Academic Profile

Statistics

Similar Authors

Papers on arXiv

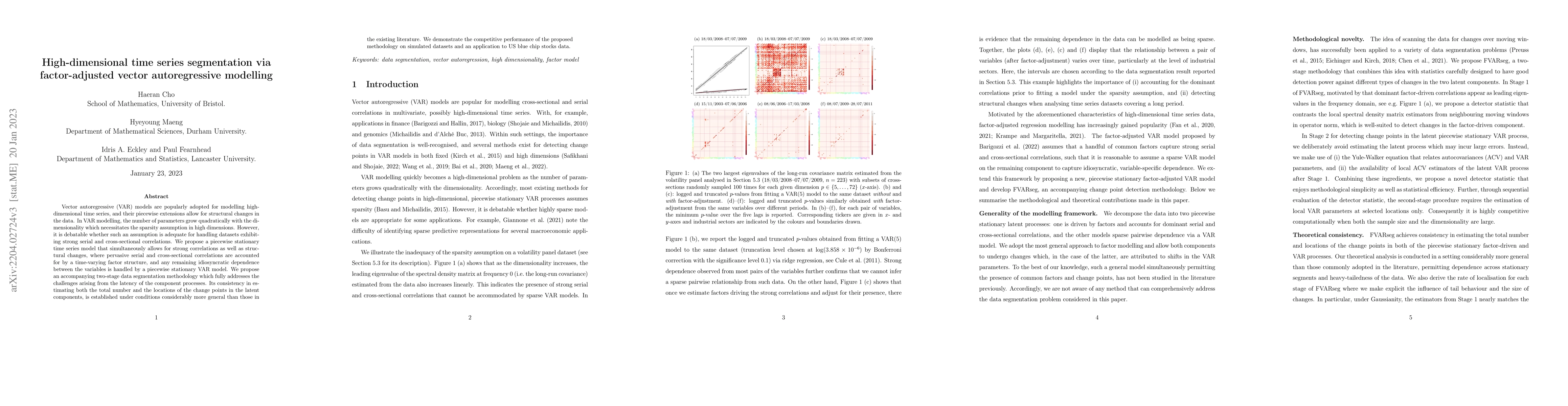

Vector autoregressive (VAR) models are popularly adopted for modelling high-dimensional time series, and their piecewise extensions allow for structural changes in the data. In VAR modelling, the nu...

There is increasing interest in detecting collective anomalies: potentially short periods of time where the features of data change before reverting back to normal behaviour. We propose a new method...

We propose TrendSegment, a methodology for detecting multiple change-points corresponding to linear trend changes in one dimensional data. A core ingredient of TrendSegment is a new Tail-Greedy Unba...

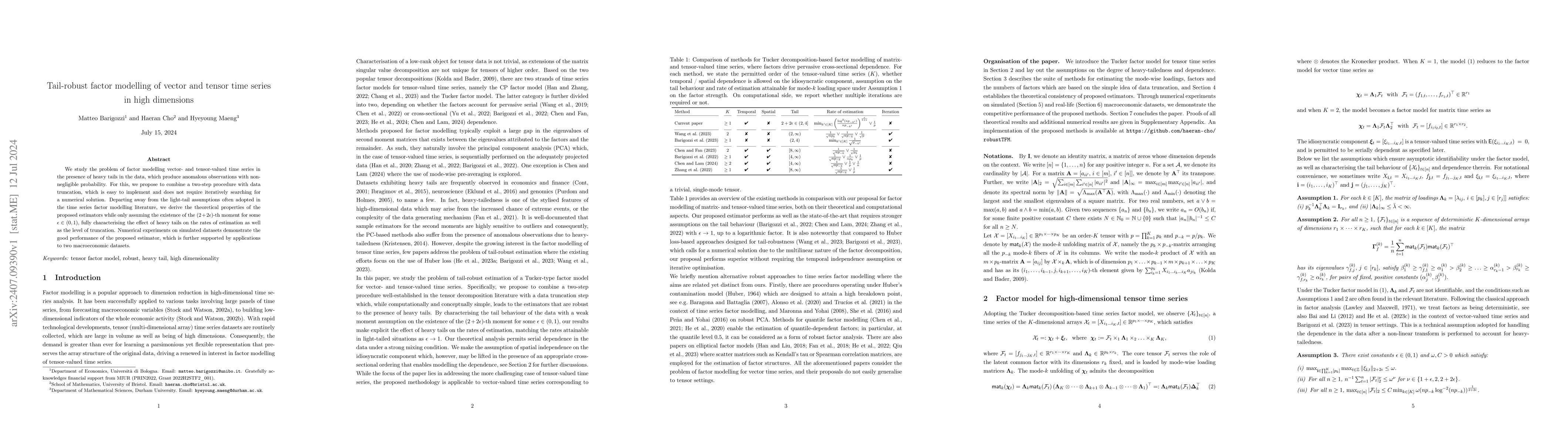

We study the problem of factor modelling vector- and tensor-valued time series in the presence of heavy tails in the data, which produce anomalous observations with non-negligible probability. For thi...