Academic Profile

Statistics

Similar Authors

Papers on arXiv

We consider quantile optimization of black-box functions that are estimated with noise. We propose two new iterative three-timescale local search algorithms. The first algorithm uses an appropriatel...

Classical reinforcement learning (RL) aims to optimize the expected cumulative reward. In this work, we consider the RL setting where the goal is to optimize the quantile of the cumulative reward. W...

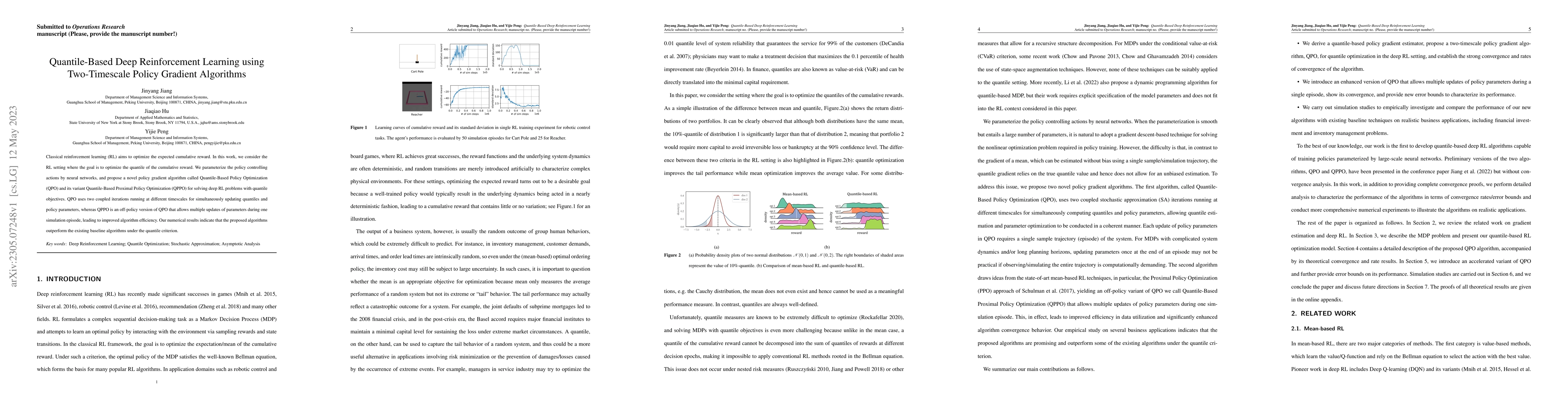

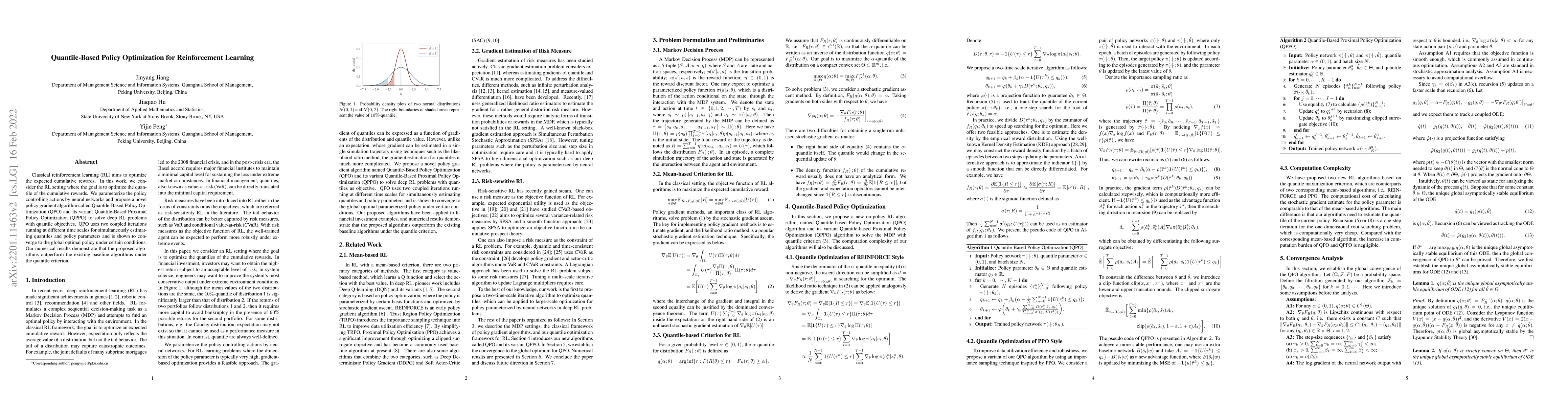

Classical reinforcement learning (RL) aims to optimize the expected cumulative rewards. In this work, we consider the RL setting where the goal is to optimize the quantile of the cumulative rewards....

