Academic Profile

Statistics

Similar Authors

Papers on arXiv

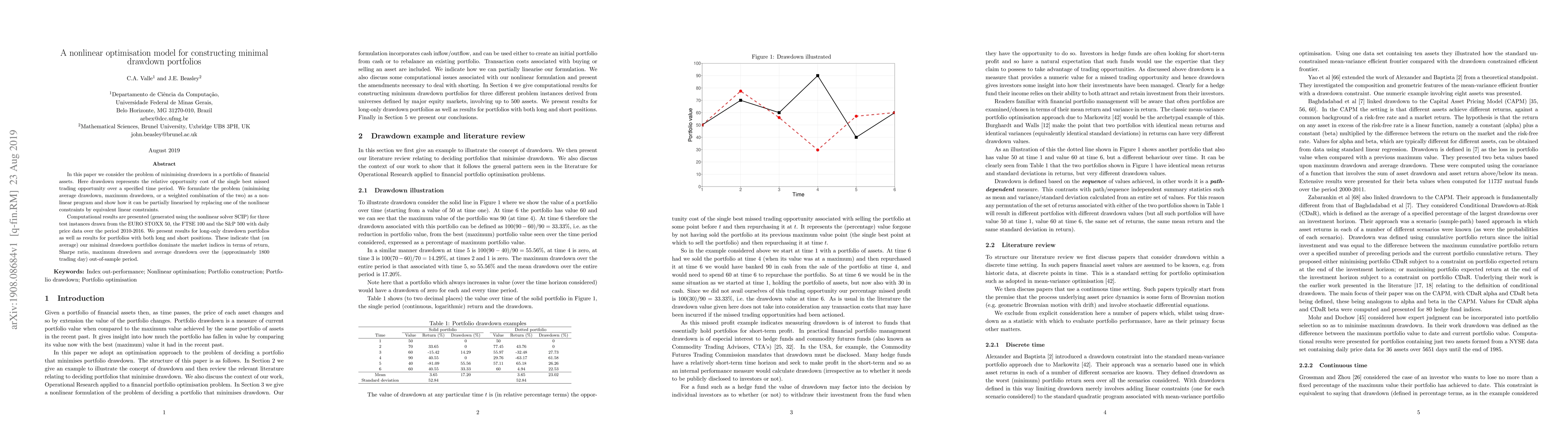

In this paper we consider the problem of minimising drawdown in a portfolio of financial assets. Here drawdown represents the relative opportunity cost of the single best missed trading opportunity ...

We consider a class of problems related to variable knockout, where knockout means set a variable to zero. Given an optimisation problem formulated as a zero-one integer program the question we cons...

An index tracker is a passive investment reproducing the return and risk of a market index, an enhanced index tracker offers a return greater than the index. We consider the selection of a portfolio o...