Academic Profile

Statistics

Similar Authors

Papers on arXiv

In the common partially linear single-index model we establish a Bahadur representation for a smoothing spline estimator of all model parameters and use this result to prove the joint weak convergen...

We introduce a new "$(m,mp/n)$ out of $(n,p)$" sampling-with-replace\-ment bootstrap for eigenvalue statistics of high-dimensional sample covariance matrices based on $n$ independent $p$-dimensional...

Stochastic Gradient Descent (SGD) is a widely used tool in machine learning. In the context of Differential Privacy (DP), SGD has been well studied in the last years in which the focus is mainly on ...

This paper addresses the problem of deciding whether the dose response relationships between subgroups and the full population in a multi-regional trial are similar to each other. Similarity is meas...

For statistical inference on an infinite-dimensional Hilbert space $\H $ with no moment conditions we introduce a new class of energy distances on the space of probability measures on $\H$. The prop...

We investigate distributional properties of a class of spectral spatial statistics under irregular sampling of a random field that is defined on $\mathbb{R}^d$, and use this to obtain a test for iso...

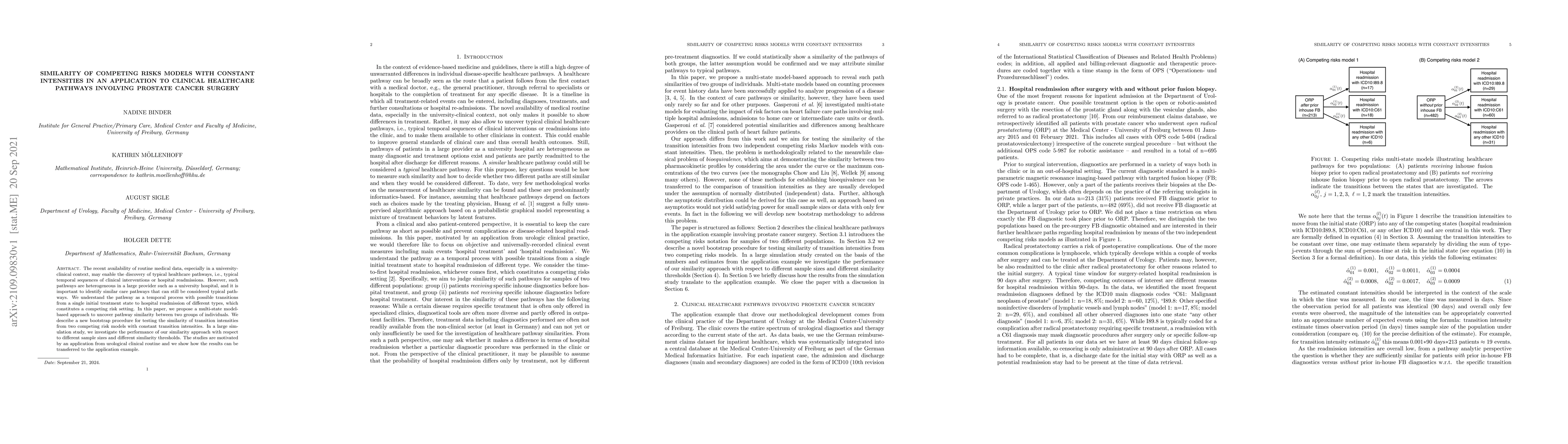

The identification of similar patient pathways is a crucial task in healthcare analytics. A flexible tool to address this issue are parametric competing risks models, where transition intensities ma...

