Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper is concerned with a linear-quadratic mean field Stackelberg stochastic differential game with partial information and common noise, which contains a leader and a large number of followers...

This paper is concerned with an indefinite linear-quadratic mean field games of stochastic large-population system, where the individual diffusion coefficients can depend on both the state and the c...

This paper is concerned with the relationship between general maximum principle and dynamic programming principle for the stochastic recursive optimal control problem with jumps, where the control d...

This paper is concerned with a linear-quadratic (LQ) Stackelberg mean field games of backward-forward stochastic systems, involving a backward leader and a substantial number of forward followers. T...

This paper is concerned with an overlapping information linear-quadratic (LQ) Stackelberg stochastic differential game with two leaders and two followers, where the diffusion terms of the state equa...

This paper is concerned with a kind of risk-sensitive optimal control problem for fully coupled forward-backward stochastic systems. The control variable enters the diffusion term of the state equat...

This paper is devoted to a Stackelberg stochastic differential game for a linear mean-field type stochastic differential system with a mean-field type quadratic cost functional in finite horizon. Th...

In this paper, we solve an open problem and obtain a general maximum principle for a stochastic optimal control problem where the control domain is an arbitrary non-empty set and all the coefficient...

This paper is devoted to a high-dimensional mixed leadership stochastic differential game on a finite horizon in feedback information mode, where the control variables enter into the diffusion term ...

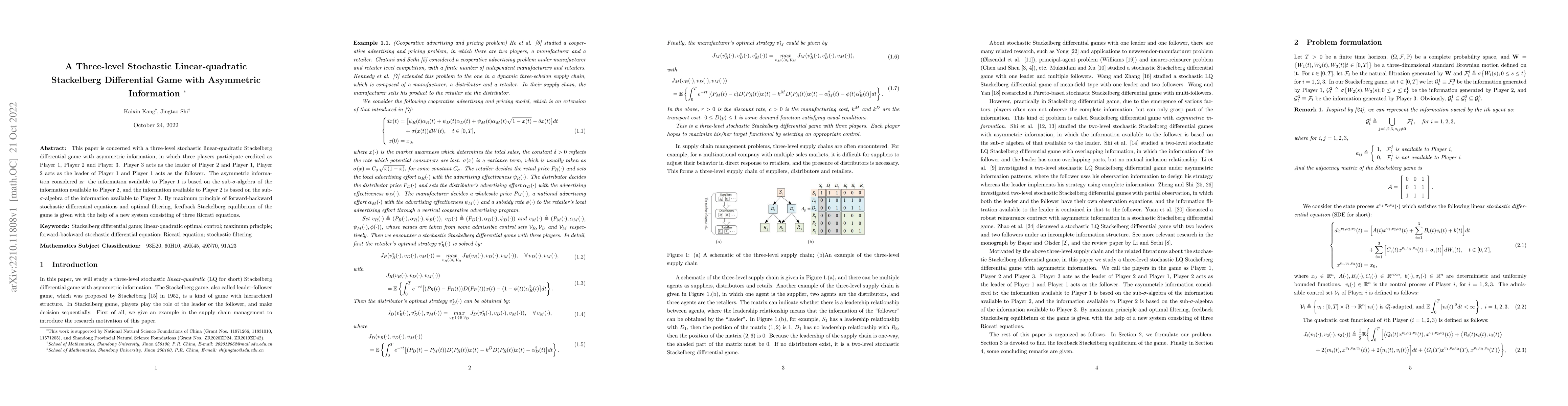

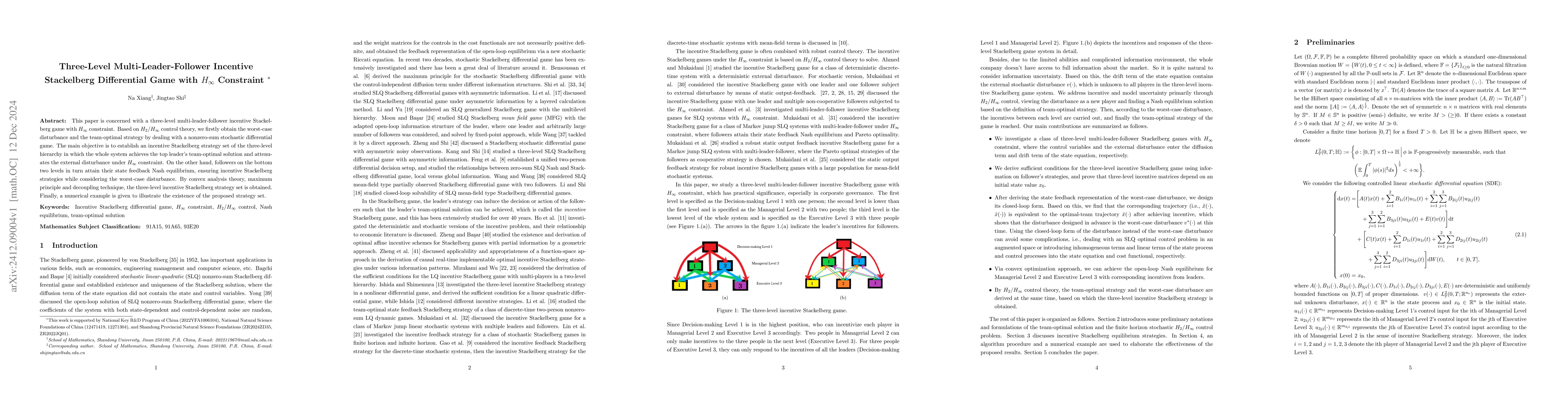

This paper is concerned with a three-level stochastic linear-quadratic Stackelberg differential game with asymmetric information, in which three players participate credited as Player 1, Player 2 an...

