Academic Profile

Statistics

Similar Authors

Papers on arXiv

We analyze the problem of optimally sharing risk using allocations that exhibit counter-monotonicity, the most extreme form of negative dependence. Counter-monotonic allocations take the form of eit...

We systematically study pairwise counter-monotonicity, an extremal notion of negative dependence. A stochastic representation and an invariance property are established for this dependence structure...

We address the problem of sharing risk among agents with preferences modelled by a general class of comonotonic additive and law-based functionals that need not be either monotone or convex. Such fu...

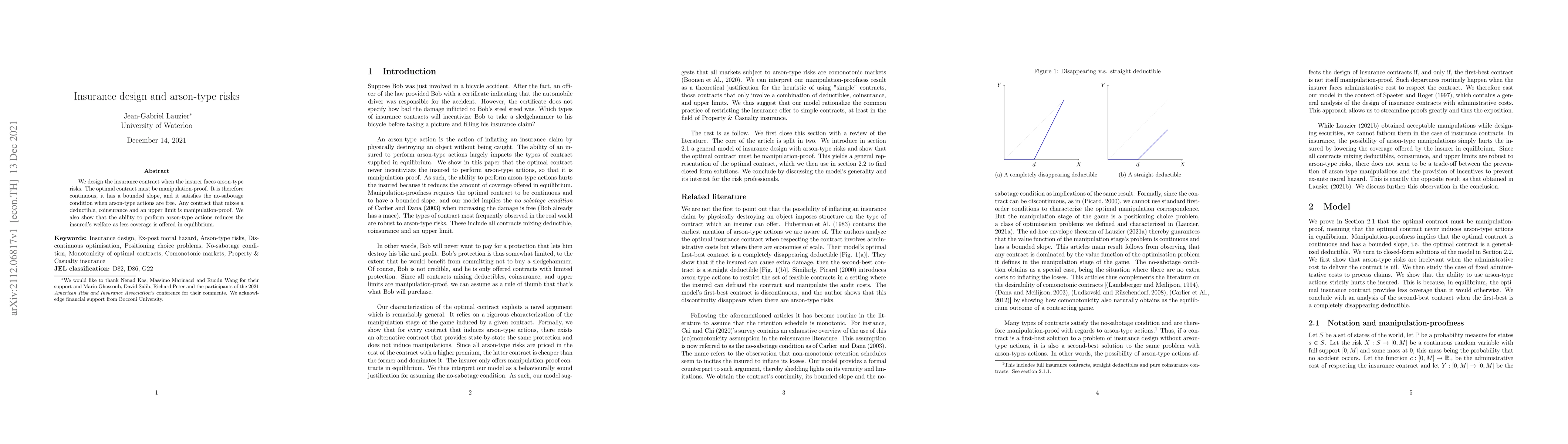

We design the insurance contract when the insurer faces arson-type risks. The optimal contract must be manipulation-proof. It is therefore continuous, it has a bounded slope, and it satisfies the no...

This article examines differentiability properties of the value function of positioning choice problems, a class of optimisation problems in finite-dimensional Euclidean spaces. We show that positio...

We examine the trade-off between the provision of incentives to exert costly effort (ex-ante moral hazard) and the incentives needed to prevent the agent from manipulating the profit observed by the...

Regulatory and contractual constraints on individual exposures are standard in insurance and reinsurance markets, but a poorly designed constraint can distort the economic incentives of risk-averse ag...

While risk pooling lowers the total cost of risk, efficiency alone does not make a pool viable. Participants need terms that ensure their participation, that are immune to subgroups breaking away, and...