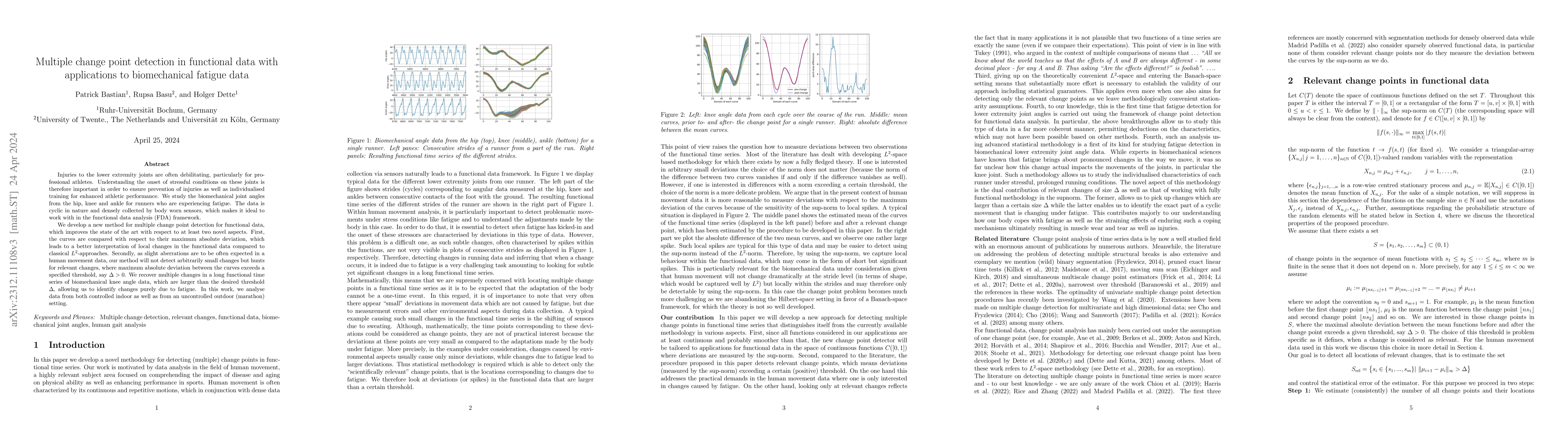

Injuries to the lower extremity joints are often debilitating, particularly for professional athletes. Understanding the onset of stressful conditions on these joints is therefore important in order...

The plausibility of the ``parallel trends assumption'' in Difference-in-Differences estimation is usually assessed by a test of the null hypothesis that the difference between the average outcomes o...

We prove that an $m$ out of $n$ bootstrap procedure for Chatterjee's rank correlation is consistent whenever asymptotic normality of Chatterjee's rank correlation can be established. In particular, ...

We propose a novel two-stage subsampling algorithm based on optimal design principles. In the first stage, we use a density-based clustering algorithm to identify an approximating design space for t...

In the case where the dimension of the data grows at the same rate as the sample size we prove a central limit theorem for the difference of a linear spectral statistic of the sample covariance and ...

In this paper we develop a novel bootstrap test for the comparison of two multinomial distributions. The two distributions are called {\it equivalent} or {\it similar} if a norm of the difference be...

Optimal designs are usually model-dependent and likely to be sub-optimal if the postulated model is not correctly specified. In practice, it is common that a researcher has a list of candidate model...

Many materials processes and properties depend on the anisotropy of the energy of grain boundaries, i.e.~on the fact that this energy is a function of the five geometric degrees of freedom (DOF) of ...

In this paper we compare two regression curves by measuring their difference by the area between the two curves, represented by their $L^1$-distance. We develop asymptotic confidence intervals for t...

Analyzing the covariance structure of data is a fundamental task of statistics. While this task is simple for low-dimensional observations, it becomes challenging for more intricate objects, such as...

For a given $p\times n$ data matrix $\textbf{X}_n$ with i.i.d. centered entries and a population covariance matrix $\bf{\Sigma}$, the corresponding sample precision matrix $\hat{\bf\Sigma}^{-1}$ is ...

This paper takes a different look on the problem of testing the mutual independence of the components of a high-dimensional vector. Instead of testing if all pairwise associations (e.g. all pairwise...

We present a general theory to quantify the uncertainty from imposing structural assumptions on the second-order structure of nonstationary Hilbert space-valued processes, which can be measured via ...

Statistical inference for large data panels is omnipresent in modern economic applications. An important benefit of panel analysis is the possibility to reduce noise and thus to guarantee stable inf...

For a spatiotemporal process $\{X_j(s,t) | ~s \in S~,~t \in T \}_{j =1, \ldots , n} $, where $S$ denotes the set of spatial locations and $T$ the time domain, we consider the problem of testing for ...

We develop methodology for testing hypotheses regarding the slope function in functional linear regression for time series via a reproducing kernel Hilbert space approach. In contrast to most of the...

Most of the popular dependence measures for two random variables $X$ and $Y$ (such as Pearson's and Spearman's correlation, Kendall's $\tau$ and Gini's $\gamma$) vanish whenever $X$ and $Y$ are inde...

