Academic Profile

Statistics

Similar Authors

Papers on arXiv

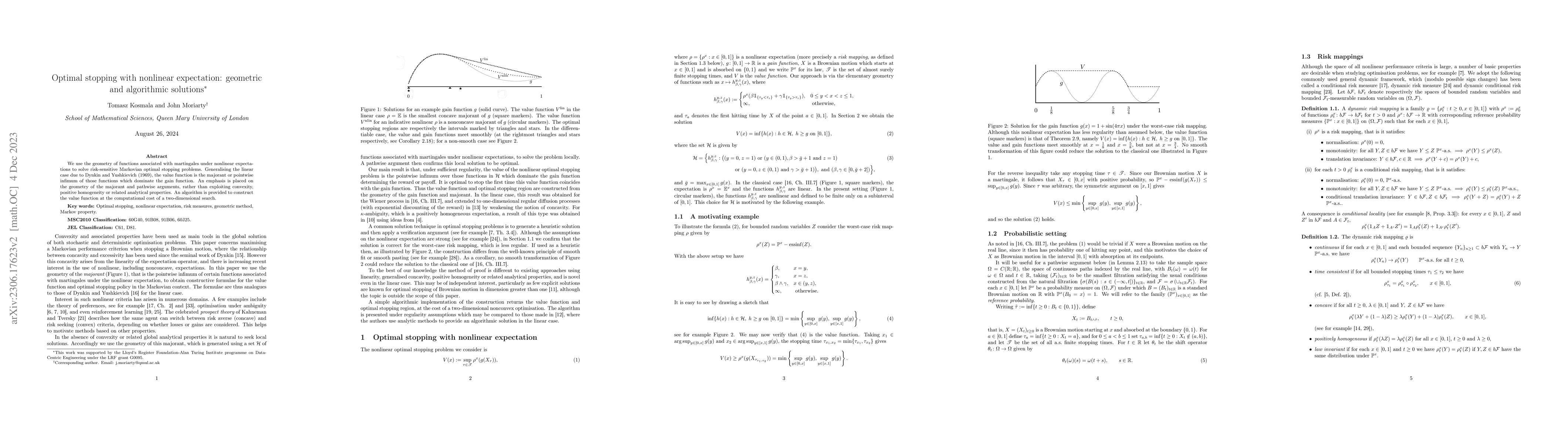

We use the geometry of functions associated with martingales under nonlinear expectations to solve risk-sensitive Markovian optimal stopping problems. Generalising the linear case due to Dynkin and ...

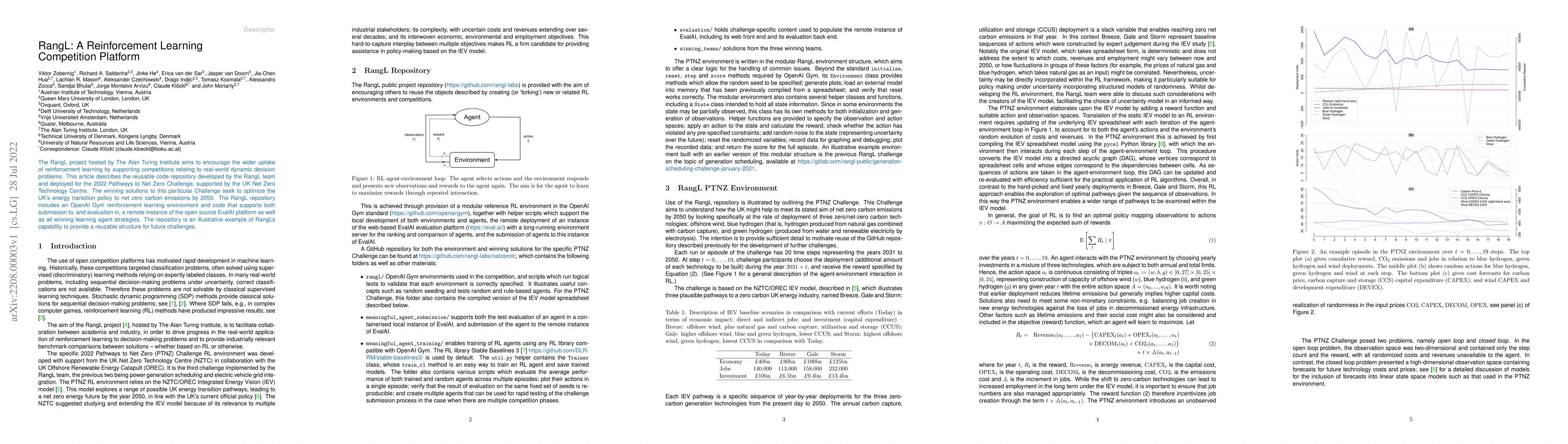

The RangL project hosted by The Alan Turing Institute aims to encourage the wider uptake of reinforcement learning by supporting competitions relating to real-world dynamic decision problems. This a...

We present the Basin Hopping with Skipping (BH-S) algorithm for stochastic optimisation, which replaces the perturbation step of basin hopping (BH) with a so-called skipping proposal from the rare-e...

This paper investigates large fluctuations of Locational Marginal Prices (LMPs) in wholesale energy markets caused by volatile renewable generation profiles. Specifically, we study events of the for...

We formulate a probabilistic Markov property in discrete time under a dynamic risk framework with minimal assumptions. This is useful for recursive solutions to risk-sensitive versions of dynamic op...

