Academic Profile

Statistics

Similar Authors

Papers on arXiv

Blockchain technology, a foundational distributed ledger system, enables secure and transparent multi-party transactions. Despite its advantages, blockchain networks are susceptible to anomalies and...

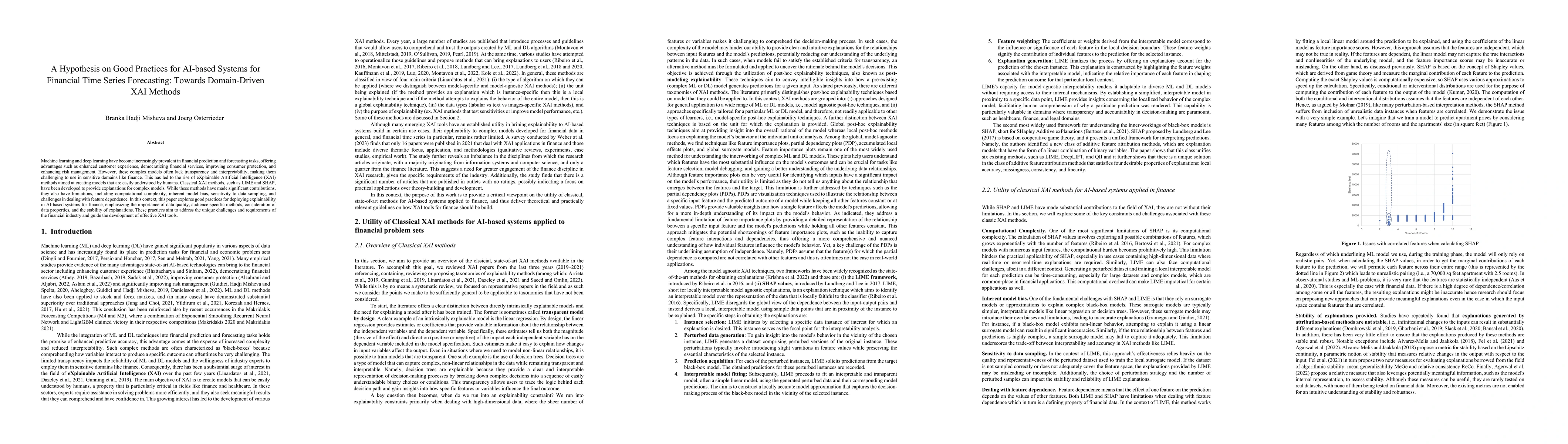

Machine learning and deep learning have become increasingly prevalent in financial prediction and forecasting tasks, offering advantages such as enhanced customer experience, democratising financial...

We delve into the intricate world of share buy-backs, a strategic corporate capital allocation tool that has gained significant prominence over the past few decades. Despite being the subject of ext...

In this paper, we propose a probabilistic model for computing an interpolative decomposition (ID) in which each column of the observed matrix has its own priority or importance, so that the end resu...

This study examines the weak form of the efficient market hypothesis for Bitcoin using a feedforward neural network. Due to the increasing popularity of cryptocurrencies in recent years, the questio...

In this bachelor thesis, we show how four different machine learning methods (Long Short-Term Memory, Random Forest, Support Vector Machine Regression, and k-Nearest Neighbor) perform compared to al...

This paper presents a Double Deep Q-Network algorithm for trading single assets, namely the E-mini S&P 500 continuous futures contract. We use a proven setup as the foundation for our environment wi...

In February 2018, the VIX index has seen its largest ever increase and has lead to significant losses for some major volatility related products. Despite many efforts, the precise underlying reasons...

Financial trading has been widely analyzed for decades with market participants and academics always looking for advanced methods to improve trading performance. Deep reinforcement learning (DRL), a...

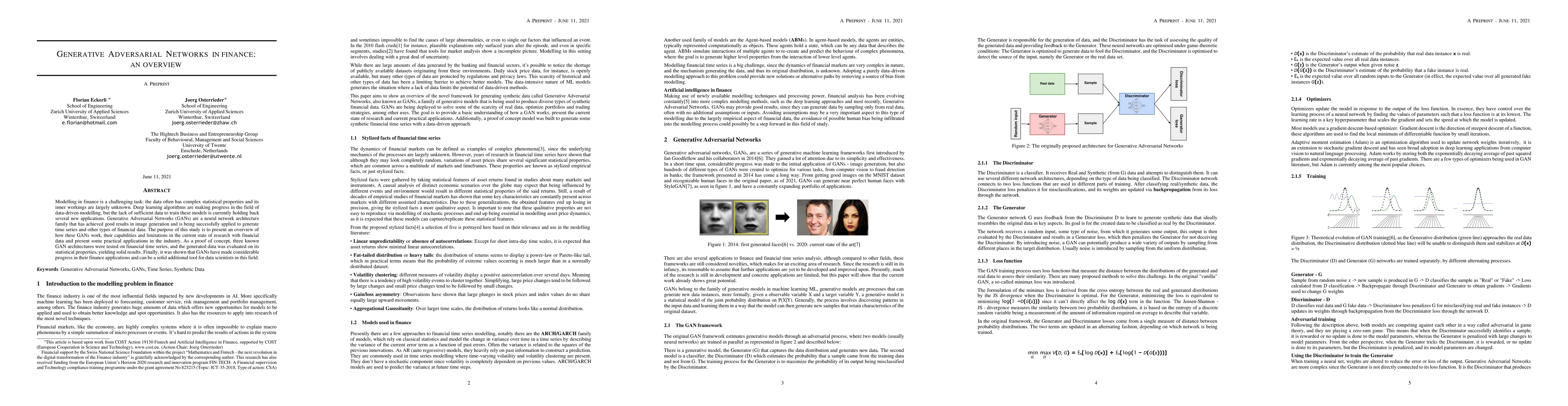

Modelling in finance is a challenging task: the data often has complex statistical properties and its inner workings are largely unknown. Deep learning algorithms are making progress in the field of...

