Academic Profile

Statistics

Similar Authors

Papers on arXiv

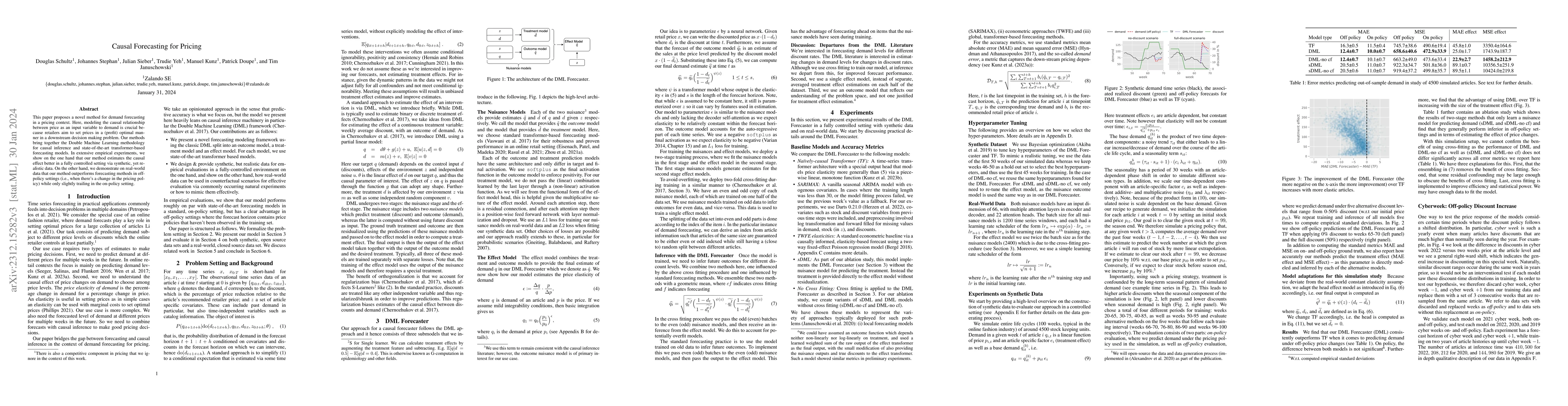

This paper proposes a novel method for demand forecasting in a pricing context. Here, modeling the causal relationship between price as an input variable to demand is crucial because retailers aim t...

Demand forecasting in the online fashion industry is particularly amendable to global, data-driven forecasting models because of the industry's set of particular challenges. These include the volume...

We show that deep belief networks with binary hidden units can approximate any multivariate probability density under very mild integrability requirements on the parental density of the visible node...

We investigate the stationary measure $\pi$ of SDEs driven by additive fractional noise with any Hurst parameter and establish that $\pi$ admits a smooth Lebesgue density obeying both Gaussian-type ...

Our first result is a stochastic sewing lemma with quantitative estimates for mild incremental processes, with which we study SPDEs driven by fractional Brownian motions in a random environment. We ...

We prove an enhanced limit theorem for additive functionals of a multi-dimensional Volterra process $(y_t)_{t\geq 0}$ in the rough path topology. As an application, we establish weak convergence as ...

We prove a fractional averaging principle for interacting slow-fast systems. The mode of convergence is in H\"older norm in probability. The main technical result is a quenched ergodic theorem on th...

We give a direct alternative proof of an area law for the entanglement entropy of the ground state of disordered oscillator systems---a result due to Nachtergaele, Sims and Stolz. Instead of studyin...

We consider the solution of an additive fractional stochastic differential equation (SDE) and, leveraging continuous observations of the process, introduce a methodology for estimating its stationary ...