Academic Profile

Statistics

Similar Authors

Papers on arXiv

The hyperbolic network models exhibit very fundamental and essential features, like small-worldness, scale-freeness, high-clustering coefficient, and community structure. In this paper, we comprehensi...

This paper highlights the significance of mesoscale structures, particularly the core-periphery structure, in financial networks for portfolio optimization. We build portfolios of stocks belonging t...

Core periphery structure represents a meso-scale structure in networks, characterized by a dense interconnection of core nodes and sparse connections among peripheral nodes. In this paper, we introduc...

In finance, Random Matrix Theory (RMT) is an important tool for filtering out noise from large datasets, revealing true correlations among stocks, enhancing risk management and portfolio optimization....

Meso-scale structures, such as core-periphery (CP) and community structure, have attracted significant attention in modern network science. While communities are characterized by dense intra-group and...

This study investigates how financial market structure reorganizes during the COVID-19 crash using a conditional p-threshold mutual information (MI) based Minimum Spanning Tree (MST) framework. We ana...

We identify a robust structural signature of stock markets during exogenous shock events by analyzing collective return dynamics across G5 countries. Using Random Matrix Theory, we introduce the compl...

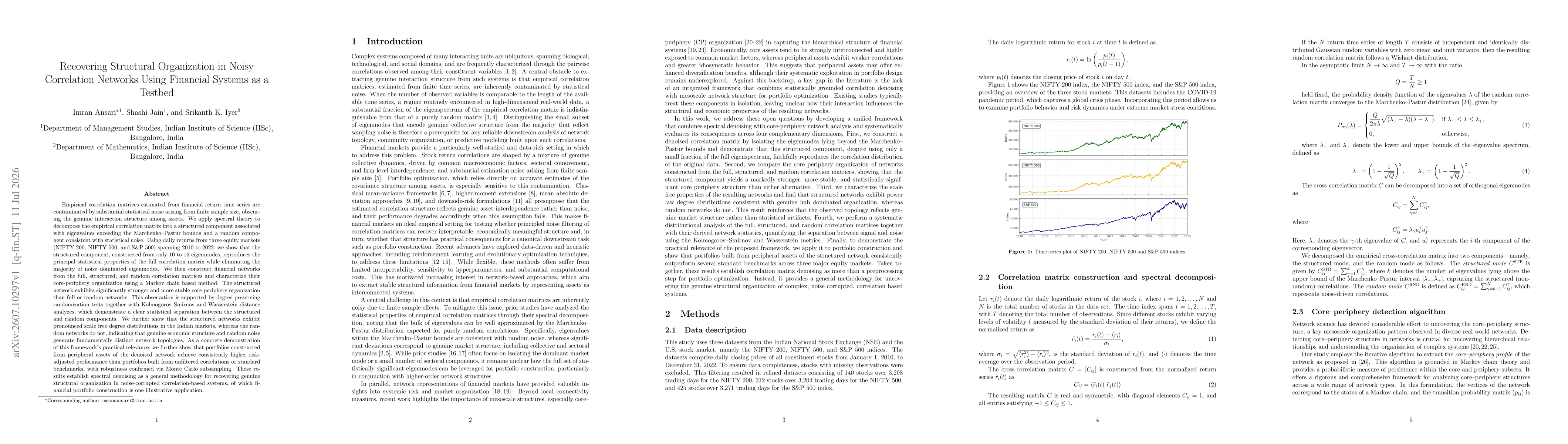

Empirical correlation matrices estimated from financial return time series are contaminated by statistical noise arising from finite sample size, obscuring genuine interactions among assets. We apply ...