Academic Profile

Statistics

Similar Authors

Papers on arXiv

Reinforcement learning (RL) has proven to be well-performed and general-purpose in the inventory control (IC). However, further improvement of RL algorithms in the IC domain is impeded due to two limi...

We consider an online two-stage stochastic optimization with long-term constraints over a finite horizon of $T$ periods. At each period, we take the first-stage action, observe a model parameter rea...

We study the contextual bandits with knapsack (CBwK) problem under the high-dimensional setting where the dimension of the feature is large. The reward of pulling each arm equals the multiplication ...

The Network Revenue Management (NRM) problem is a well-known challenge in dynamic decision-making under uncertainty. In this problem, fixed resources must be allocated to serve customers over a fini...

We consider an online two-stage stochastic optimization with long-term constraints over a finite horizon of $T$ periods. At each period, we take the first-stage action, observe a model parameter rea...

We study the classical Network Revenue Management (NRM) problem with accept/reject decisions and $T$ IID arrivals. We consider a distributional form where each arrival must fall under a finite numbe...

We consider a stochastic lost-sales inventory control system with a lead time $L$ over a planning horizon $T$. Supply is uncertain, and is a function of the order quantity (due to random yield/capac...

In this paper, we study the problem of bandits with knapsacks (BwK) in a non-stationary environment. The BwK problem generalizes the multi-arm bandit (MAB) problem to model the resource consumption ...

Prophet inequalities consist of many beautiful statements that establish tight performance ratios between online and offline allocation algorithms. Typically, tightness is established by constructin...

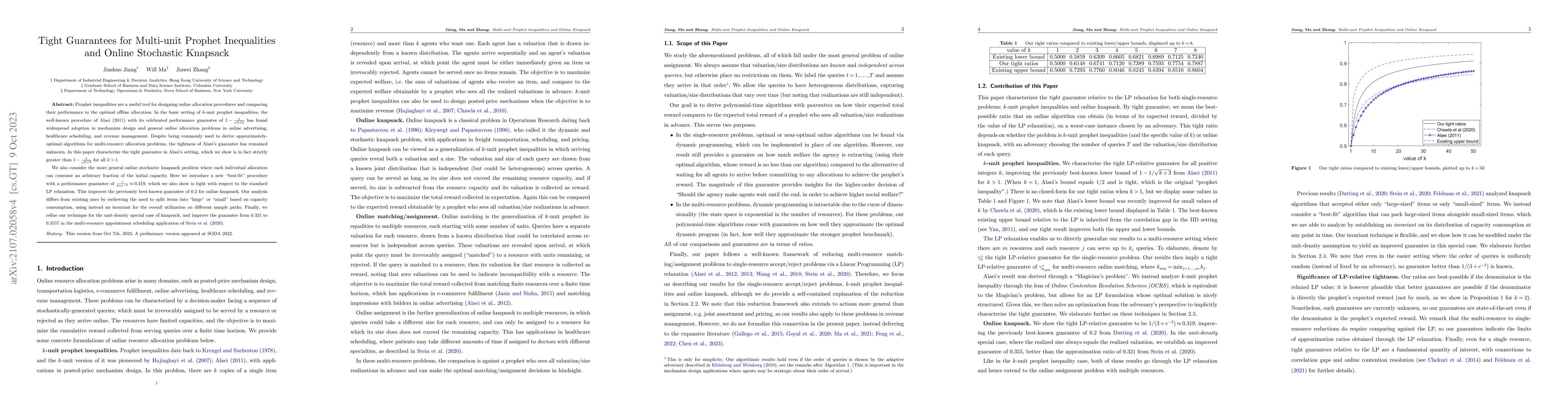

Prophet inequalities are a useful tool for designing online allocation procedures and comparing their performance to the optimal offline allocation. In the basic setting of $k$-unit prophet inequali...

We consider an online resource allocation problem where multiple resources, each with an individual initial capacity, are available to serve random requests arriving sequentially over multiple discr...

We consider a general online stochastic optimization problem with multiple budget constraints over a horizon of finite time periods. In each time period, a reward function and multiple cost function...

This paper investigates regret minimization, statistical inference, and their interplay in high-dimensional online decision-making based on the sparse linear context bandit model. We integrate the $\v...

We study the dynamic pricing problem with knapsack, addressing the challenge of balancing exploration and exploitation under resource constraints. We introduce three algorithms tailored to different i...

We study an online learning problem on dynamic pricing and resource allocation, where we make joint pricing and inventory decisions to maximize the overall net profit. We consider the stochastic depen...

Large Language Model (LLM) inference, where a trained model generates text one word at a time in response to user prompts, is a computationally intensive process requiring efficient scheduling to opti...

We study infinite-horizon Discounted Markov Decision Processes (DMDPs) under a generative model. Motivated by the Algorithm with Advice framework Mitzenmacher and Vassilvitskii 2022, we propose a nove...

We study how a budget-constrained bidder should learn to adaptively bid in repeated first-price auctions to maximize her cumulative payoff. This problem arose due to an industry-wide shift from second...

