Academic Profile

Statistics

Similar Authors

Papers on arXiv

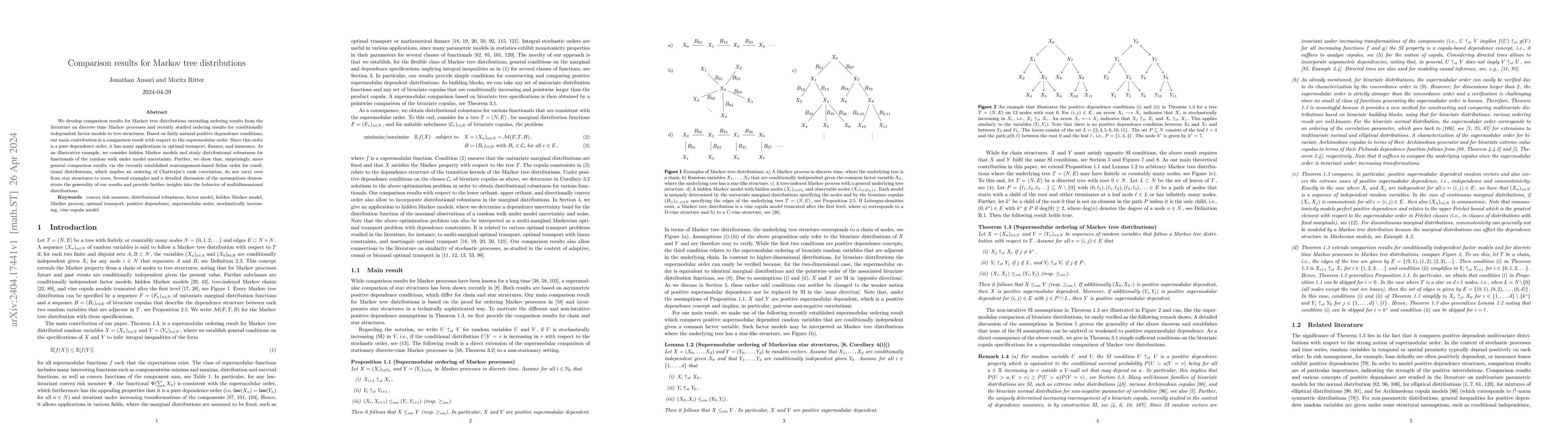

We develop comparison results for Markov tree distributions extending ordering results from the literature on discrete time Markov processes and recently studied ordering results for conditionally i...

Motivated by recently investigated results on dependence measures and robust risk models, this paper provides an overview of dependence properties of many well-known bivariate copula families, where...

Recently established, directed dependence measures for pairs $(X,Y)$ of random variables build upon the natural idea of comparing the conditional distributions of $Y$ given $X=x$ with the marginal d...

We show how inter-asset dependence information derived from market prices of options can lead to improved model-free price bounds for multi-asset derivatives. Depending on the type of the traded opt...

Multidimensional integration by parts formulas are valid under the standard assumption that one of the functions is continuous and the other has bounded Hardy-Krause variation. Motivated by several ...

