Academic Profile

Statistics

Similar Authors

Papers on arXiv

In the context of large financial markets we formulate the notion of \emph{no asymptotic free lunch with vanishing risk} (NAFLVR), under which we can prove a version of the fundamental theorem of as...

Using a Besov topology on spaces of modelled distributions in the framework of Hairer's regularity structures, we prove the reconstruction theorem on these Besov spaces with negative regularity. The...

Robust utility optimization enables an investor to deal with market uncertainty in a structured way, with the goal of maximizing the worst-case outcome. In this work, we propose a generative adversa...

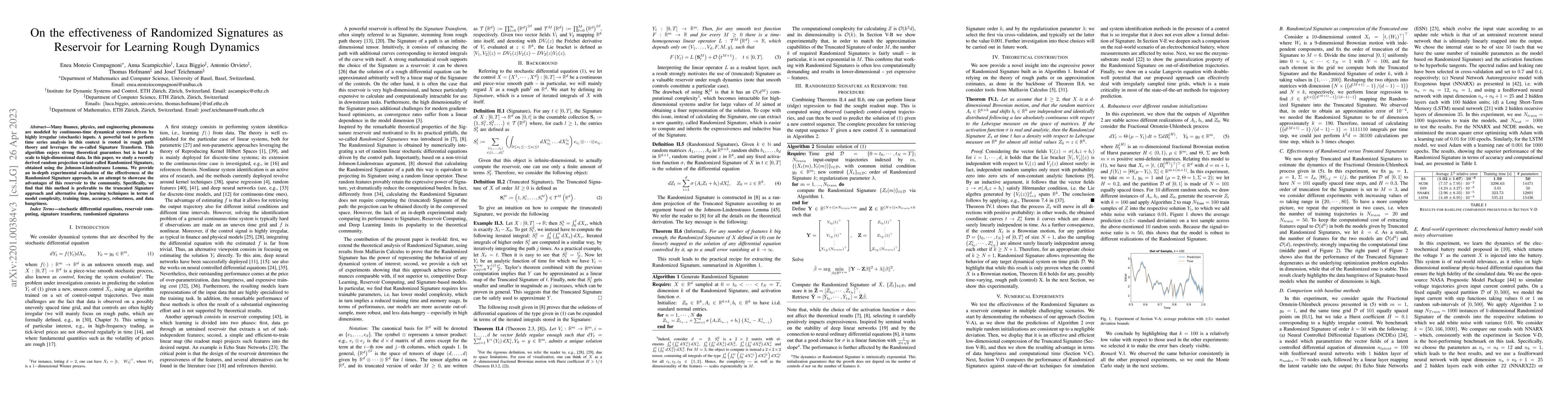

We present convincing empirical results on the application of Randomized Signature Methods for non-linear, non-parametric drift estimation for a multi-variate financial market. Even though drift est...

Generalized Feller theory provides an important analog to Feller theory beyond locally compact state spaces. This is very useful for solutions of certain stochastic partial differential equations, M...

Introduced in the late 90s, the passport option gives its holder the right to trade in a market and receive any positive gain in the resulting traded account at maturity. Pricing the option amounts ...

The Path-Dependent Neural Jump Ordinary Differential Equation (PD-NJ-ODE) is a model for predicting continuous-time stochastic processes with irregular and incomplete observations. In particular, th...

We introduce so-called functional input neural networks defined on a possibly infinite dimensional weighted space with values also in a possibly infinite dimensional output space. To this end, we us...

Randomized neural networks (randomized NNs), where only the terminal layer's weights are optimized constitute a powerful model class to reduce computational time in training the neural network model...

Signature stochastic differential equations (SDEs) constitute a large class of stochastic processes, here driven by Brownian motions, whose characteristics are entire or real-analytic functions of t...

We consider an asymptotic robust growth problem under model uncertainty and in the presence of (non-Markovian) stochastic covariance. We fix two inputs representing the instantaneous covariance for ...