Frequency domain methods form a ubiquitous part of the statistical toolbox for time series analysis. In recent years, considerable interest has been given to the development of new spectral methodol...

Data based materials science is the new promise to accelerate materials design. Especially in computational materials science, data generation can easily be automatized. Usually, the focus is on pro...

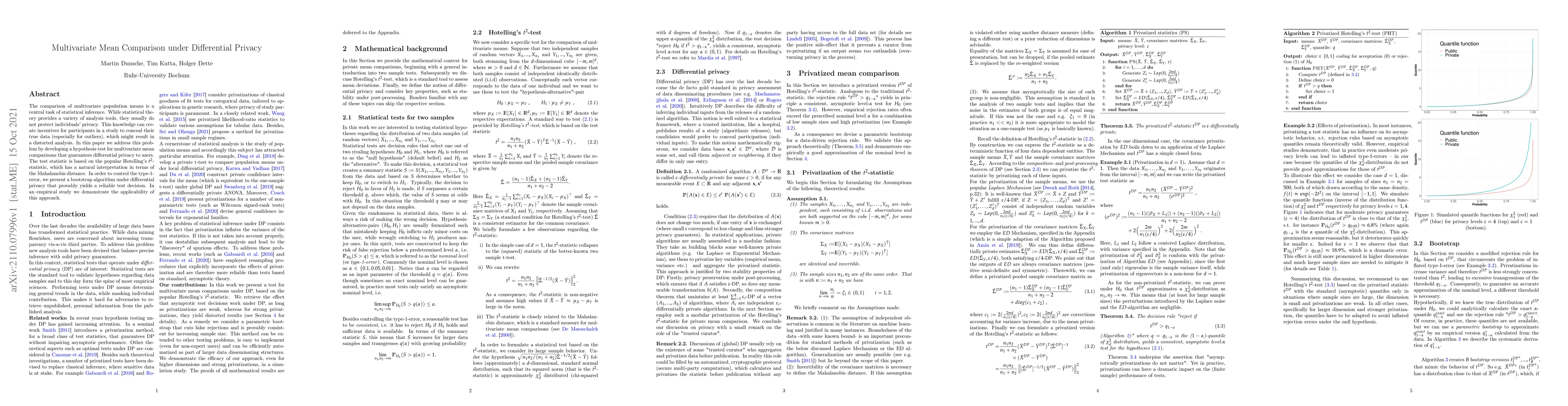

The comparison of multivariate population means is a central task of statistical inference. While statistical theory provides a variety of analysis tools, they usually do not protect individuals' pr...

Function-on-function linear regression is important for understanding the relationship between the response and the predictor that are both functions. In this article, we propose a reproducing kerne...

The recent availability of routine medical data, especially in a university-clinical context, may enable the discovery of typical healthcare pathways, i.e., typical temporal sequences of clinical in...