Distortion Risk Measures (DRMs) capture risk preferences in decision-making and serve as general criteria for managing uncertainty. This paper proposes gradient descent algorithms for DRM optimization...

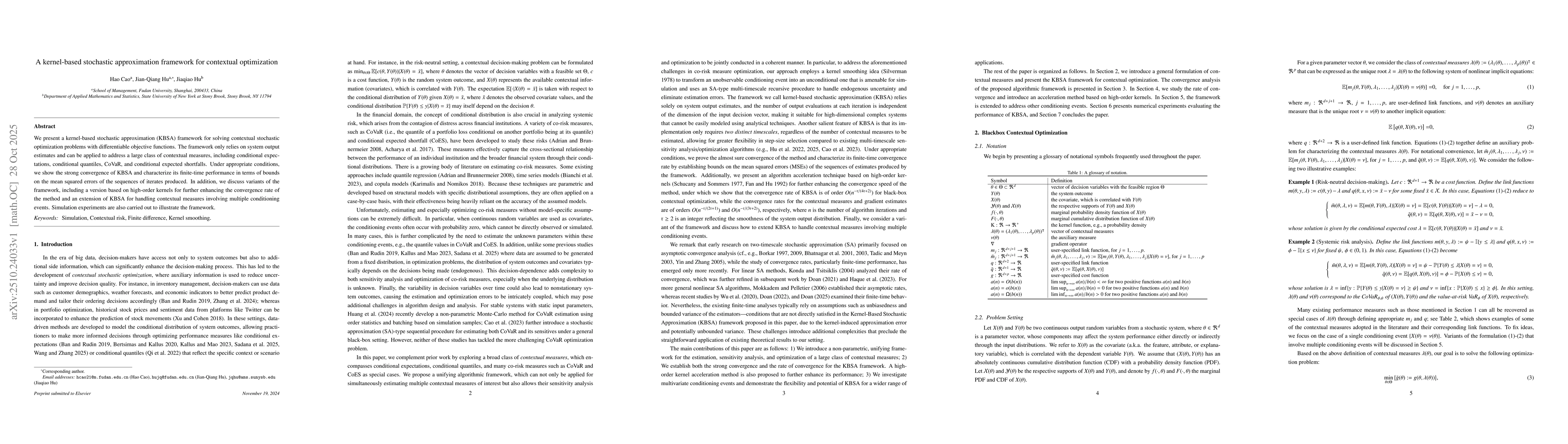

We present a kernel-based stochastic approximation (KBSA) framework for solving contextual stochastic optimization problems with differentiable objective functions. The framework only relies on system...

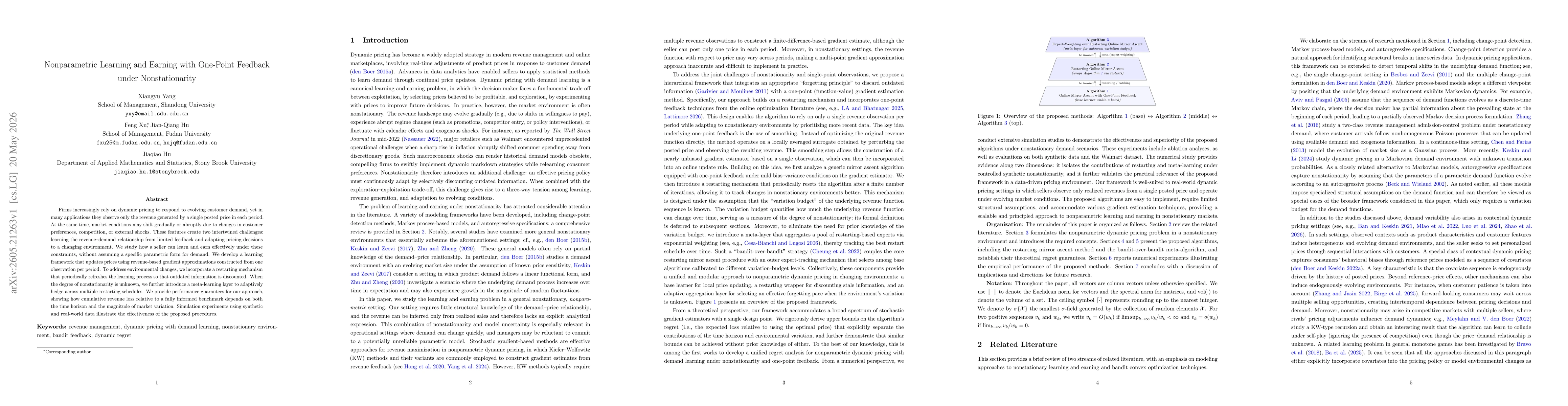

Firms increasingly rely on dynamic pricing to respond to evolving customer demand, yet in many applications they observe only the revenue generated by a single posted price in each period. At the same...