Academic Profile

Statistics

Similar Authors

Papers on arXiv

This note lays part of the theoretical ground for a definition of differential systems modeling reinforcement learning in continuous time non-Markovian rough environments. Specifically we focus on o...

In this work, we study a natural nonparametric estimator of the transition probability matrices of a finite controlled Markov chain. We consider an offline setting with a fixed dataset, collected us...

In this paper, we study the Onsager-Machlup function and its relationship to the Freidlin-Wentzell function for measures equivalent to arbitrary infinite dimensional Gaussian measures. The Onsager-M...

We study sparse linear regression over a network of agents, modeled as an undirected graph (with no centralized node). The estimation problem is formulated as the minimization of the sum of the loca...

We study infinite server queues driven by Cox processes in a fast oscillatory random environment. While exact performance analysis is difficult, we establish diffusion approximations to the (re-scal...

This paper considers data-driven chance-constrained stochastic optimization problems in a Bayesian framework. Bayesian posteriors afford a principled mechanism to incorporate data and prior knowledg...

Datasets displaying temporal dependencies abound in science and engineering applications, with Markov models representing a simplified and popular view of the temporal dependence structure. In this ...

We present methodology for estimating the stochastic intensity of a doubly stochastic Poisson process. Statistical and theoretical analyses of traffic traces show that these processes are appropriat...

In this paper, we consider a $G_t/G_t/\infty$ infinite server queueing model in a random environment. More specifically, the arrival rate in our server is modeled as a highly fluctuating stochastic ...

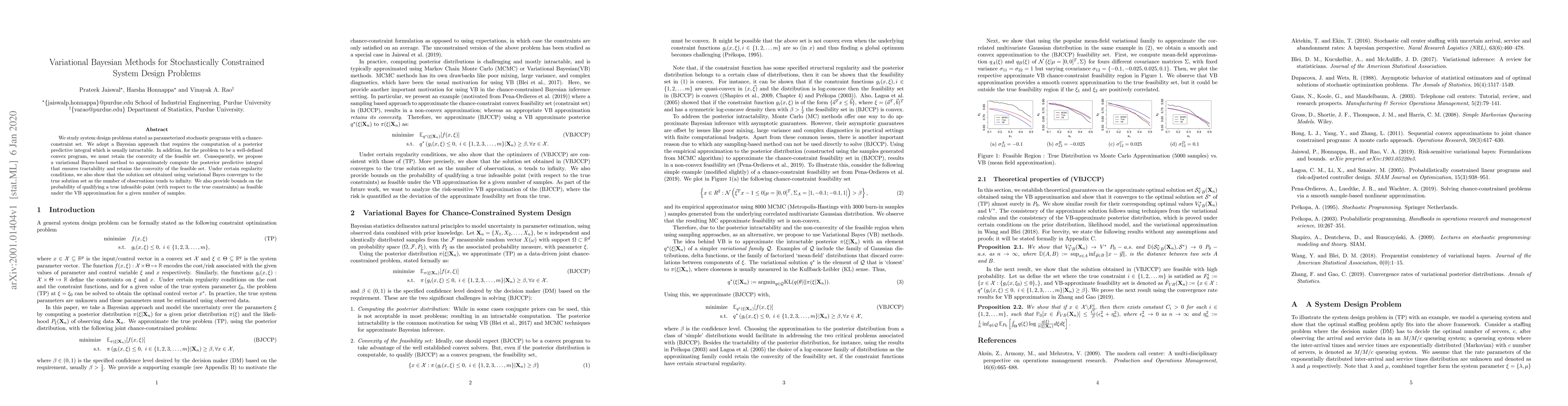

We study system design problems stated as parameterized stochastic programs with a chance-constraint set. We adopt a Bayesian approach that requires the computation of a posterior predictive integra...

The purpose of this note is to show that it is possible to establish a many-server functional strong law of large numbers (FSLLN) for the fraction of occupied servers (i.e., the scaled number-in-sys...