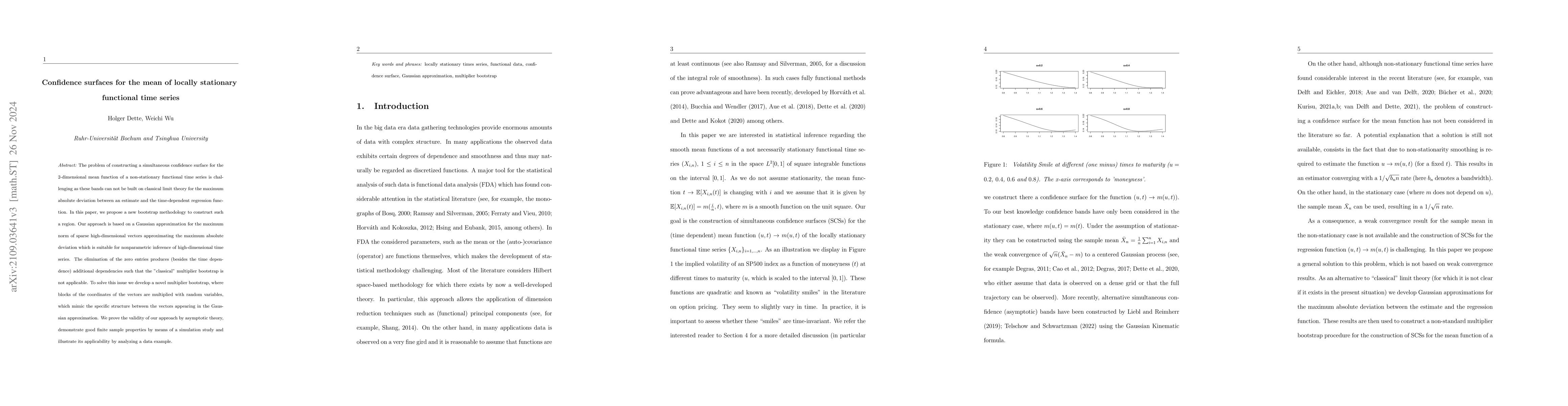

The problem of constructing a simultaneous confidence band for the mean function of a locally stationary functional time series $ \{ X_{i,n} (t) \}_{i = 1, \ldots, n}$ is challenging as these bands ...

