Academic Profile

Statistics

Similar Authors

Papers on arXiv

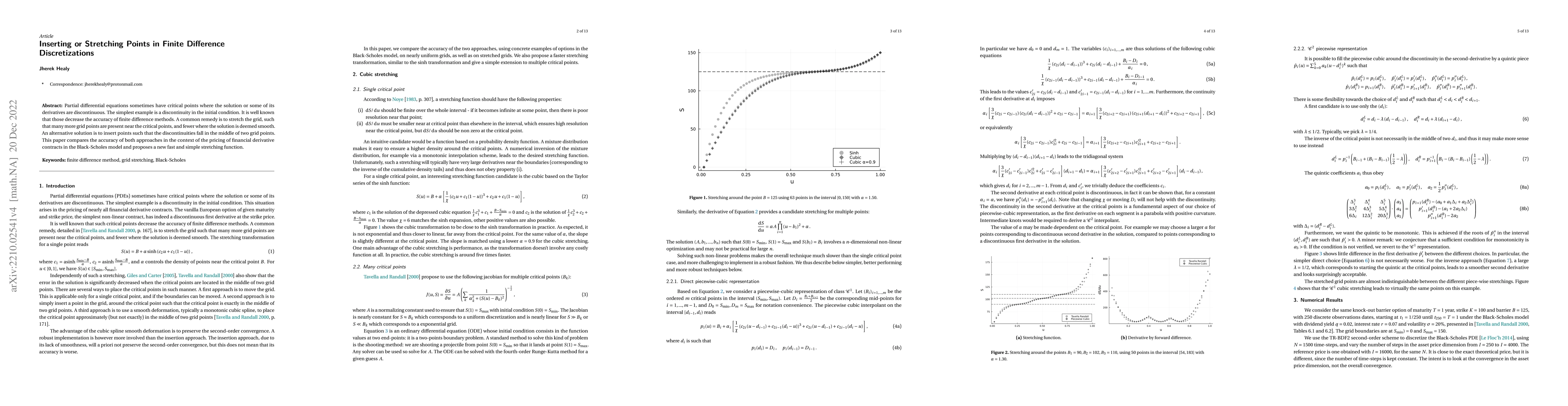

Partial differential equations sometimes have critical points where the solution or some of its derivatives are discontinuous. The simplest example is a discontinuity in the initial condition. It is...

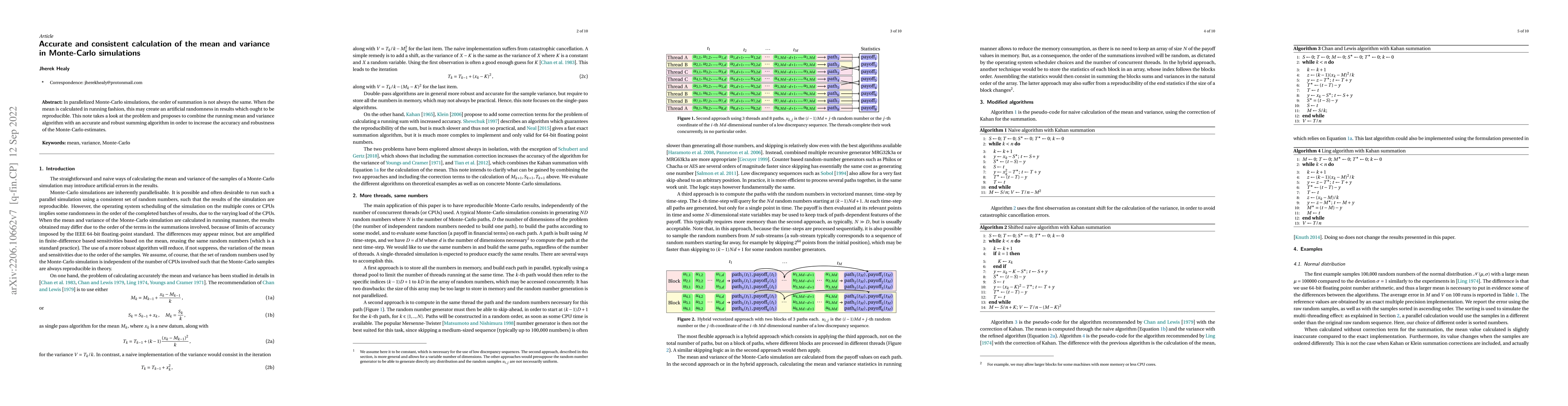

In parallelized Monte-Carlo simulations, the order of summation is not always the same. When the mean is calculated in running fashion, this may create an artificial randomness in results which ough...

This paper starts by defining the criteria where the early-exercise of an American option is never optimal, under positive, or negative rates. It follows with a short analysis of the various shapes ...

