Academic Profile

Statistics

Similar Authors

Papers on arXiv

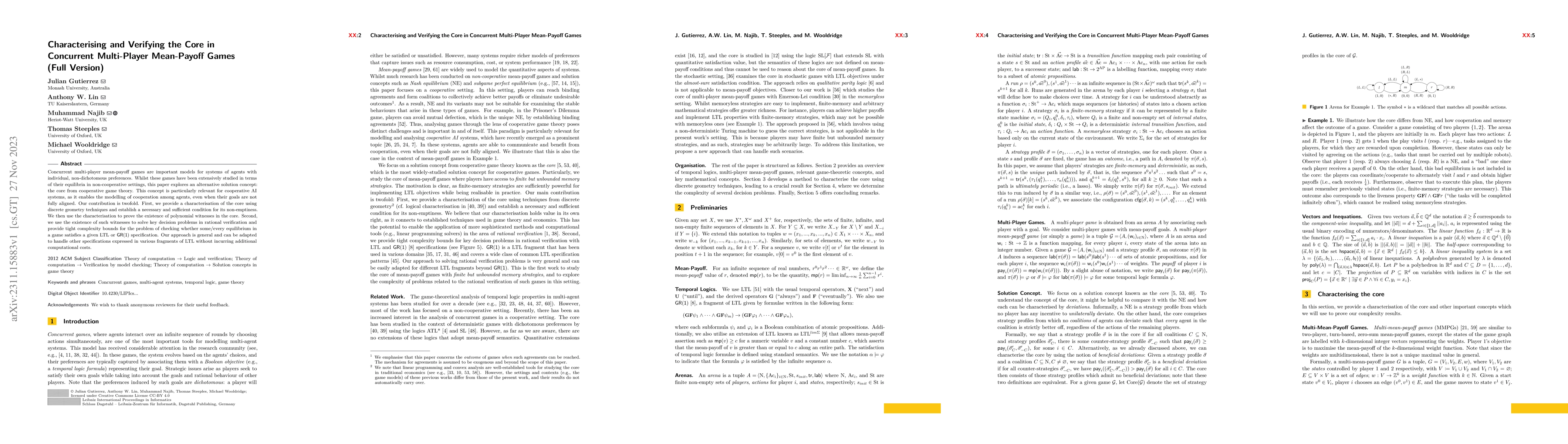

Concurrent multi-player mean-payoff games are important models for systems of agents with individual, non-dichotomous preferences. Whilst these games have been extensively studied in terms of their ...

We consider the problem of incentivising desirable behaviours in multi-agent systems by way of taxation schemes. Our study employs the concurrent games model: in this model, each agent is primarily ...

In game theory, mechanism design is concerned with the design of incentives so that a desired outcome of the game can be achieved. In this paper, we explore the concept of equilibrium design, where ...

We propose a machine learning method to solve a mean-field game price formation model with common noise. This involves determining the price of a commodity traded among rational agents subject to a ...

We introduce and study a computational version of the principal-agent problem -- a classic problem in Economics that arises when a principal desires to contract an agent to carry out some task, but ...

We introduce a natural variant of weighted voting games, which we refer to as k-Prize Weighted Voting Games. Such games consist of n players with weights, and k prizes, of possibly differing values....

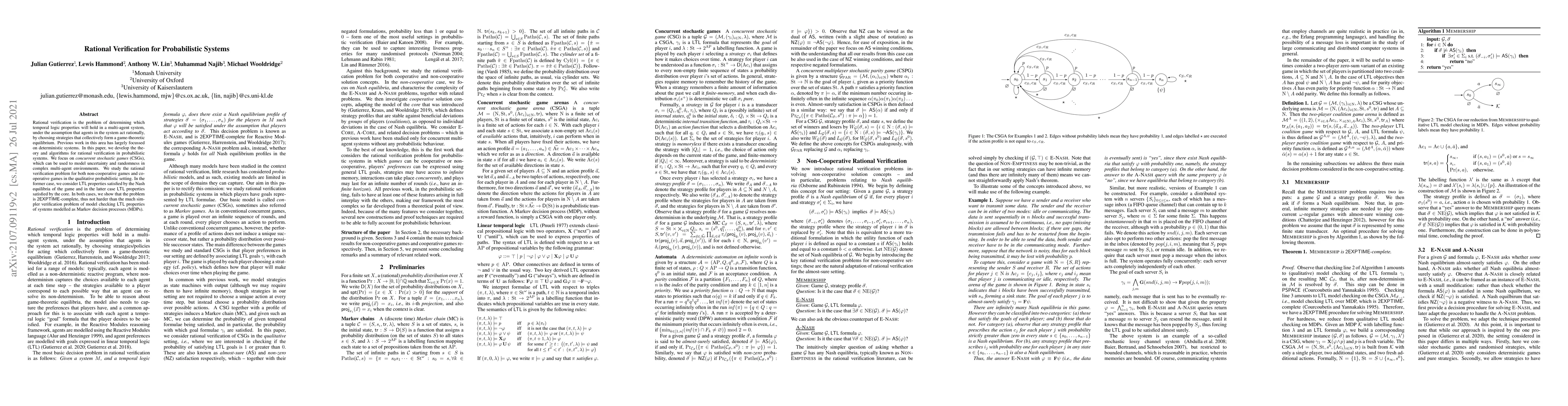

In rational verification, the aim is to verify which temporal logic properties will obtain in a multi-agent system, under the assumption that agents ("players") in the system choose strategies for a...

