Academic Profile

Statistics

Similar Authors

Papers on arXiv

We propose new goodness-of-fit tests for the Poisson distribution. The testing procedure entails fitting a weighted Poisson distribution, which has the Poisson as a special case, to observed data. B...

We propose new goodness-of-fit tests for the Pareto type I distribution. These tests are based on a multiplicative version of the memoryless property which characterises this distribution. We presen...

Credit scorecards are models used for the modelling of the probability of default of clients. The decision to extend credit to an applicant, as well as the price of the credit, is often based on the...

In this paper we investigate the performance of a variety of estimation techniques for the scale and shape parameter of the Lomax distribution. These methods include traditional methods such as the ...

In this paper, we revisit the classical goodness-of-fit problems for univariate distributions; we propose a new testing procedure based on a characterisation of the uniform distribution. Asymptotic ...

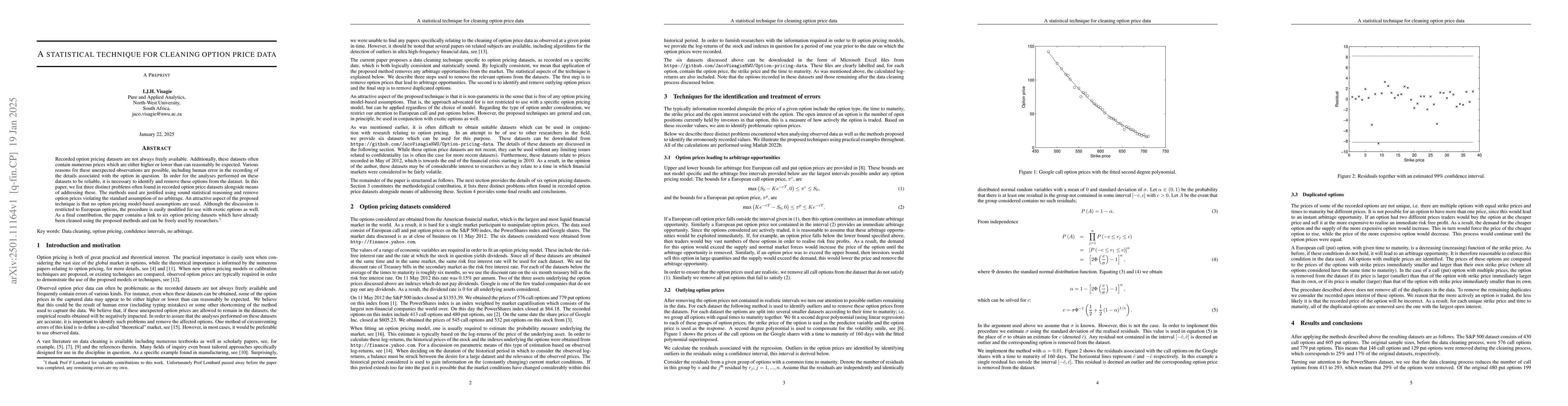

Recorded option pricing datasets are not always freely available. Additionally, these datasets often contain numerous prices which are either higher or lower than can reasonably be expected. Various r...