Academic Profile

Statistics

Similar Authors

Papers on arXiv

State-space models are widely used in many applications. In the domain of count data, one such example is the model proposed by Harvey and Fernandes (1989). Unlike many of its parameter-driven alter...

The collective risk model (CRM) for frequency and severity is an important tool for retail insurance ratemaking, macro-level catastrophic risk forecasting, as well as operational risk in banking reg...

Traditional credibility analysis of risks in insurance is based on the random effects model, where the heterogeneity across the policyholders is assumed to be time-invariant. One popular extension i...

Copulas allow a flexible and simultaneous modeling of complicated dependence structures together with various marginal distributions. Especially if the density function can be represented as the pro...

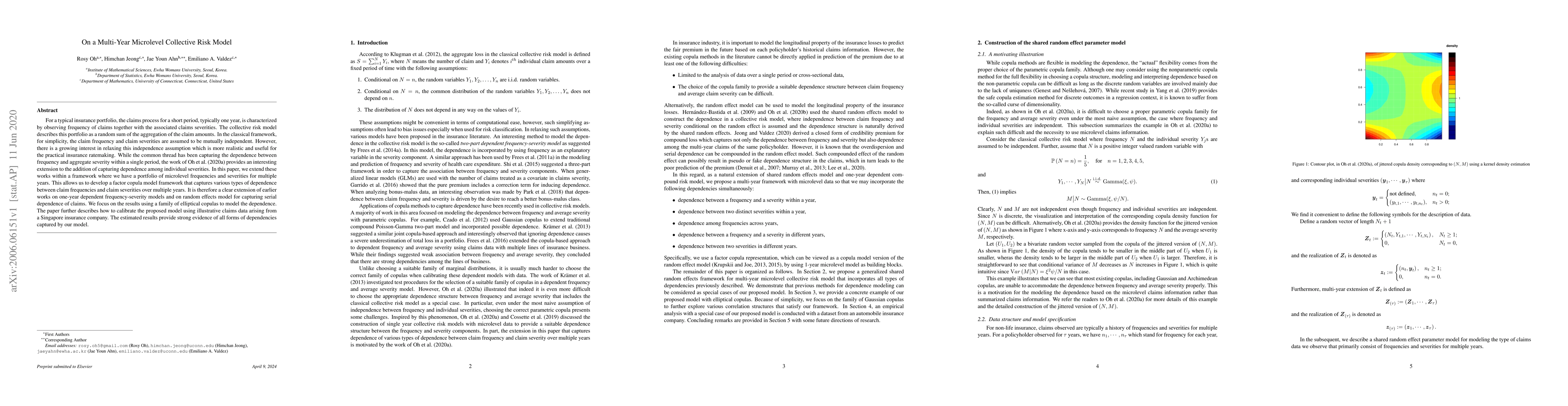

For a typical insurance portfolio, the claims process for a short period, typically one year, is characterized by observing frequency of claims together with the associated claims severities. The co...

In auto insurance, a Bonus-Malus System (BMS) is commonly used as a posteriori risk classification mechanism to set the premium for the next contract period based on a policyholder's claim history. ...

Typical risk classification procedure in insurance is consists of a priori risk classification determined by observable risk characteristics, and a posteriori risk classification where the premium i...

The bonus-malus system (BMS) is a widely used premium adjustment mechanism based on policyholder's claim history. Most auto insurance BMSs assume that policyholders in the same bonus-malus (BM) leve...

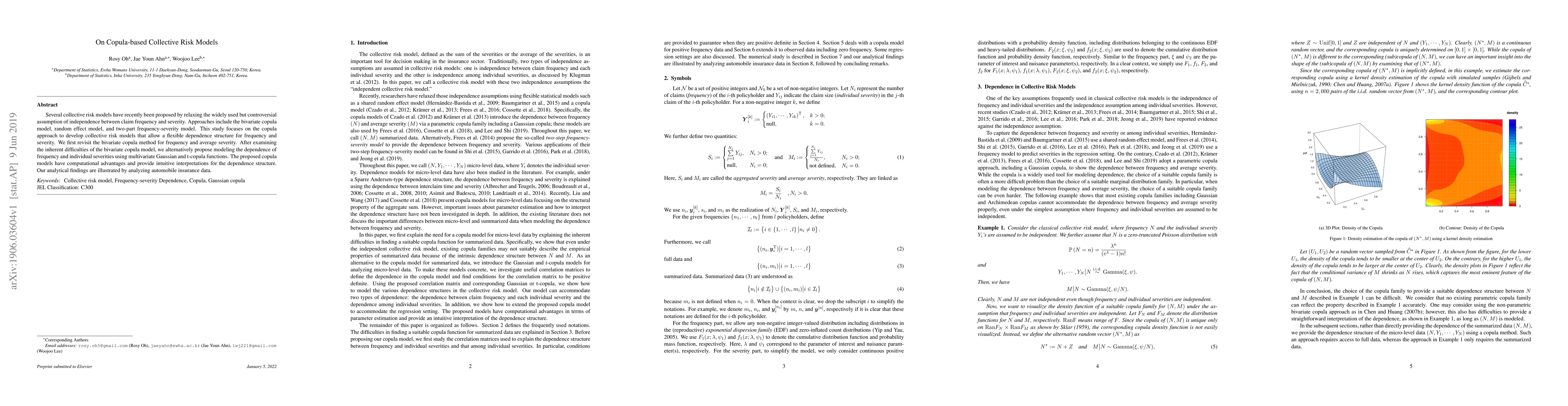

Several collective risk models have recently been proposed by relaxing the widely used but controversial assumption of independence between claim frequency and severity. Approaches include the bivar...

State-space models are popular models in econometrics. Recently, these models have gained some popularity in the actuarial literature. The best known state-space models are of Kalman-filter type. Thes...

Integer-valued generalized autoregressive conditional heteroskedastic (INGARCH) models are a popular framework for modeling serial dependence in count time-series. While convenient for modeling, predi...

Standard count models such as the Poisson and Negative Binomial models often fail to capture the large proportion of zero claims commonly observed in insurance data. To address such issue of excessive...