We solve non-Markovian optimal switching problems in discrete time on an infinite horizon, when the decision maker is risk aware and the filtration is general, and establish existence and uniqueness...

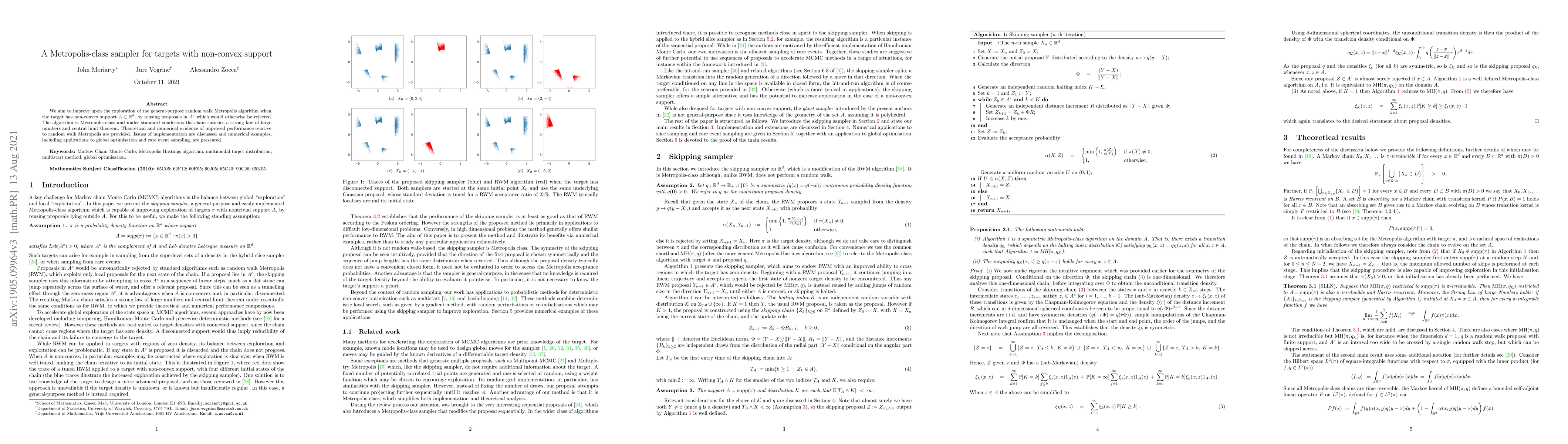

We aim to improve upon the exploration of the general-purpose random walk Metropolis algorithm when the target has non-convex support $A \subset \mathbb{R}^d$, by reusing proposals in $A^c$ which wo...

In the nonzero-sum setting, we establish a connection between Nash equilibria in games of optimal stopping (Dynkin games) and generalised Nash equilibrium problems (GNEP). In the Dynkin game this re...

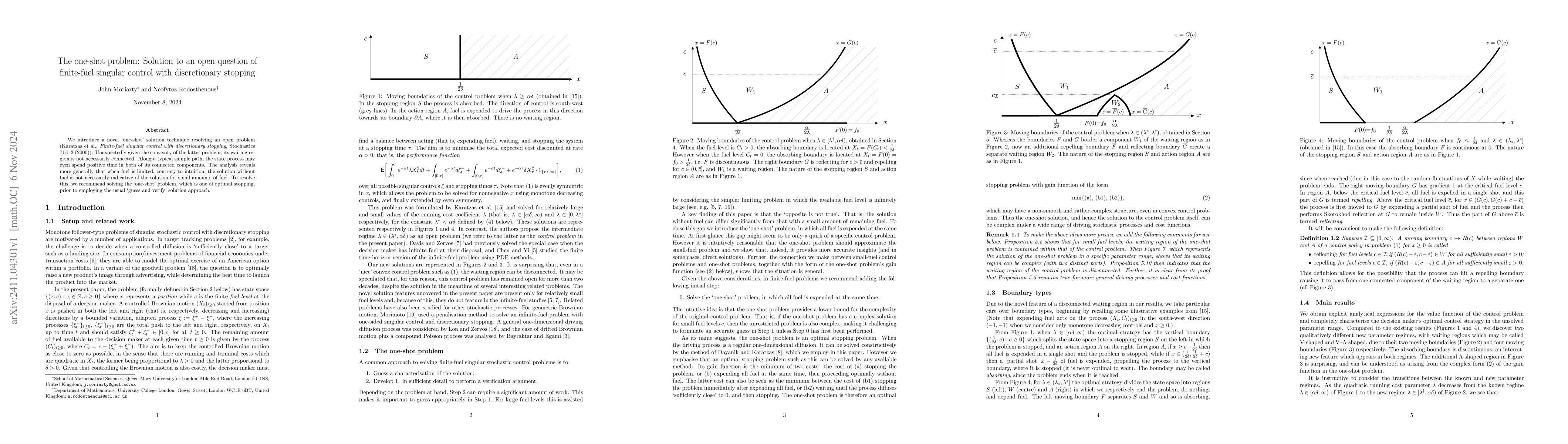

We introduce a novel 'one-shot' solution technique resolving an open problem (Karatzas et al., Finite-fuel singular control with discretionary stopping, Stochastics 71:1-2 (2000)). Unexpectedly given ...

We solve optimal stopping for multidimensional Brownian motion in a bounded domain, a question raised in Dynkin and Yushkevich (1967), where the one-dimensional case was presented. Taking a geometric ...