Academic Profile

Statistics

Similar Authors

Papers on arXiv

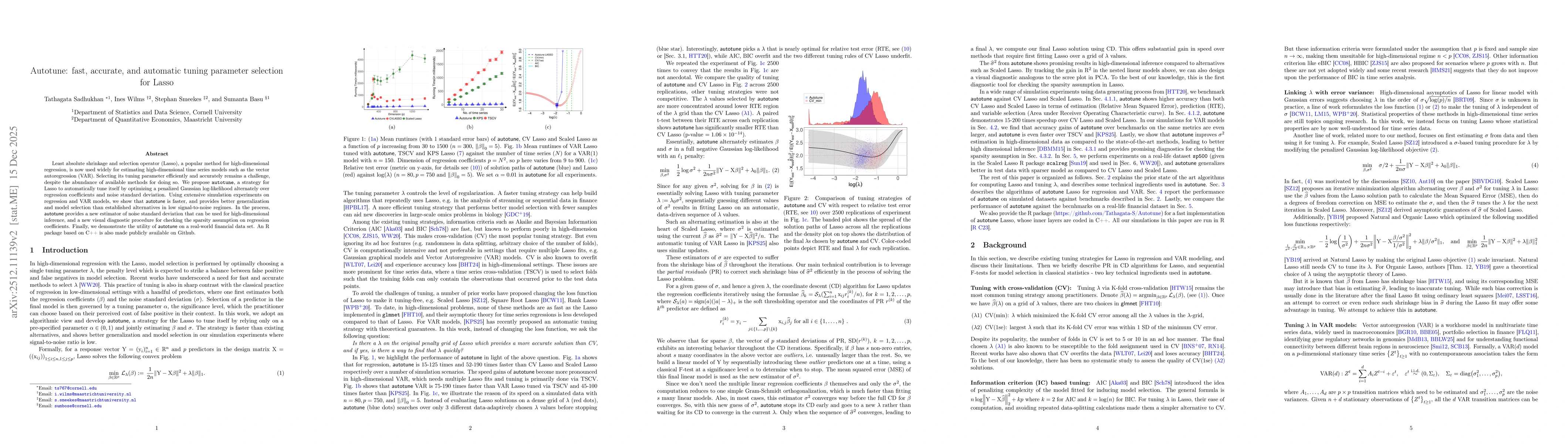

Vector autoregression (VAR) is a fundamental tool for modeling multivariate time series. However, as the number of component series is increased, the VAR model becomes overparameterized. Several aut...

Vector AutoRegressive Moving Average (VARMA) models form a powerful and general model class for analyzing dynamics among multiple time series. While VARMA models encompass the Vector AutoRegressive ...

We propose a framework for the analysis of transmission channels in a large class of dynamic models. To this end, we formulate our approach both using graph theory and potential outcomes, which we s...

Platform businesses operate on a digital core and their decision making requires high-dimensional accurate forecast streams at different levels of cross-sectional (e.g., geographical regions) and te...

Data stream forecasts are essential inputs for decision making at digital platforms. Machine learning algorithms are appealing candidates to produce such forecasts. Yet, digital platforms require a ...

Accurate forecasts for day-ahead photovoltaic (PV) power generation are crucial to support a high PV penetration rate in the local electricity grid and to assure stability in the grid. We use state-...

Compositional data are characterized by the fact that their elemental information is contained in simple pairwise logratios of the parts that constitute the composition. While pairwise logratios are...

