Academic Profile

Statistics

Similar Authors

Papers on arXiv

The Cheyette model is a quasi-Gaussian volatility interest rate model widely used to price interest rate derivatives such as European and Bermudan Swaptions for which Monte Carlo simulation has beco...

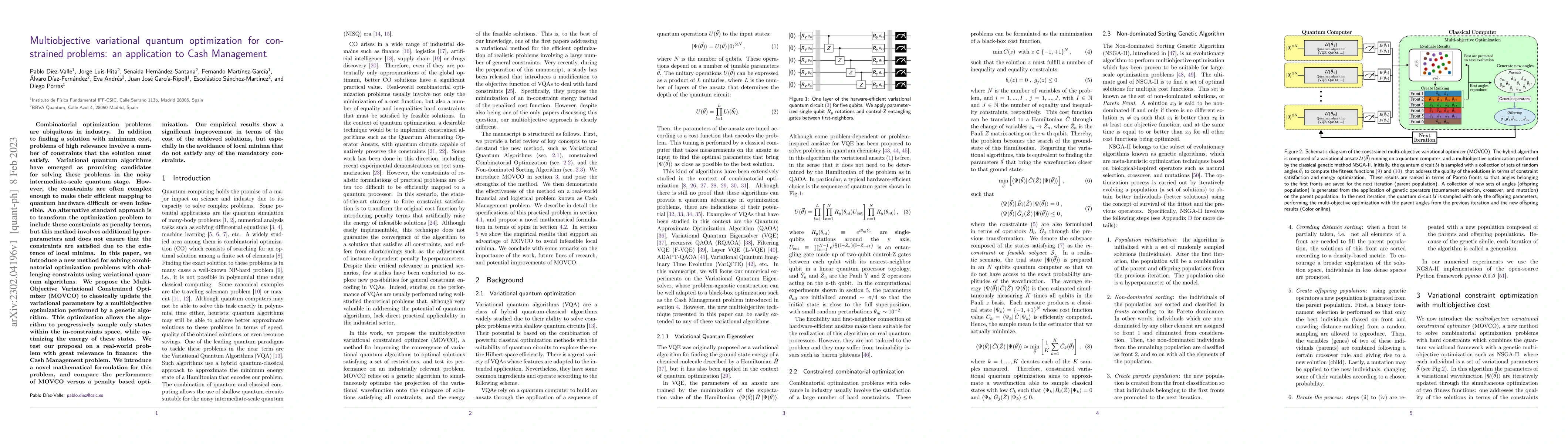

Combinatorial optimization problems are ubiquitous in industry. In addition to finding a solution with minimum cost, problems of high relevance involve a number of constraints that the solution must...

In this paper we tackle the problem of dynamic portfolio optimization, i.e., determining the optimal trading trajectory for an investment portfolio of assets over a period of time, taking into accou...

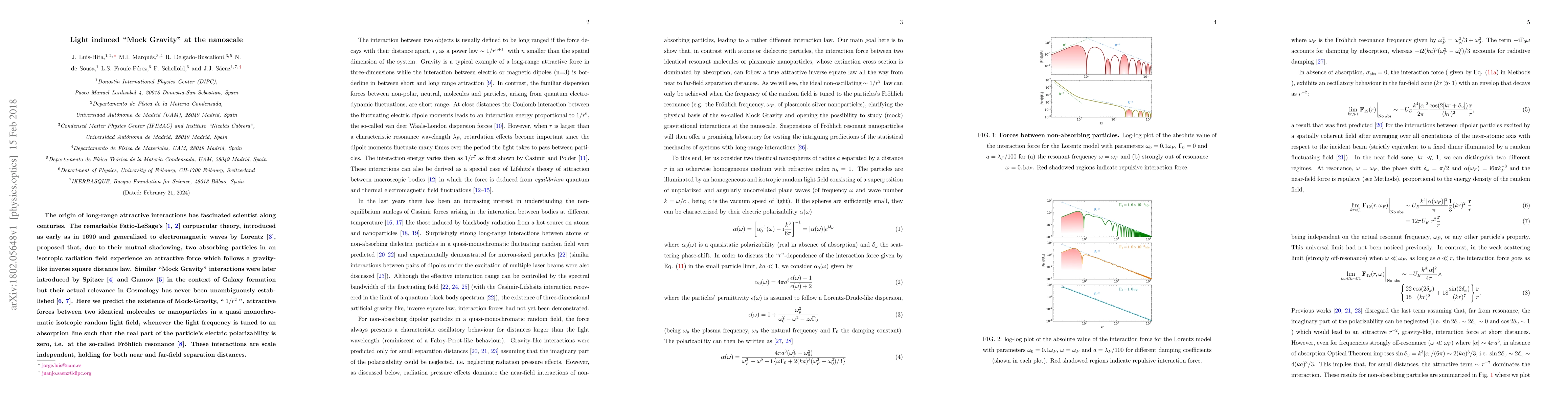

The origin of long-range attractive interactions has fascinated scientist along centuries. The remarkable Fatio-LeSage's corpuscular theory, introduced as early as in 1690 and generalized to electro...