Academic Profile

Statistics

Similar Authors

Papers on arXiv

In this paper we propose a new method for probabilistic forecasting of electricity prices. It is based on averaging point forecasts from different models combined with expectile regression. We show ...

In this paper we analyze the product of bi-dimensional VAR(1) model components. For the introduced time series we derive general formulas for the autocovariance function and study its properties for...

In this paper we study the distribution of a product of two continuous random variables. We derive formulas for the probability density functions and moments of the products of the Gaussian, log-nor...

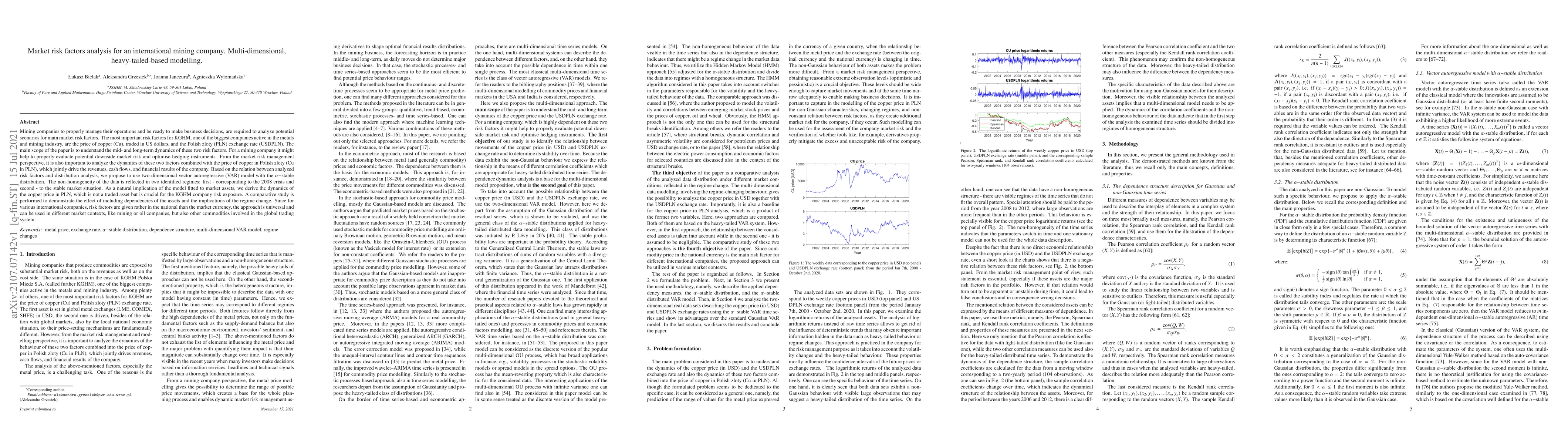

Mining companies to properly manage their operations and be ready to make business decisions, are required to analyze potential scenarios for main market risk factors. The most important risk factor...

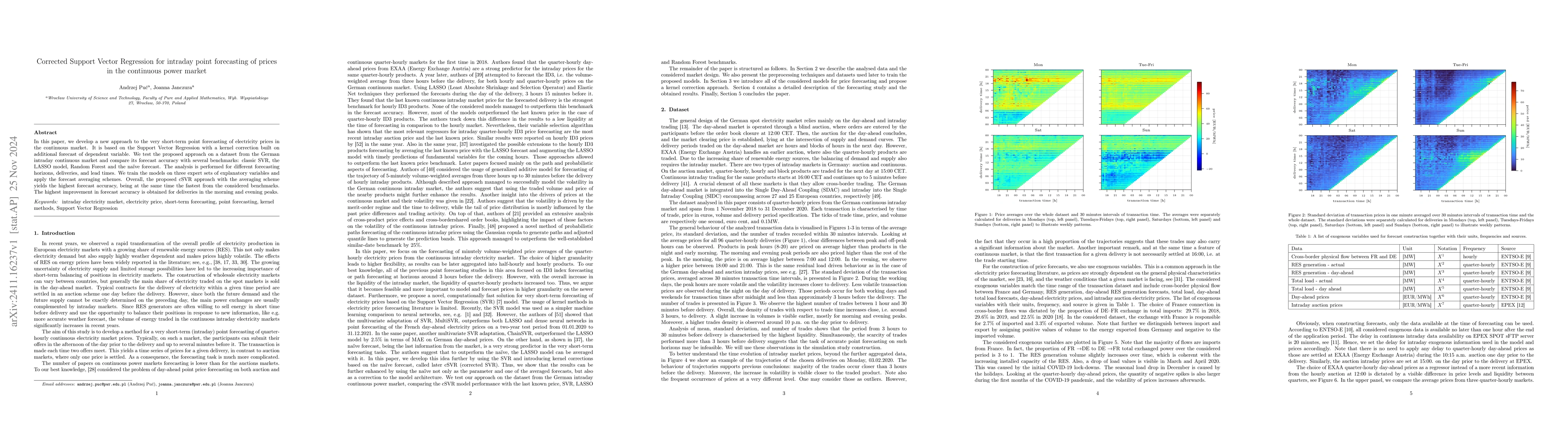

In this paper, we develop a new approach to the very short-term point forecasting of electricity prices in the continuous market. It is based on the Support Vector Regression with a kernel correction ...

Continuous intraday electricity markets play an increasingly important role in short-term trading and balancing, yet decision-making under rapidly evolving price dynamics remains challenging. This pap...