Academic Profile

Statistics

Similar Authors

Papers on arXiv

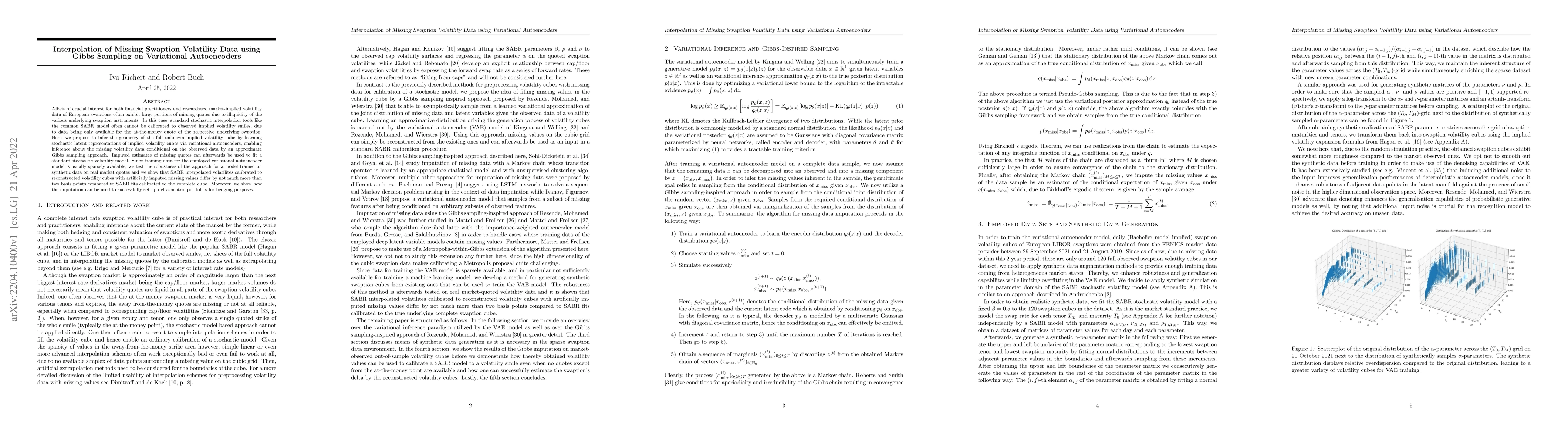

Albeit of crucial interest for both financial practitioners and researchers, market-implied volatility data of European swaptions often exhibit large portions of missing quotes due to illiquidity of...

Estimation of the value-at-risk (VaR) of a large portfolio of assets is an important task for financial institutions. As the joint log-returns of asset prices can often be projected to a latent spac...

This paper is devoted to parameter estimation for partially observed polynomial state space models. This class includes discretely observed affine or more generally polynomial Markov processes. The po...

This paper is devoted to filtering, smoothing, and prediction of polynomial processes that are partially observed. These problems are known to allow for an explicit solution in the simpler case of lin...