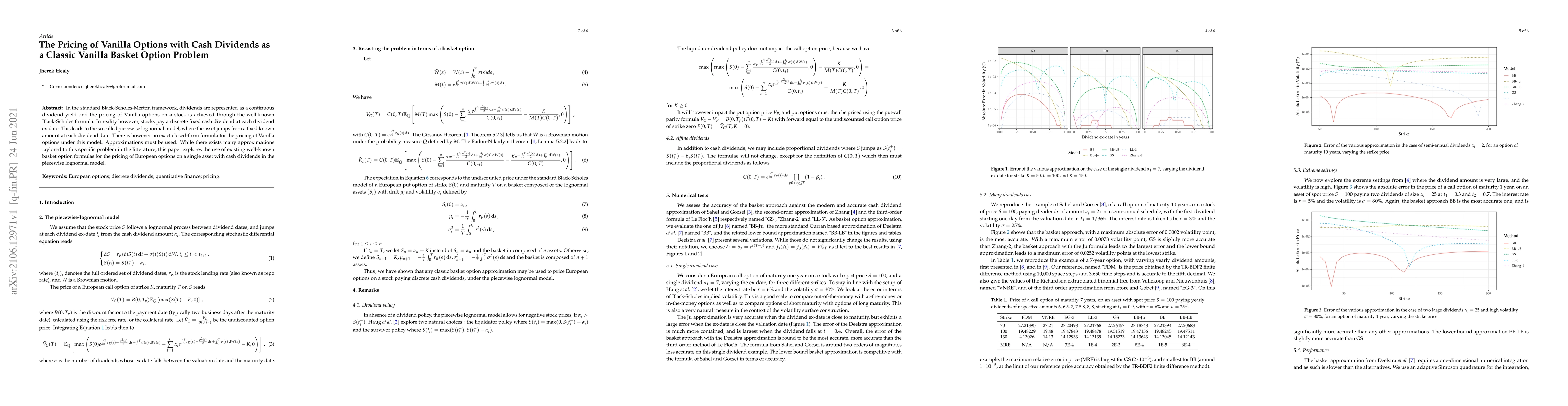

In the standard Black-Scholes-Merton framework, dividends are represented as a continuous dividend yield and the pricing of Vanilla options on a stock is achieved through the well-known Black-Schole...

The traditional way of building a yield curve is to choose an interpolation on discount factors, implied by the market tradable instruments. Since then, constructions based on specific interpolation...

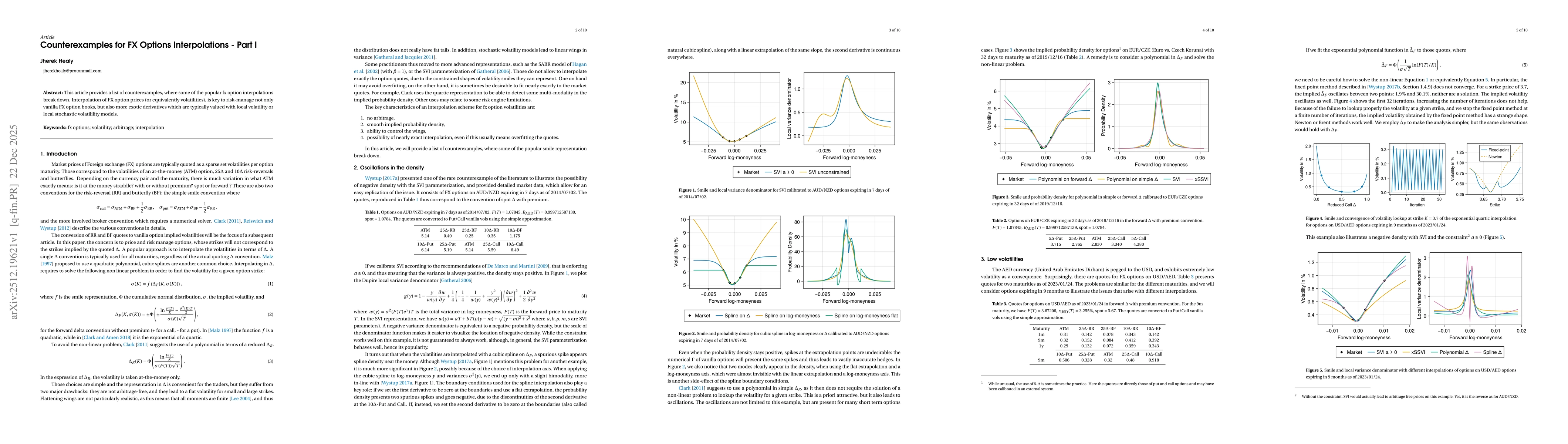

This article provides a list of counterexamples, where some of the popular fx option interpolations break down. Interpolation of FX option prices (or equivalently volatilities), is key to risk-manage ...

The Heston stochastic volatility model is arguably, the most popular stochastic volatility model used to price and risk manage exotic derivatives. In spite of this, it is not necessarily easy to calib...

This follow-up article analyzes the impact of foreign exchange option interpolation on the vanilla option implied volatilities. In particular different exact interpolations of broker quotes may lead t...

FlashIV is a low-latency Black--Scholes implied-volatility solver for production use. It normalises each input to an out-of-the-money price and solves a tail-stable erfcx/log-price residual. The hot p...