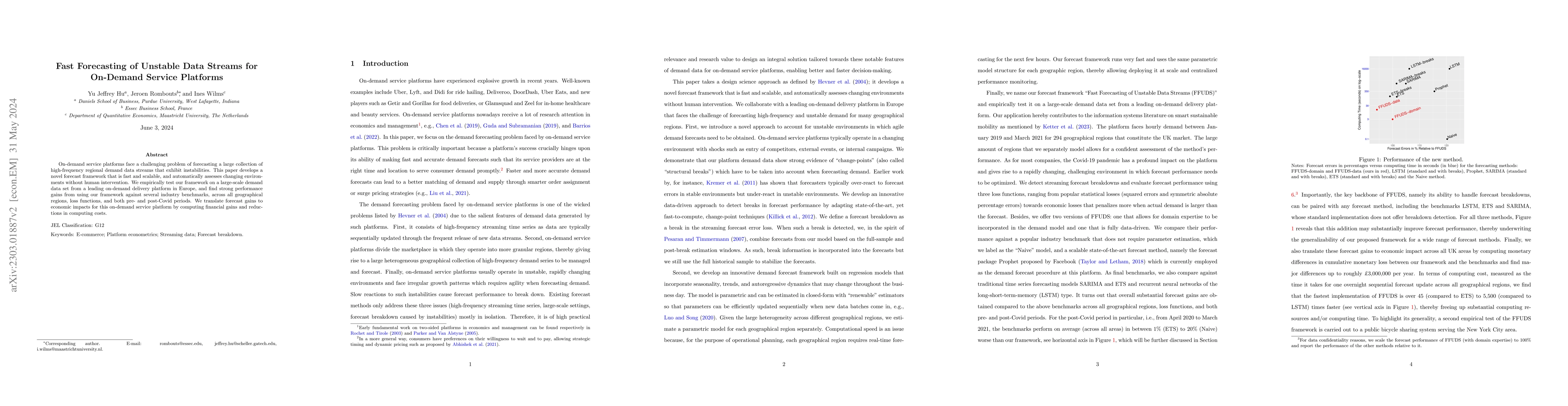

On-demand service platforms face a challenging problem of forecasting a large collection of high-frequency regional demand data streams that exhibit instabilities. This paper develops a novel foreca...

We introduce a high-dimensional multiplier bootstrap for time series data based capturing dependence through a sparsely estimated vector autoregressive model. We prove its consistency for inference ...

Reverse Unrestricted MIxed DAta Sampling (RU-MIDAS) regressions are used to model high-frequency responses by means of low-frequency variables. However, due to the periodic structure of RU-MIDAS reg...

The precision matrix that encodes conditional linear dependency relations among a set of variables forms an important object of interest in multivariate analysis. Sparse estimation procedures for pr...

In this paper, we estimate impulse responses by local projections in high-dimensional settings. We use the desparsified (de-biased) lasso to estimate the high-dimensional local projections, while le...

Despite the increasing integration of the global economic system, anti-dumping measures are a common tool used by governments to protect their national economy. In this paper, we propose a methodolo...

Faced with changing markets and evolving consumer demands, beef industries are investing in grading systems to maximise value extraction throughout their entire supply chain. The Meat Standards Aust...