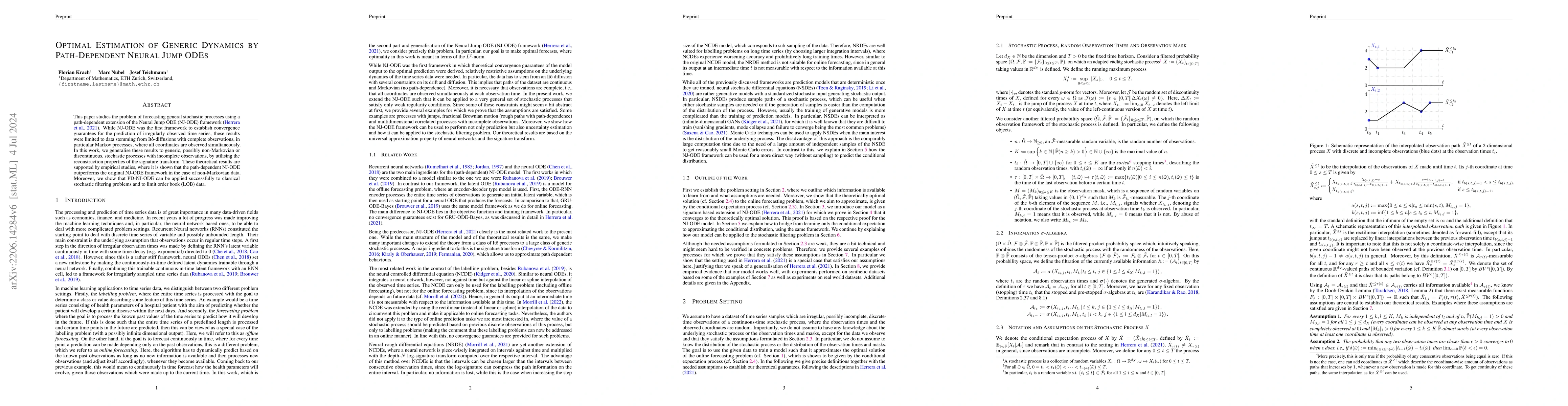

This paper studies the problem of forecasting general stochastic processes using a path-dependent extension of the Neural Jump ODE (NJ-ODE) framework \citep{herrera2021neural}. While NJ-ODE was the ...

Anomaly detection is the process of identifying abnormal instances or events in data sets which deviate from the norm significantly. In this study, we propose a signatures based machine learning alg...

Many finance, physics, and engineering phenomena are modeled by continuous-time dynamical systems driven by highly irregular (stochastic) inputs. A powerful tool to perform time series analysis in t...

In practice, multi-task learning (through learning features shared among tasks) is an essential property of deep neural networks (NNs). While infinite-width limits of NNs can provide good intuition ...

This paper presents the benefits of using randomized neural networks instead of standard basis functions or deep neural networks to approximate the solutions of optimal stopping problems. The key id...

We show that every $\mathbb{R}^d$-valued Sobolev path with regularity $\alpha$ and integrability $p$ can be lifted to a Sobolev rough path provided $\alpha < 1/p<1/3$. The novelty of our approach is...

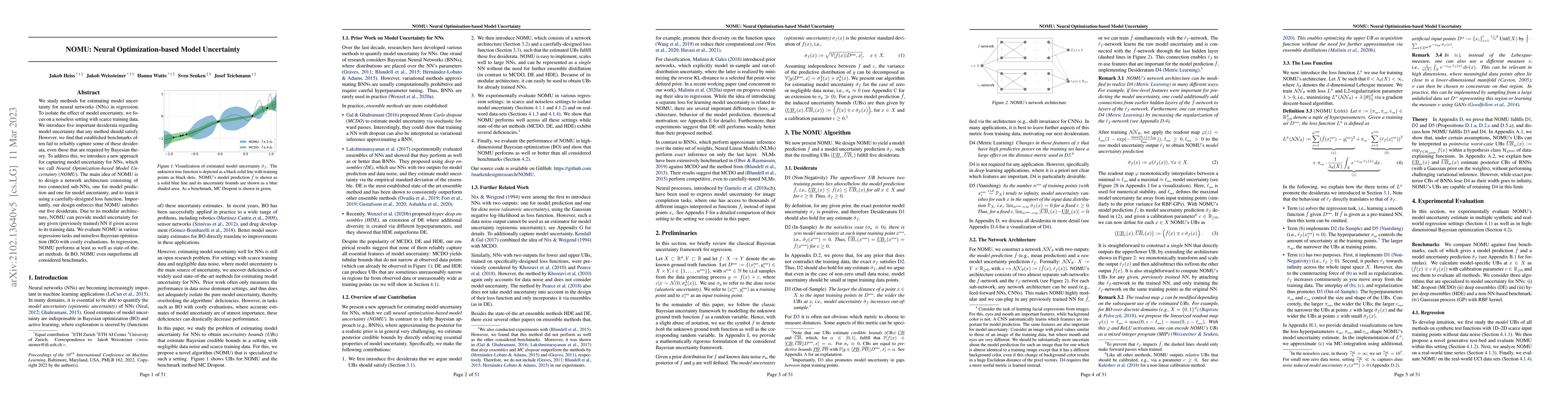

We study methods for estimating model uncertainty for neural networks (NNs) in regression. To isolate the effect of model uncertainty, we focus on a noiseless setting with scarce training data. We i...

