Academic Profile

Statistics

Similar Authors

Papers on arXiv

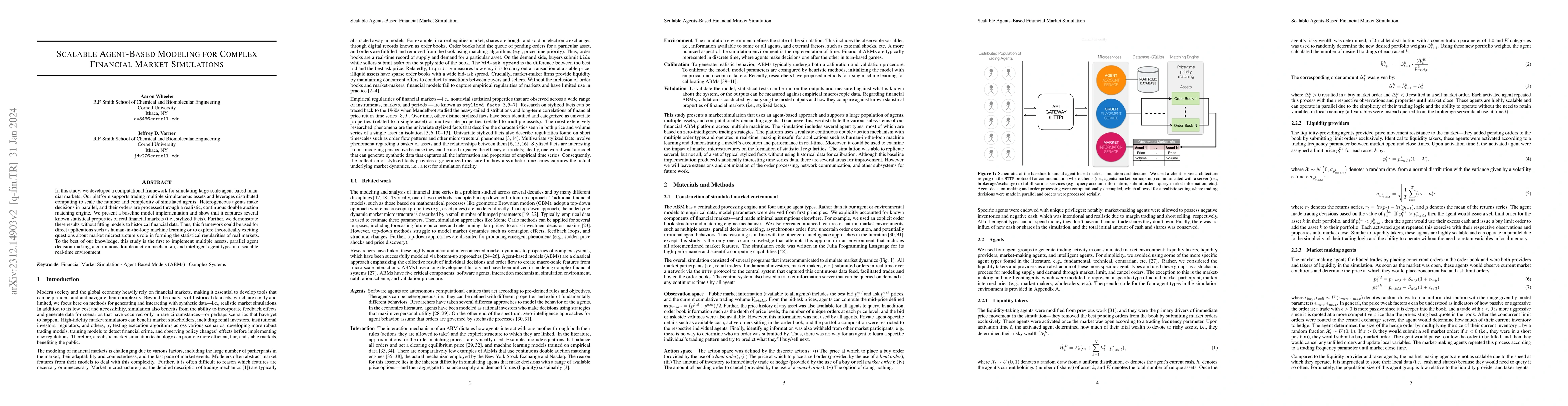

In this study, we developed a computational framework for simulating large-scale agent-based financial markets. Our platform supports trading multiple simultaneous assets and leverages distributed c...

This work presents a generative pre-trained transformer (GPT) designed for modeling financial time series. The GPT functions as an order generation engine within a discrete event simulator, enabling r...

Attention heads retrieve: given a query, they return a softmax-weighted average of stored values. We show that this computation is one step of gradient descent on a classical energy function, and that...

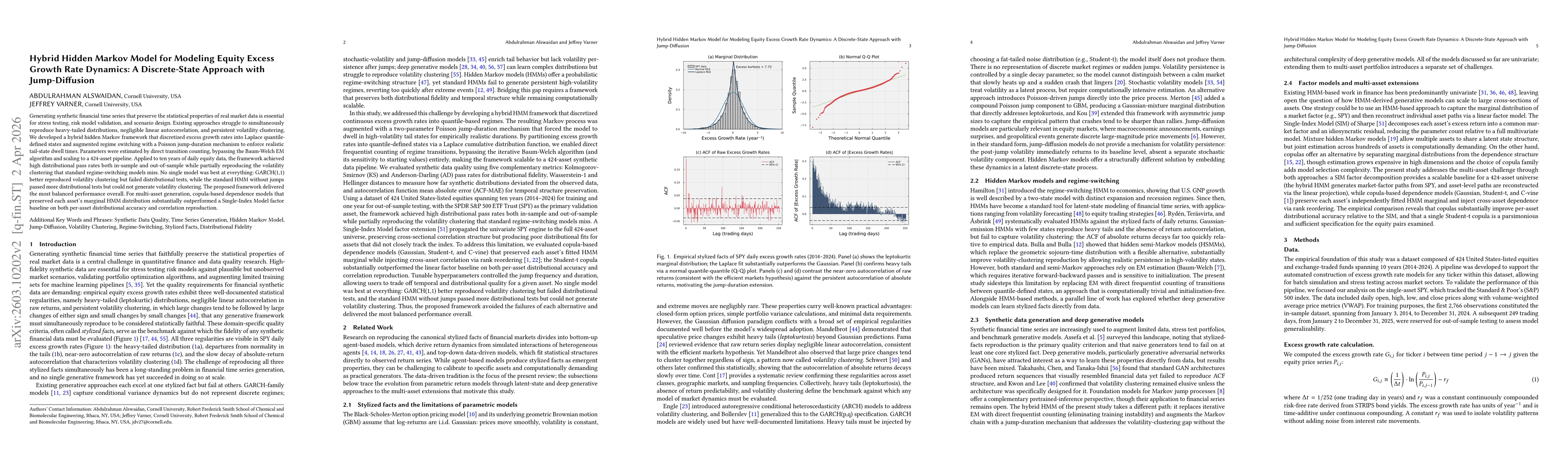

Generating synthetic financial time series that preserve statistical properties of real market data is essential for stress testing, risk model validation, and scenario design. Existing approaches, fr...

Most protein families have fewer than 100 known members, a regime where deep generative models overfit or collapse. We propose stochastic attention (SA), a training-free sampler that treats the modern...

We present BSTModelKit.jl, an open-source Julia package for constructing, solving, and analyzing Biochemical Systems Theory (BST) models of biochemical networks. The package implements S-system repres...

Protein sequence generation via stochastic attention produces plausible family members from small alignments without training, but treats all stored sequences equally and cannot direct generation towa...

Mathematical models of natural and man-made systems often have many adjustable parameters that must be estimated from multiple, potentially conflicting datasets. Rather than reporting a single best-fi...

Small longitudinal clinical cohorts, common in maternal health, rare diseases, and early-phase trials, limit computational modeling: too few patients to train reliable models, yet too costly and slow ...

In silico tools are important for generating novel hypotheses and exploring alternatives in de novo metabolic pathway design. However, while many computational frameworks have been proposed for retrob...

Generating realistic synthetic option prices requires implied volatility as an input, yet implied volatility is itself derived from observed option prices, creating a circular dependency that limits s...

Synthetic generators of daily equity returns let practitioners stress test, backtest, and design scenarios that a single realized market history cannot supply, but only if the generator reproduces the...

Ramkrishna, Kompala, and Tsao proposed the cybernetic model of microbial growth, in which cells allocate enzyme synthesis resources according to a matching rule that mimics rational decision-making. T...