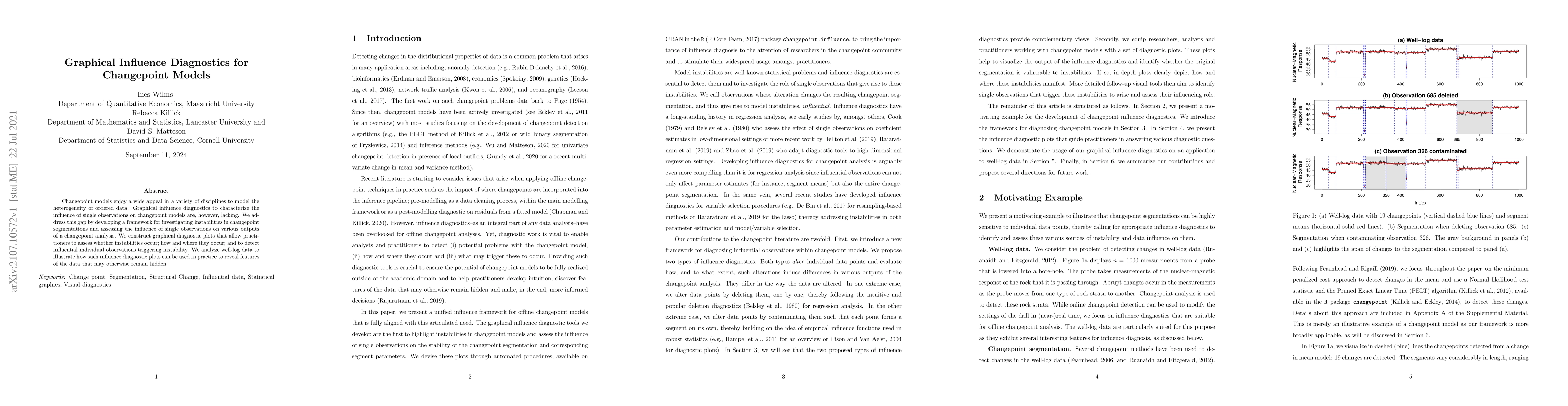

Changepoint models enjoy a wide appeal in a variety of disciplines to model the heterogeneity of ordered data. Graphical influence diagnostics to characterize the influence of single observations on...

Mixed-frequency Vector AutoRegressions (MF-VAR) model the dynamics between variables recorded at different frequencies. However, as the number of series and high-frequency observations per low-frequ...

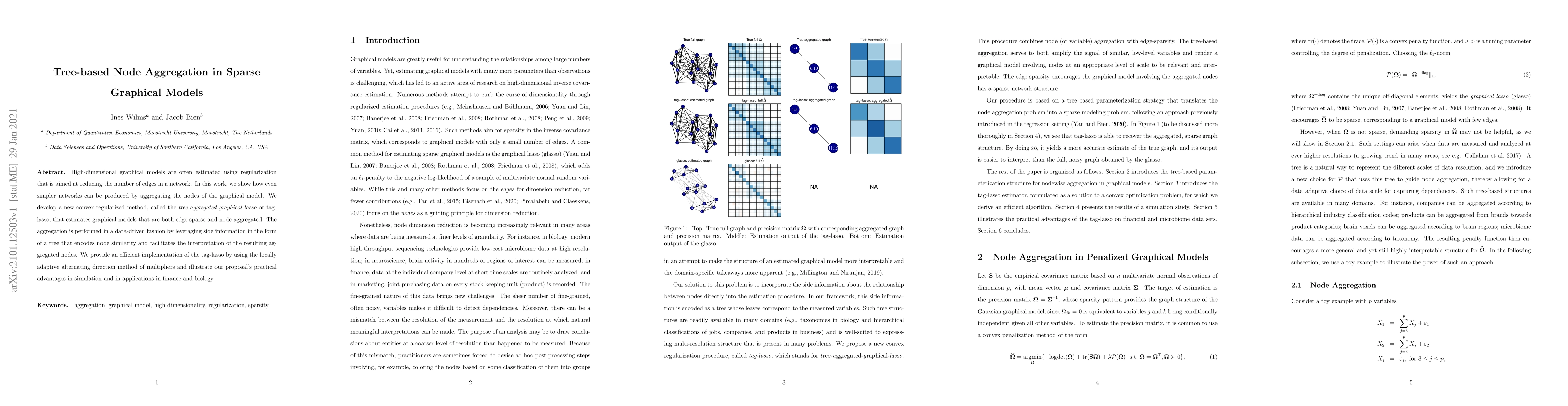

High-dimensional graphical models are often estimated using regularization that is aimed at reducing the number of edges in a network. In this work, we show how even simpler networks can be produced...

Unit root tests form an essential part of any time series analysis. We provide practitioners with a single, unified framework for comprehensive and reliable unit root testing in the R package bootUR...

In this paper we develop valid inference for high-dimensional time series. We extend the desparsified lasso to a time series setting under Near-Epoch Dependence (NED) assumptions allowing for non-Ga...

Sparse and outlier-robust Principal Component Analysis (PCA) has been a very active field of research recently. Yet, most existing methods apply PCA to a single dataset whereas multi-source data-i.e. ...