This paper establishes the asymptotic consistency of the {\it loss-calibrated variational Bayes} (LCVB) method. LCVB was proposed in~\cite{LaSiGh2011} as a method for approximately computing Bayesia...

In this paper we establish strong embedding theorems, in the sense of the Komlos-Major-Tusnady framework, for the performance metrics of a general class of transitory queueing models of nonstationar...

This paper gives an elementary proof for the following theorem: a renewal process can be represented by a doubly-stochastic Poisson process (DSPP) if and only if the Laplace-Stieltjes transform of the...

Estimating the transition dynamics of controlled Markov chains is crucial in fields such as time series analysis, reinforcement learning, and system exploration. Traditional non-parametric density est...

This paper introduces a drift optimization model of stochastic optimization problems driven by regulated stochastic processes. A broad range of problems across operations research, machine learning, a...

The standard linear quadratic Gaussian (LQG) framework assumes a Brownian noise process and relies on classical stochastic calculus tools, such as those based on Itô calculus. In this paper, we solve ...

This paper analyzes a service system modeled as a single-server queue, in which the service provider aims to dynamically maximize the expected revenue per unit of time. This is achieved by constructin...

We derive the Pontryagin maximum principle and $Q$-functions for the relaxed control of noisy rough differential equations. Our main tool is the development of a novel differentiation procedure along ...

We study robust nonlinear filtering for stochastic models driven by Lévy processes, where the signal and observation processes are coupled through common Brownian and jump noise. Robustness, defined a...

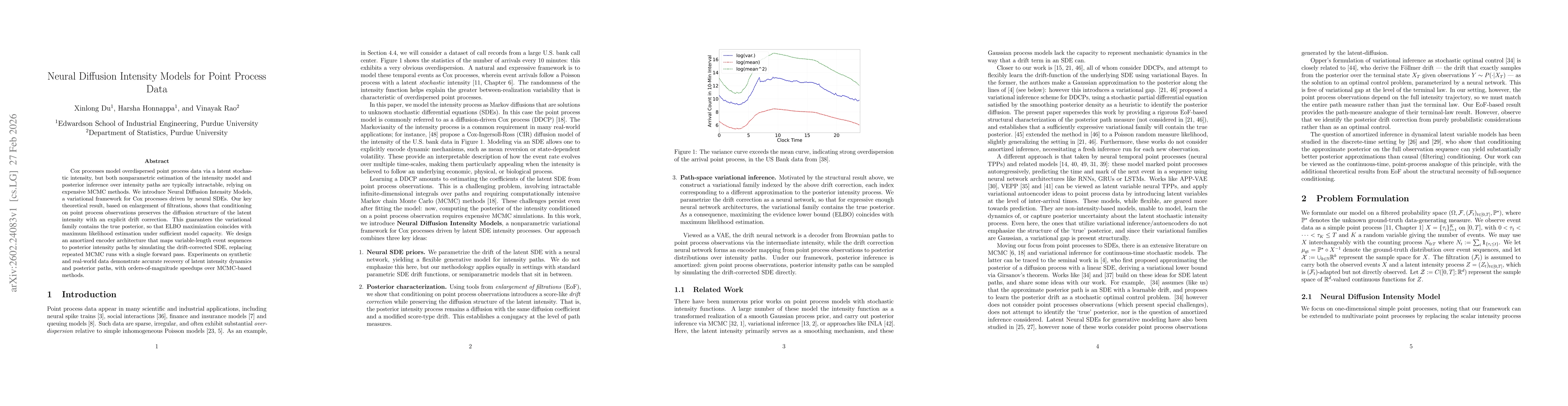

Cox processes model overdispersed point process data via a latent stochastic intensity, but both nonparametric estimation of the intensity model and posterior inference over intensity paths are typica...

The variational formulation of nonlinear filtering due to Mitter and Newton characterizes the filtering distribution as the unique minimizer of a free energy functional involving the relative entropy ...