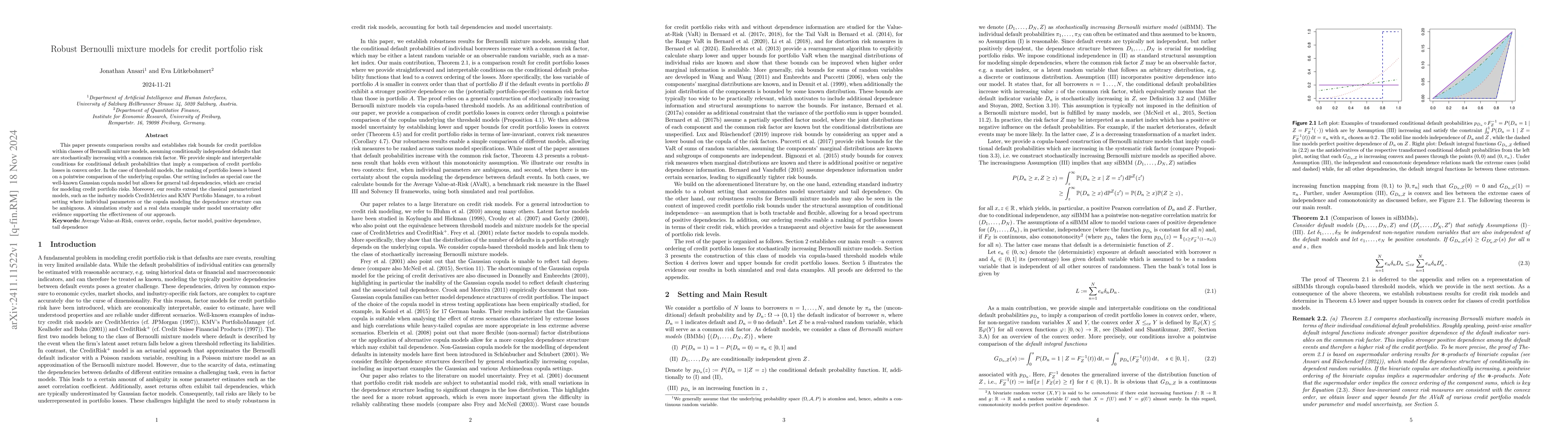

This paper presents comparison results and establishes risk bounds for credit portfolios within classes of Bernoulli mixture models, assuming conditionally independent defaults that are stochastically...

While measures of concordance -- such as Spearman's rho, Kendall's tau, and Blomqvist's beta -- are continuous with respect to weak convergence, Chatterjee's rank correlation xi recently introduced in...

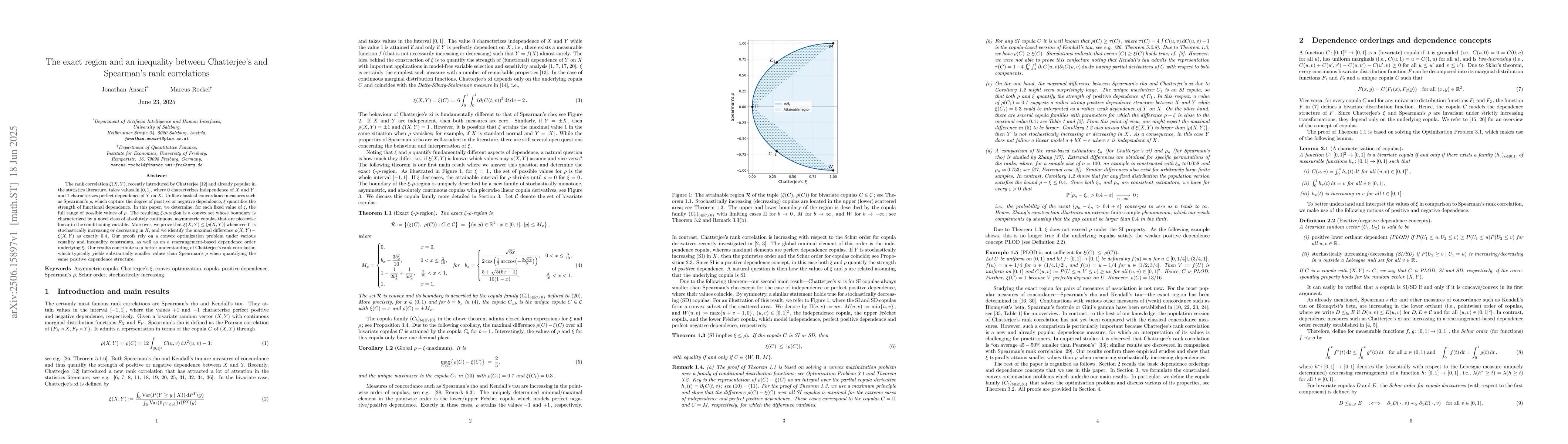

The rank correlation xi(X,Y), recently introduced by Chatterjee [12] and already popular in the statistics literature, takes values in [0,1], where 0 characterizes independence of X and Y, and 1 chara...

We introduce a new dependence order that satisfies eight natural axioms that we propose for a global dependence order. Its minimal and maximal elements characterize independence and perfect dependence...

Recent research in statistics has focused on dependence measures kappa(Y,X) taking values in [0, 1], where 0 characterizes independence of X and Y, and 1 perfect functional dependence of Y on X. One c...

Recently studied dependence measures, such as Chatterjee's rank correlation, that characterize both independence and perfect functional dependence, provide a powerful framework for detecting nonlinear...