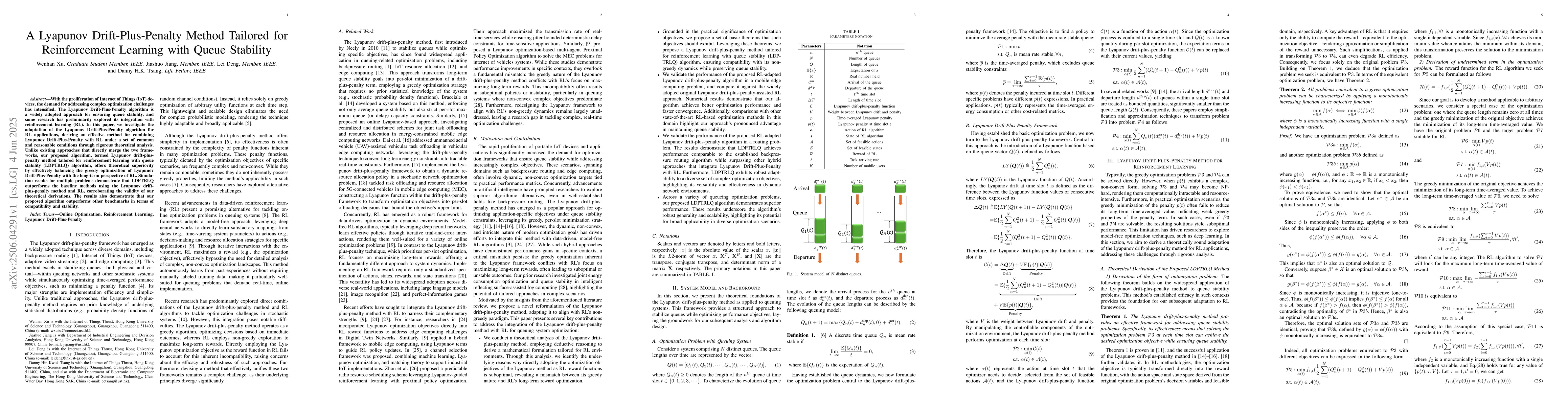

With the proliferation of Internet of Things (IoT) devices, the demand for addressing complex optimization challenges has intensified. The Lyapunov Drift-Plus-Penalty algorithm is a widely adopted app...

Inventory management remains a challenge for many small and medium-sized businesses that lack the expertise to deploy advanced optimization methods. This paper investigates whether Large Language Mode...

Decentralized decision making in multi--product firms can lead to efficiency losses when autonomous decision makers fail to internalize cross--product demand interactions. This paper quantifies the ma...

In this work, we study the sample complexity of obtaining a Nash equilibrium (NE) estimate in two-player zero-sum matrix games with noisy feedback. Specifically, we propose a novel algorithm that repe...

We study online resource allocation under non-stationary demand with a minimum offline data requirement. In this problem, a decision-maker must allocate multiple types of resources to sequentially arr...

In modern e-commerce and service operations, firms must jointly manage inventory replenishment and real-time order fulfillment to maximize profit under demand uncertainty. While each component has bee...

In this paper, we study the problem of learning to bid in repeated first-price auctions with budget constraints. In each period, the decision maker needs to submit a bid to win the auction and maximiz...

We consider the dynamic resource allocation problem where the decision space is finite-dimensional, yet the solution must satisfy a large or even infinite number of constraints revealed via streaming ...

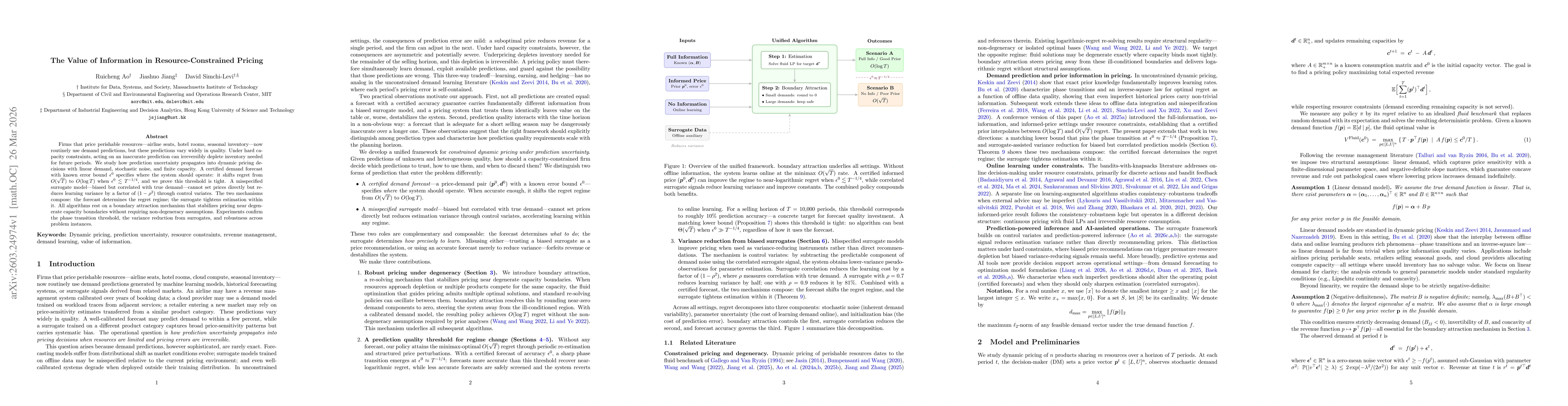

Firms that price perishable resources -- airline seats, hotel rooms, seasonal inventory -- now routinely use demand predictions, but these predictions vary widely in quality. Under hard capacity const...

In this paper, we study how a budget-constrained bidder should learn to bid adaptively in repeated first-price auctions to maximize cumulative payoff. This problem arises from the recent industry-wide...

Resource-constrained pricing controllers can make fixed-price inference impossible: the controller's resource state may remove the target price neighborhood from the feasible set, even when every real...

LLM post-training often relies on reinforcement learning methods that sample multiple rollouts per prompt, yet most existing approaches use a fixed rollout budget for every prompt, despite large diffe...