas of finance, a broad spectrum of studies and investigations on this model have been carried out. In case of ambiguity, we ch...

In this paper, we address the stochastic representation problem in discrete time under (non-linear) g-expectation. We establish existence and uniqueness of the solution, as well as a characterizatio...

We consider the well-posedness problem of multi-dimensional reflected backward stochastic differential equations driven by $G$-Brownian motion ($G$-BSDEs) with diagonal generators. Two methods, i.e....

We study an intertemporal consumption and portfolio choice problem under Knightian uncertainty in which agent's preferences exhibit local intertemporal substitution. We also allow for market frictio...

In this paper, we introduce a new method to study the doubly reflected backward stochastic differential equation driven by G-Brownian motion (G-BSDE). Our approach involves approximating the solutio...

In this paper, we study an irreversible investment problem under Knightian uncertainty. In a general framework, in which Knightian uncertainty is modeled through a set of multiple priors, we prove e...

In this paper, we study the optimal multiple stopping problem under Knightian uncertainty both under discrete-time case and continuous-time case. The Knightian uncertainty is modeled by a single rea...

In this paper, we study the reflected backward stochastic differential equations driven by G-Brownian motion with two reflecting obstacles, which means that the solution lies between two prescribed ...

In this paper, we study the optimal multiple stopping problem under the filtration consistent nonlinear expectations. The reward is given by a set of random variables satisfying some appropriate ass...

We explore intertemporal preferences that are recursive and account for local intertemporal substitution. First, we establish a rigorous foundation for these preferences and analyze their properties. ...

In this paper, we study reflected backward stochastic differential equations driven by rough paths (rough RBSDEs), which can be understood as a probabilistic representation of nonlinear rough partial ...

In this paper, we analyze the mean field backward stochastic differential equations (MFBSDEs) with double mean reflections, whose generator and constraints both depend on the distribution of the solut...

In this paper, we study a kind of constrained backward stochastic differential equations (BSDEs) such that the nonlinear expectation of the composition of a loss function and the solution remains abov...

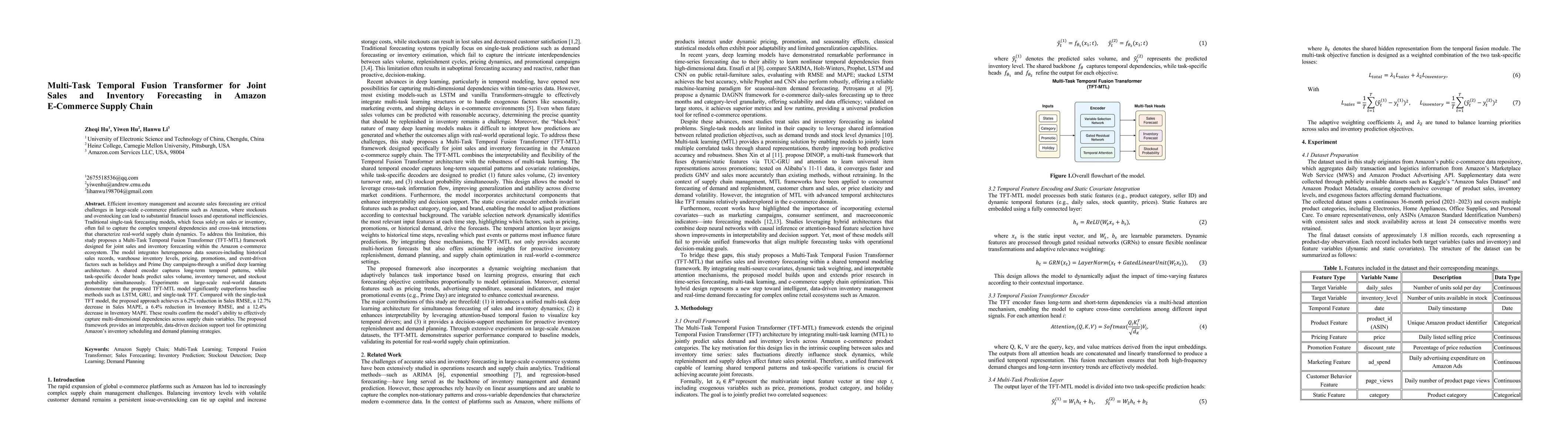

Efficient inventory management and accurate sales forecasting are critical challenges in large-scale e-commerce platforms such as Amazon, where stockouts and overstocking can lead to substantial finan...

In this paper, we introduce a new type of backward stochastic differential equations (BSDEs), called conditional expectation BSDEs, whose drivers depend not only on the value of the solutions but also...

In this paper, we study the doubly conditional reflected backward stochastic differential equations (BSDEs), where constraints are made on the conditional expectation of the first component of the sol...

In this paper, we study the reflected stochastic differential equations driven by G-Brownian motion (reflected G-SDEs) with two nonlinear constraints. With the help of the Skorokhod problem with nonli...

In this paper, we study the doubly reflected backward stochastic differential equations driven by $G$-Brownian motion ($G$-BSDEs for short) when the generator has quadratic growth in the $z$-component...

In this paper, we investigate mean-field backward stochastic differential equation (MFBSDE) with double mean reflections and nonlinear resistance. Specifically, the constraints are formulated in terms...

In this paper, we establish a propagation of chaos result for mean-field mean reflected backward stochastic differential equations (BSDEs), where both the generator and constraint depend on the distri...