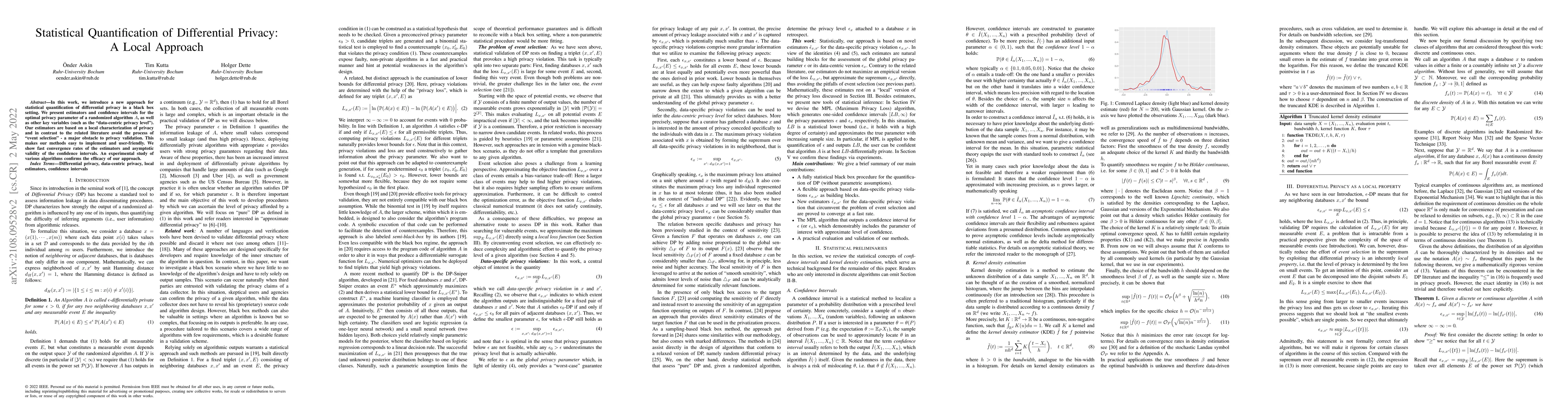

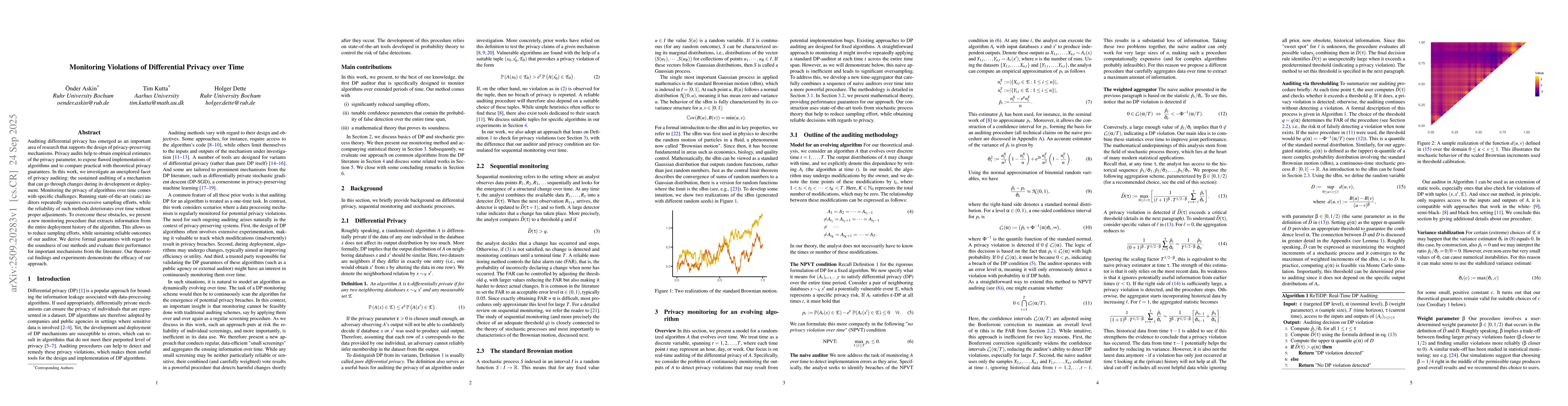

In this work, we introduce a new approach for statistical quantification of differential privacy in a black box setting. We present estimators and confidence intervals for the optimal privacy parame...

In this paper we consider the linear regression model $Y =S X+\varepsilon $ with functional regressors and responses. We develop new inference tools to quantify deviations of the true slope $S$ from...

Independent $p$-dimensional vectors with independent complex or real valued entries such that $\mathbb{E} [\mathbf{x}_i] = \mathbf{0}$, ${\rm Var } (\mathbf{x}_i) = \mathbf{I}_p$, $i=1, \ldots,n$, l...

For the class of Gauss-Markov processes we study the problem of asymptotic equivalence of the nonparametric regression model with errors given by the increments of the process and the continuous tim...

We consider the problem of constructing nonparametric undirected graphical models for high-dimensional functional data. Most existing statistical methods in this context assume either a Gaussian dis...

We consider the problem of designing experiments for the comparison of two regression curves describing the relation between a predictor and a response in two groups, where the data between and with...

In this note we consider the optimal design problem for estimating the slope of a polynomial regression with no intercept at a given point, say z. In contrast to previous work, which considers symme...

The Portmanteau test provides the vanilla method for detecting serial correlations in classical univariate time series analysis. The method is extended to the case of observations from a locally sta...

In this paper we propose statistical inference tools for the covariance operators of functional time series in the two sample and change point problem. In contrast to most of the literature the focu...

Change point detection in high dimensional data has found considerable interest in recent years. Most of the literature either designs methodology for a retrospective analysis, where the whole sampl...

In the common time series model $X_{i,n} = \mu (i/n) + \varepsilon_{i,n}$ with non-stationary errors we consider the problem of detecting a significant deviation of the mean function $\mu$ from a be...

We study the problem of testing the equivalence of functional parameters (such as the mean or variance function) in the two sample functional data problem. In contrast to previous work, which reduce...

Motivated by the need to statistically quantify differences between modern (complex) data-sets which commonly result as high-resolution measurements of stochastic processes varying over a continuum,...

The estimation of covariance operators of spatio-temporal data is in many applications only computationally feasible under simplifying assumptions, such as separability of the covariance into strict...

The determination of an optimal design for a given regression problem is an intricate optimization problem, especially for models with multivariate predictors. Design admissibility and invariance ar...

In this paper we develop statistical inference tools for high dimensional functional time series. We introduce a new concept of physical dependent processes in the space of square integrable functio...

The classical approach to analyze pharmacokinetic (PK) data in bioequivalence studies aiming to compare two different formulations is to perform noncompartmental analysis (NCA) followed by two one-s...

Classical change point analysis aims at (1) detecting abrupt changes in the mean of a possibly non-stationary time series and at (2) identifying regions where the mean exhibits a piecewise constant ...

We develop an estimator for the high-dimensional covariance matrix of a locally stationary process with a smoothly varying trend and use this statistic to derive consistent predictors in non-station...

Detecting structural changes in functional data is a prominent topic in statistical literature. However not all trends in the data are important in applications, but only those of large enough influ...

Clinical trials often aim to compare a new drug with a reference treatment in terms of efficacy and/or toxicity depending on covariates such as, for example, the dose level of the drug. Equivalence ...

This paper deals with two-sample tests for functional time series data, which have become widely available in conjunction with the advent of modern complex observation systems. Here, particular inte...

This article studies the problem whether two convex (concave) regression functions modelling the relation between a response and covariate in two samples differ by a shift in the horizontal and/or v...