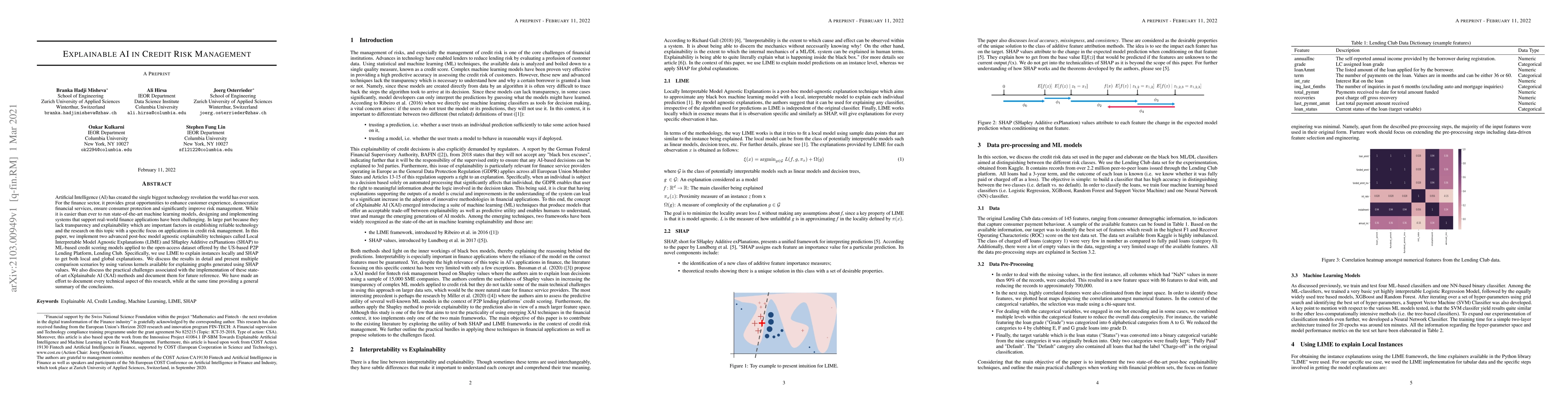

Artificial Intelligence (AI) has created the single biggest technology revolution the world has ever seen. For the finance sector, it provides great opportunities to enhance customer experience, dem...

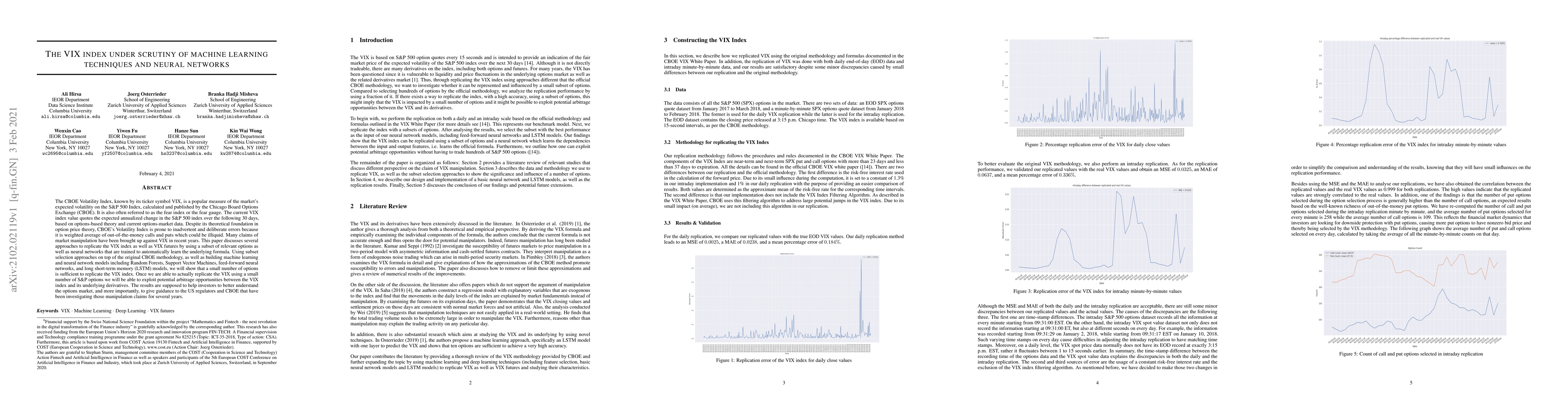

The CBOE Volatility Index, known by its ticker symbol VIX, is a popular measure of the market's expected volatility on the SP 500 Index, calculated and published by the Chicago Board Options Exchang...

This paper introduces an algorithmic framework for conducting systematic literature reviews (SLRs), designed to improve efficiency, reproducibility, and selection quality assessment in the literature ...