To the best of our knowledge, the application of deep learning in the field of quantitative risk management is still a relatively recent phenomenon. In this article, we utilize techniques inspired b...

We investigate the performance of the Deep Hedging framework under training paths beyond the (finite dimensional) Markovian setup. In particular we analyse the hedging performance of the original ar...

A new explanation of geometric nature of the reservoir computing phenomenon is presented. Reservoir computing is understood in the literature as the possibility of approximating input/output systems...

To the best of our knowledge, the application of deep learning in the field of quantitative risk management is still a relatively recent phenomenon. This article presents the key notions of Deep Ass...

The Kyle model describes how an equilibrium of order sizes and security prices naturally arises between a trader with insider information and the price providing market maker as they interact throug...

In 2002, Benjamin Jourdain and Claude Martini discovered that for a class of payoff functions, the pricing problem for American options can be reduced to pricing of European options for an appropria...

Consistent Recalibration models (CRC) have been introduced to capture in necessary generality the dynamic features of term structures of derivatives' prices. Several approaches have been suggested t...

We introduce the space of rough paths with Sobolev regularity and the corresponding concept of controlled Sobolev paths. Based on these notions, we study rough path integration and rough differentia...

The robust PCA of covariance matrices plays an essential role when isolating key explanatory features. The currently available methods for performing such a low-rank plus sparse decomposition are ma...

The Lipschitz constant is an important quantity that arises in analysing the convergence of gradient-based optimization methods. It is generally unclear how to estimate the Lipschitz constant of a c...

This article introduces a new mathematical concept of illiquidity that goes hand in hand with credit risk. The concept is not volume- but constraint-based, i.e., certain assets cannot be shorted and...

We consider a financial market with zero-coupon bonds that are exposed to credit and liquidity risk. We revisit the famous Jarrow & Turnbull setting in order to account for these two intricately int...

In this paper, we consider one dimensional (shallow) ReLU neural networks in which weights are chosen randomly and only the terminal layer is trained. First, we mathematically show that for such net...

We consider stochastic partial differential equations appearing as Markovian lifts of matrix valued (affine) Volterra type processes from the point of view of the generalized Feller property (see e....

We show that every $\mathbb{R}^d$-valued Sobolev path with regularity $\alpha$ and integrability $p$ can be lifted to a Sobolev rough path in the sense of T. Lyons provided $\alpha >1/p>0$. Moreover...

The canonical generalizations of two classical norms on Besov spaces are shown to be equivalent even in the case of non-linear Besov spaces, that is, function spaces consisting of functions taking v...

The Path-dependent Neural Jump ODE (PD-NJ-ODE) is a model for online prediction of generic (possibly non-Markovian) stochastic processes with irregular (in time) and potentially incomplete (with respe...

Controlled ordinary differential equations driven by continuous bounded variation curves can be considered a continuous time analogue of recurrent neural networks for the construction of expressive fe...

We identify various classes of neural networks that are able to approximate continuous functions locally uniformly subject to fixed global linear growth constraints. For such neural networks the assoc...

We analyze an algorithm to numerically solve the mean-field optimal control problems by approximating the optimal feedback controls using neural networks with problem specific architectures. We approx...

We investigate the existence of a robust, i.e., continuous, representation of the conditional distribution in a stochastic filtering model for multidimensional correlated jump-diffusions. Even in the ...

Key global challenges of our times are characterized by complex interdependencies and can only be effectively addressed through an integrated, participatory effort. Conventional risk analysis framewor...

As the mathematical capabilities of large language models (LLMs) improve, it becomes increasingly important to evaluate their performance on research-level tasks at the frontier of mathematical knowle...

Detecting anomalies in irregularly sampled multi-variate time-series is challenging, especially in data-scarce settings. Here we introduce an anomaly detection framework for irregularly sampled time-s...

In this work, we explore how Neural Jump ODEs (NJODEs) can be used as generative models for It\^o processes. Given (discrete observations of) samples of a fixed underlying It\^o process, the NJODE fra...

Drifts of asset returns are notoriously difficult to model accurately and, yet, trading strategies obtained from portfolio optimization are very sensitive to them. To mitigate this well-known phenomen...

We study post-calibration uncertainty for trained ensembles of classifiers. Specifically, we consider both aleatoric (label noise) and epistemic (model) uncertainty. Among the most popular and widely ...

We generalize the universal approximation theorem for functional input neural networks (FNN) to differentiable maps by including the approximation of the derivatives. A FNN maps the input from a possi...