Optimal portfolio selection problems are determined by the (unknown) parameters of the data generating process. If an investor wants to realise the position suggested by the optimal portfolios, he/s...

We consider the problem of predicting values of a random process or field satisfying a linear model $y(x)=\theta^\top f(x) + \varepsilon(x)$, where errors $\varepsilon(x)$ are correlated. This is a ...

In a seminal paper \cite{studden1968} characterized $c$-optimal designs in regression models, where the regression functions form a Chebyshev system. He used these results to determine the optimal d...

We propose a new sequential monitoring scheme for changes in the parameters of a multivariate time series. In contrast to procedures proposed in the literature which compare an estimator from the tr...

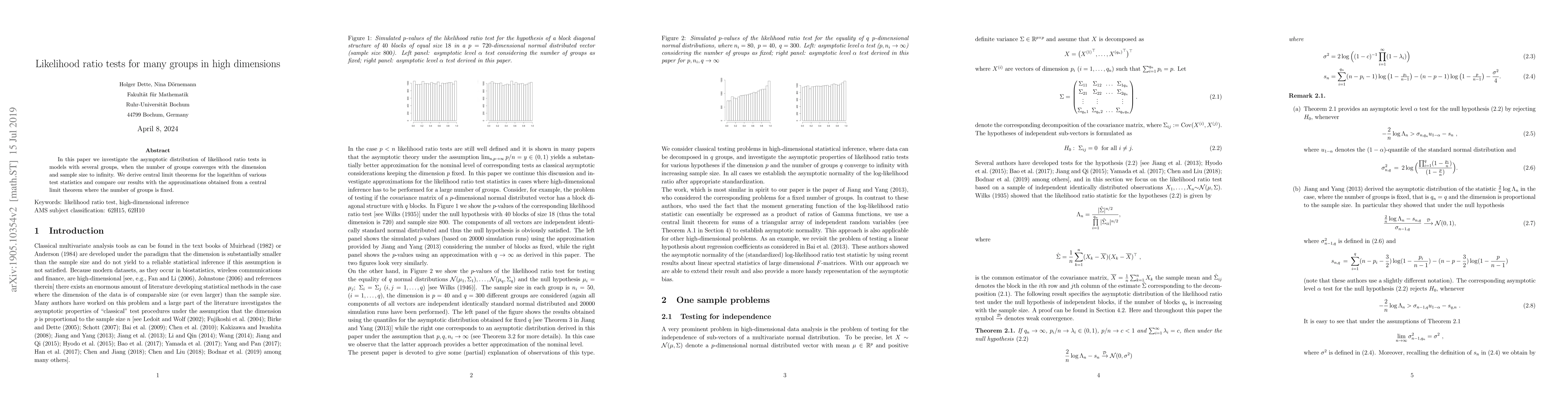

In this paper we investigate the asymptotic distribution of likelihood ratio tests in models with several groups, when the number of groups converges with the dimension and sample size to infinity. ...

In this paper we construct optimal designs for frequentist model averaging estimation. We derive the asymptotic distribution of the model averaging estimate with fixed weights in the case where the ...