Rational verification refers to the problem of checking which temporal logic properties hold of a concurrent multiagent system, under the assumption that agents in the system choose strategies that ...

We consider the mean-field game price formation model introduced by Gomes and Sa\'ude. In this MFG model, agents trade a commodity whose supply can be deterministic or stochastic. Agents maximize pr...

In this paper, we study a class of first-order mean-field games (MFGs) that model price formation. Using Poincar{\'e} Lemma, we eliminate one of the equations and obtain a variational problem for a ...

We study the connection between the Aubry-Mather theory and a mean-field game (MFG) price-formation model. We introduce a framework for Mather measures that is suited for constrained time-dependent ...

We consider a market where a finite number of players trade an asset whose supply is a stochastic process. The price formation problem consists of finding a price process that ensures that when agen...

Rational verification is the problem of determining which temporal logic properties will hold in a multi-agent system, under the assumption that agents in the system act rationally, by choosing stra...

In game theory, mechanism design is concerned with the design of incentives so that a desired outcome of the game can be achieved. In this paper, we study the design of incentives so that a desirabl...

In this paper, we study the problem of learning to satisfy temporal logic specifications with a group of agents in an unknown environment, which may exhibit probabilistic behaviour. From a learning ...

Linear Dynamic Logic on finite traces LDLf is a powerful logic for reasoning about the behaviour of concurrent and multi-agent systems. In this paper, we investigate techniques for both the charac...

The overall aim of our research is to develop techniques to reason about the equilibrium properties of multi-agent systems. We model multi-agent systems as concurrent games, in which each player is ...

In the context of multi-agent systems, the rational verification problem is concerned with checking which temporal logic properties will hold in a system when its constituent agents are assumed to b...

In this paper, we propose a mean-field game model for the price formation of a commodity whose production is subjected to random fluctuations. The model generalizes existing deterministic price form...

Game theory provides a well-established framework for the analysis of concurrent and multi-agent systems. The basic idea is that concurrent processes (agents) can be understood as corresponding to p...

We evaluate a co-evolutionary calibration framework for the Heston model in which a genetic algorithm (GA) over parameters is coupled to an evolving neural inverse map from option surfaces to paramete...

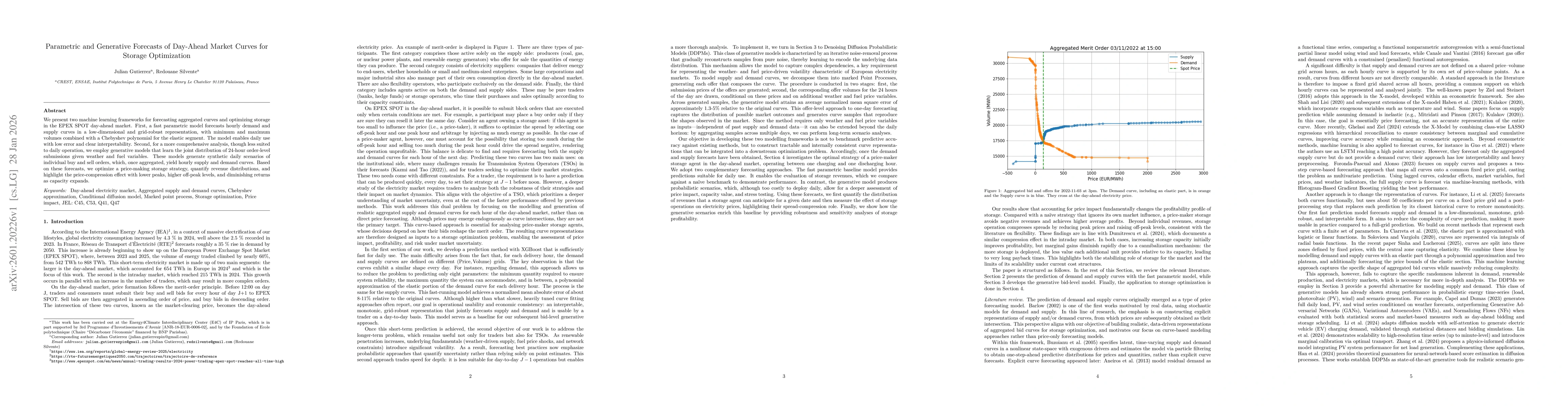

We present two machine learning frameworks for forecasting aggregated curves and optimizing storage in the EPEX SPOT day-ahead market. First, a fast parametric model forecasts hourly demand and supply...