This paper proposes a Matrix Error Correction Model to identify cointegration relations in matrix-valued time series. We hereby allow separate cointegrating relations along the rows and columns of the...

Reduced-rank regressions are powerful tools used to identify co-movements within economic time series. However, this task becomes challenging when we observe matrix-valued time series, where each dime...

Matrix completion has gained considerable interest in recent years. The goal of matrix completion is to predict the unknown entries of a partially observed matrix using its known entries. Although com...

Machine learning models are widely recognized for their strong performance in forecasting. To keep that performance in streaming data settings, they have to be monitored and frequently re-trained. Thi...

Are data groups which are pre-defined by expert opinions or medical diagnoses corresponding to groups based on statistical modeling? For which reason might observations be inconsistent? This contribut...

We introduce a panel data model where coefficients vary both over time and the cross-section. Slope coefficients change smoothly over time and follow a latent group structure, being homogeneous within...

We propose a pseudo-structural framework for analyzing contemporaneous co-movements in reduced-rank matrix autoregressive (RRMAR) models. Unlike conventional vector-autoregressive (VAR) models that wo...

State-space models (SSMs) provide a flexible framework for modelling time series data, but their reliance on Gaussian error assumptions makes them highly sensitive to outliers. We propose a robust est...

Least absolute shrinkage and selection operator (Lasso), a popular method for high-dimensional regression, is now used widely for estimating high-dimensional time series models such as the vector auto...

Forecast reconciliation has become key to improving the accuracy and coherence of forecasts for linearly constrained multiple time series, such as hierarchical and grouped series. Yet, comprehensive s...

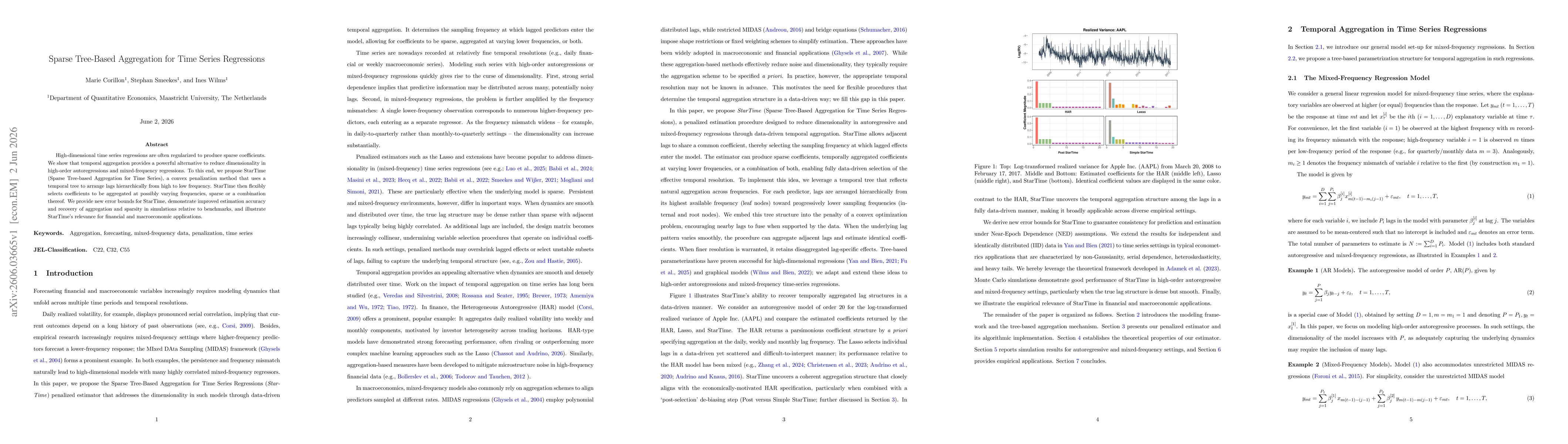

High-dimensional time series regressions are often regularized to produce sparse coefficients. We show that temporal aggregation provides a powerful alternative to reduce dimensionality in high-order ...