Academic Profile

Statistics

Similar Authors

Papers on arXiv

This book is about dynamic programming and its applications in economics, finance, and adjacent fields. It brings together recent innovations in the theory of dynamic programming and provides applic...

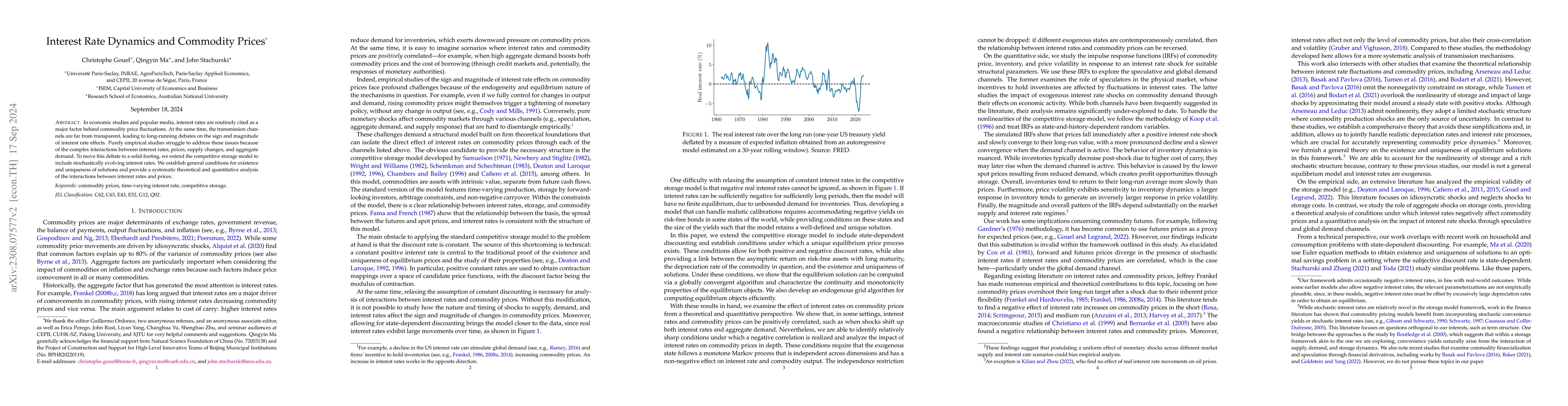

Monetary conditions are frequently cited as a significant factor influencing fluctuations in commodity prices. However, the precise channels of transmission are less well identified. In this paper, ...

We introduce a completely abstract dynamic programming framework in which dynamic programs are sets of policy operators acting on a partially ordered space. We provide an optimality theory based on ...

Systems of the form $x = (A x^s)^{1/s} + b$ arise in a range of economic, financial and control problems, where $A$ is a linear operator acting on a space of real-valued functions (or vectors) and $...

This textbook is an introduction to economic networks, intended for students and researchers in the fields of economics and applied mathematics. The textbook emphasizes quantitative modeling, with t...

Eisenberg and Noe (2001) analyze systemic risk for financial institutions linked by a network of liabilities. They show that the solution to their model is unique when the financial system is satisf...

We propose a new approach to solving dynamic decision problems with unbounded rewards based on the transformations used in Q-learning. In our case, the objective of the transform is to convert an un...

We propose a new approach to solving dynamic decision problems with rewards that are unbounded below. The approach involves transforming the Bellman equation in order to convert an unbounded problem...

In Hopenhayn's (1992) entry-exit model productivity is bounded, implying that the predicted firm size distribution cannot match the power law tail observable in the data. In this paper we remove the...

We show that competitive equilibria in a range of models related to production networks can be recovered as solutions to dynamic programs. Although these programs fail to be contractive, we prove th...

This paper extends the core results of discrete time infinite horizon dynamic programming to the case of state-dependent discounting. We obtain a condition on the discount factor process under which...

We analyze the household savings problem in a general setting where returns on assets, non-financial income and impatience are all state dependent and fluctuate over time. All three processes can be...

In the theory of dynamic programming, an optimal policy is a policy whose lifetime value dominates that of all other policies at every point in the state space. This raises a natural question: under w...

This paper integrates two strands of the literature on stability of general state Markov chains: conventional, total variation based results and more recent order-theoretic results. First we introduce...

In recent years, a range of measures of partial stochastic dominance have been introduced. These measures attempt to determine the extent to which one distribution is dominated by another. We assess t...

For Markov chains and Markov processes exhibiting a form of stochastic monotonicity (larger states shift up transition probabilities in terms of stochastic dominance), stability and ergodicity results...

Recent approaches to the theory of dynamic programming view dynamic programs as families of policy operators acting on partially ordered sets. In this paper, we extend these ideas by shifting from arb...

Many economic models feature monotone Markov dynamics on state spaces that may be noncompact. Establishing existence, uniqueness, and stability of stationary distributions in such settings has require...

We study relationships between dynamic programs by applying conjugacy methods from dynamical systems theory. When two dynamic programs are connected by an order isomorphism, we show that optimality pr...

We study abstract dynamic programs on partially ordered spaces, pairing the order-theoretic approach to dynamic programming with topological and metric foundations. We show that readily verifiable for...