This paper is concerned with the stochastic linear-quadratic optimal control problem with Poisson jumps. The coefficients in the state equation and the weighting matrices in the cost functional are ...

This paper is concerned with a discounted optimal control problem of partially observed forward-backward stochastic systems with jumps on infinite horizon. The control domain is convex and a kind of...

IIn this paper, we study a partially observed progressive optimal control problem of forward-backward stochastic differential equations with random jumps, where the control domain is not necessarily...

In this paper, a leader-follower stochastic differential game is studied for a linear stochastic differential equation with a quadratic cost functional. The coefficients in the state equation and th...

This paper is concerned with the closed-loop solvability of one kind of linear-quadratic Stackelberg stochastic differential game, where the coefficients are deterministic. The notion of the closed-...

This paper is concerned with a linear quadratic stochastic Stackelberg differential game with time delay. The model is general, in which the state delay and the control delay both appear in the stat...

This paper is concerned with a linear quadratic optimal control problem of delayed backward stochastic differential equations. An explicit representation is derived for the optimal control, which is...

This paper is concerned with a Stackelberg stochastic differential game with asymmetric noisy observation, with one follower and one leader. In our model, the follower cannot observe the state proce...

This paper is concerned with the stochastic recursive optimal control problem with mixed delay. The connection between Pontryagin's maximum principle and Bellman's dynamic programming principle is d...

This paper is concerned with a Stackelberg game of backward stochastic differential equations (BSDEs) with partial information, where the information of the follower is a sub-$\sigma$-algebra of tha...

In this paper, we study a linear-quadratic partially observed Stackelberg stochastic differential game problem in which a single leader and multiple followers are involved. We consider more practical ...

This paper studies a linear-quadratic mean-field game of stochastic large-population system, where the large-population system satisfies a class of $N$ weakly coupled linear backward stochastic differ...

This paper is concerned with a three-level multi-leader-follower incentive Stackelberg game with $H_\infty$ constraint. Based on $H_2/H_\infty$ control theory, we firstly obtain the worst-case disturb...

This paper is concerned with a two-person zero-sum indefinite stochastic linear-quadratic Stackelberg differential game with asymmetric informational uncertainties, where both the leader and follower ...

This paper is concerned with a general maximum principle for the fully coupled forward-backward stochastic optimal control problem with jumps, where the control domain is not necessarily convex, withi...

This paper addresses a linear-quadratic Stackelberg mean field (MF) games and teams problem with arbitrary population sizes, where the game among the followers is further categorized into two types: n...

This paper studies a new class of linear-quadratic mean field games and teams problem, where the large-population system satisfies a class of $N$ weakly coupled linear backward stochastic differential...

This paper is concerned with a stochastic linear-quadratic leader-follower differential game with elephant memory. The model is general in that the state equation for both the leader and the follower ...

This paper is devoted to an optimal control problem of fully coupled forward-backward stochastic differential equations driven by sub-diffusion, whose solutions are not Markov processes. The stochasti...

This paper is concerned with a linear-quadratic partially observed mean field Stackelberg stochastic differential game, which contains a leader and a large number of followers. Specifically, the follo...

This paper is concerned with one kind of partially observed progressive optimal control problems of coupled forward-backward stochastic systems driven by both Brownian motion and Poisson random measur...

This paper investigates a class of general linear-quadratic mean field games with common noise, where the diffusion terms of the system contain the state variables, control variables, and the average ...

This paper is concerned with the relationship between maximum principle and dynamic programming principle for risk-sensitive stochastic optimal control problems. Under the smooth assumption of the val...

This paper investigates a robust incentive Stackelberg stochastic differential game problem for a linear-quadratic mean field system, where the model uncertainty appears in the drift term of the leade...

This paper is concerned with the maximum principle and dynamic programming principle for mean-variance portfolio selection of jump diffusions and their relationship. First, the optimal portfolio and e...

This paper investigates a linear-quadratic mean field games problem with common noise, where the drift term and diffusion term of individual state equations are coupled with both the state, control, a...

This paper is concerned with a linear-quadratic non-zero sum differential game with asymmetric delayed information. To be specific, two players exist time delays simultaneously which are different, le...

In this paper, the mean-variance portfolio selection problem with Poisson jumps are studied, where the recursive utility is given by the solution to a backward stochastic differential equation with Po...

This paper is concerned with a stochastic linear-quadratic optimal control problem of Markovian regime switching system with model uncertainty and partial information, where the information available ...

This paper investigates an optimal control problem where the system is described by a stochastic differential equation with extended mixed delays that contain point delay, extended distributed delay, ...

In this paper, a partially observed stochastic linear Stackelberg differential game with mean-variance criteria is studied. Randomness comes from Brownian motions and Poisson random measures. which le...

This paper investigates leader-follower linear-quadratic stochastic graphon games, which consist of a single leader and a continuum of followers. The state equations of the followers interact through ...

In this paper, we study the relationship between general maximum principle and dynamic programming principle for risk-sensitive stochastic optimal control problems, where the control domain is not nec...