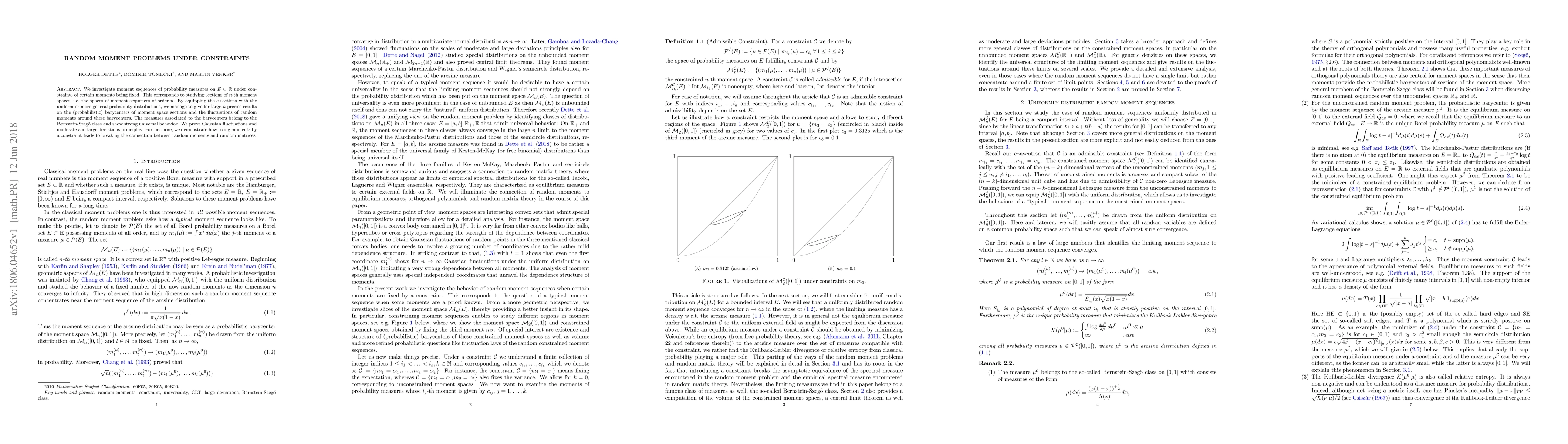

We investigate moment sequences of probability measures on $E\subset\mathbb{R}$ under constraints of certain moments being fixed. This corresponds to studying sections of $n$-th moment spaces, i.e. ...

We propose a new measure for stationarity of a functional time series, which is based on an explicit representation of the $L^2$-distance between the spectral density operator of a non-stationary pr...

In this paper new tests for the independence of two high-dimensional vectors are investigated. We consider the case where the dimension of the vectors increases with the sample size and propose mult...

This paper investigates the problem of detecting relevant change points in the mean vector, say $\mu_t =(\mu_{1,t},\ldots ,\mu_{d,t})^T$ of a high dimensional time series $(Z_t)_{t\in \mathbb{Z}}$. ...

In this paper we take a different look on the problem of testing the independence of two infinite dimensional random variables using the distance correlation. Instead of testing if the distance correl...

We consider the problem of detecting gradual changes in the sequence of mean functions from a not necessarily stationary functional time series. Our approach is based on the maximum deviation (calcula...

Subsampling is one of the popular methods to balance statistical efficiency and computational efficiency in the big data era. Most approaches aim at selecting informative or representative sample poin...

Chatterjee's correlation coefficient has recently been proposed as a new association measure for bivariate random vectors that satisfies a number of desirable properties. Among these properties is the...

We consider a linear regression model with complex-valued response and predictors from a compact and connected Lie group. The regression model is formulated in terms of eigenfunctions of the Laplace-B...

Testing for change points in sequences of high-dimensional covariance matrices is an important and equally challenging problem in statistical methodology with applications in various fields. Motivated...

Multivariate locally stationary functional time series provide a flexible framework for modeling complex data structures exhibiting both temporal and spatial dependencies while allowing for time-varyi...

A novel method for sequential outlier detection in non-stationary time series is proposed. The method tests the null hypothesis of ``no outlier'' at each time point, addressing the multiple testing pr...

We develop uniform confidence bands for the mean function of stationary time series as a post-hoc analysis of multiple change point detection in functional time series. In particular, the methodology ...

In this paper we propose new methods to statistically assess $f$-Differential Privacy ($f$-DP), a recent refinement of differential privacy (DP) that remedies certain weaknesses of standard DP (includ...

Cryptographic research takes software timing side channels seriously. Approaches to mitigate them include constant-time coding and techniques to enforce such practices. However, recent attacks like Me...

Bootstrap is a common tool for quantifying uncertainty in data analysis. However, besides additional computational costs in the application of the bootstrap on massive data, a challenging problem in b...

In many change point problems it is reasonable to assume that compared to a benchmark at a given time point $t_0$ the properties of the observed stochastic process change gradually over time for $t >t...

In the framework of semiparametric distribution regression, we consider the problem of comparing the conditional distribution functions corresponding to two samples. In contrast to testing for exact e...

We propose a two-sample test for covariance matrices in the high-dimensional regime, where the dimension diverges proportionally to the sample size. Our hybrid test combines a Frobenius-norm-based sta...

