Academic Profile

Statistics

Similar Authors

Papers on arXiv

We present a general framework for the estimation of corporate default based on a firm's capital structure, when its assets are assumed to follow a pure jump L\'evy processes; this setup provides a ...

We provide closed-form pricing formulas for a wide variety of path-independent options, in the exponential L\'evy model driven by the Normal inverse Gaussian process. The results are obtained in bot...

We establish several closed pricing formula for various path-independent payoffs, under an exponential L\'evy model driven by the Variance Gamma process. These formulas take the form of quickly conv...

We derive new formulas for the price of the European call and put options in the Black-Scholes model, under the form of uniformly convergent series generalizing previously known approximations. We a...

We introduce and document a class of probability distributions, called bilateral generalized inverse Gaussian (BGIG) distributions, that are obtained by convolution of two generalized inverse Gaussian...

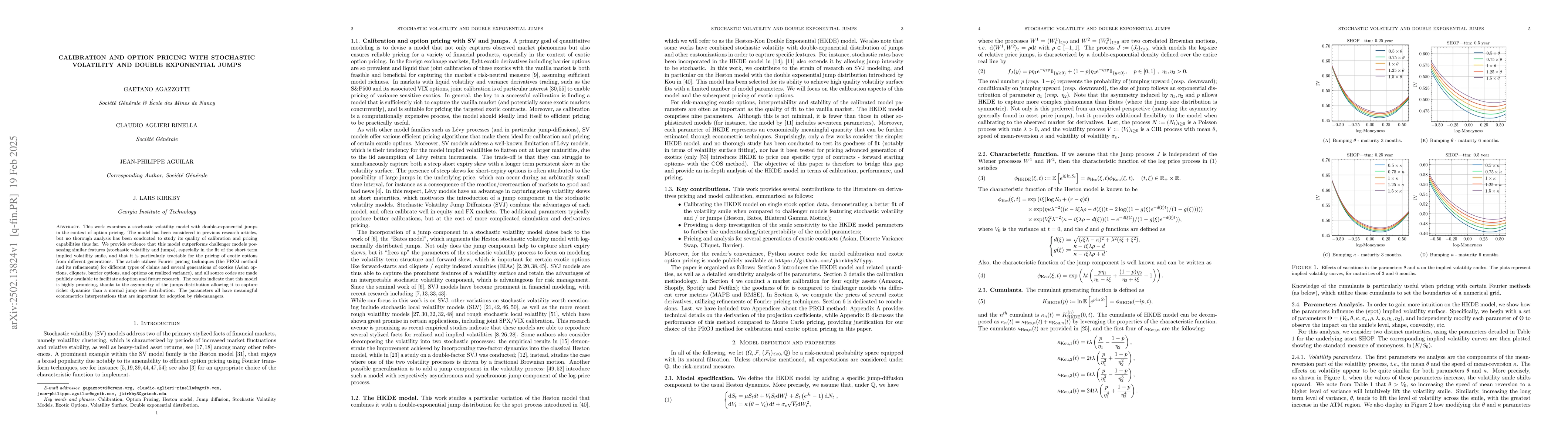

This work examines a stochastic volatility model with double-exponential jumps in the context of option pricing. The model has been considered in previous research articles, but no thorough analysis h...

We provide series expansions for the tempered stable densities and for the price of European-style contracts in the exponential L\'evy model driven by the tempered stable process. These formulas recov...