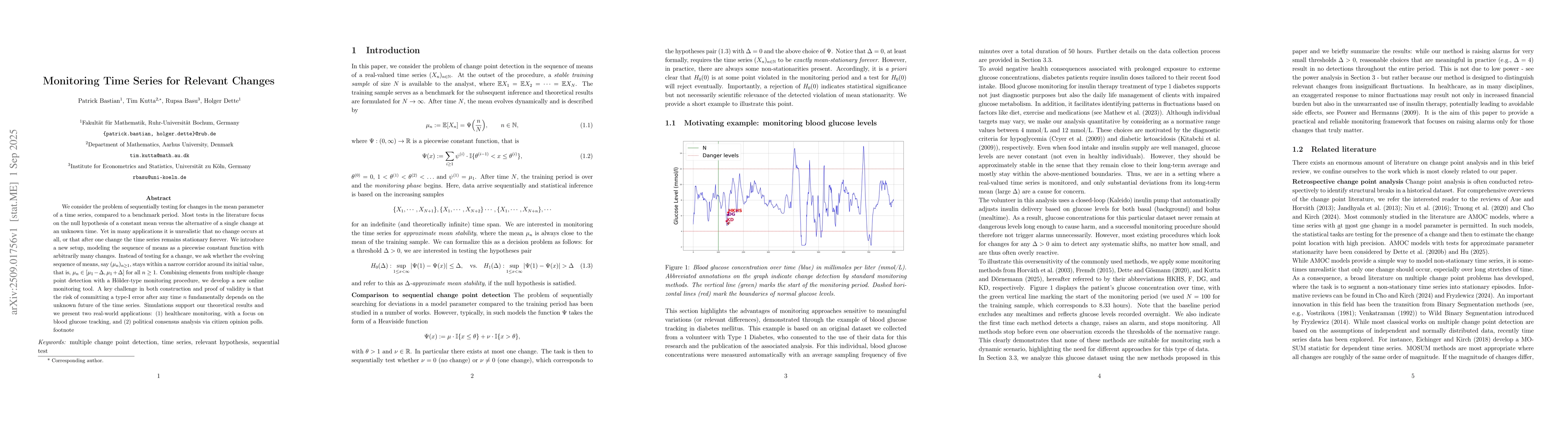

We consider the problem of sequentially testing for changes in the mean parameter of a time series, compared to a benchmark period. Most tests in the literature focus on the null hypothesis of a const...

We consider the change point testing problem for high-dimensional time series. Unlike conventional approaches, where one tests whether the difference $\delta$ of the mean vectors before and after the ...

In this paper we develop pivotal inference for the final (FPE) and relative final prediction error (RFPE) of linear forecasts in stationary processes. Our approach is based on a novel self-normalizing...

Auditing differential privacy has emerged as an important area of research that supports the design of privacy-preserving mechanisms. Privacy audits help to obtain empirical estimates of the privacy p...

Most of the work on checking spherical symmetry assumptions on the distribution of the $p$-dimensional random vector $Y$ has its focus on statistical tests for the null hypothesis of exact spherical s...

We investigate the problem of detecting dependencies between the components of a high-dimensional vector. Our approach advances the existing literature in two important respects. First, we consider th...

We study the problem of detecting and localizing multiple changes in the mean parameter of a Banach space-valued time series. The goal is to construct a collection of narrow confidence intervals, each...

Assessing whether two patient populations exhibit comparable event dynamics is essential for evaluating treatment equivalence, pooling data across cohorts, or comparing clinical pathways across hospit...

Second-order characteristics including covariance and spectral density functions are fundamentally important for both statistical applications and theoretical analysis in functional time series. In th...

Panels with large time $(T)$ and cross-sectional $(N)$ dimensions are a key data structure in social sciences and other fields. A central question in panel data analysis is whether to pool data across...

Change-point detection and locally stationary time series modeling are two major approaches for the analysis of non-stationary data. The former aims to identify stationary phases by detecting abrupt c...

Dette, Siburg, and Stoimenov (2013) introduced a copula-based measure of dependence, which implies independence if it vanishes and is equal to 1 if one variable is a measurable function of the other. ...

A crucial assumption to reduce computational complexity in spatial-temporal data analysis is separability, which factors the covariance structure into a purely spatial and a purely temporal component....

The Admixture Model describes genetic marker data by representing each individual's genome as a mixture of contributions from $K$ ancestral populations, with the individual admixture vector summarizin...

We develop a spectral based coefficient of determination to measure how well the spectral density of a stationary process is represented by the class of MA($q$) models. Using periodogram-based estimat...