Academic Profile

Statistics

Similar Authors

Papers on arXiv

We introduce and study geometric Bass martingales. Bass martingales were introduced in \cite{Ba83} and studied recently in a series of works, including \cite{BaBeHuKa20,BaBeScTs23}, where they appea...

Defining a divergence between the laws of continuous martingales is a delicate task, owing to the fact that these laws tend to be singular to each other. An important idea, put forward by N. Gantert...

An interesting question in the field of martingale optimal transport, is to determine the martingale with prescribed initial and terminal marginals which is most correlated to Brownian motion. Under...

In classical optimal transport, the contributions of Benamou$-$Brenier and McCann regarding the time-dependent version of the problem are cornerstones of the field and form the basis for a variety o...

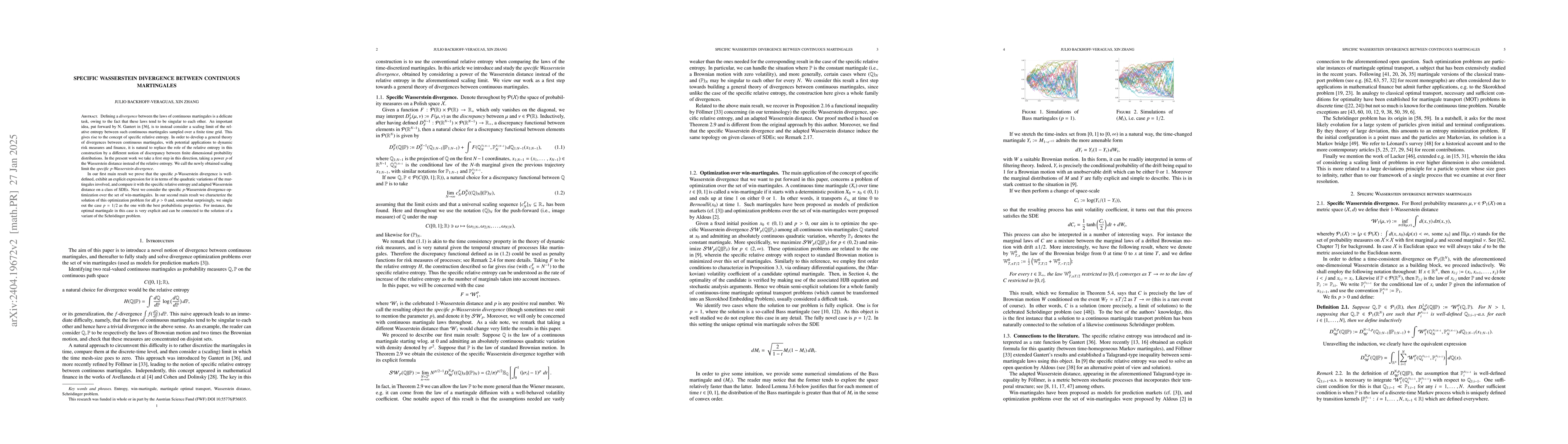

Motivated by a problem posed by Aldous, our goal is to find the maximal-entropy win-martingale: In a sports game between two teams, the chance the home team wins is initially $x_0 \in (0,1)$ and f...

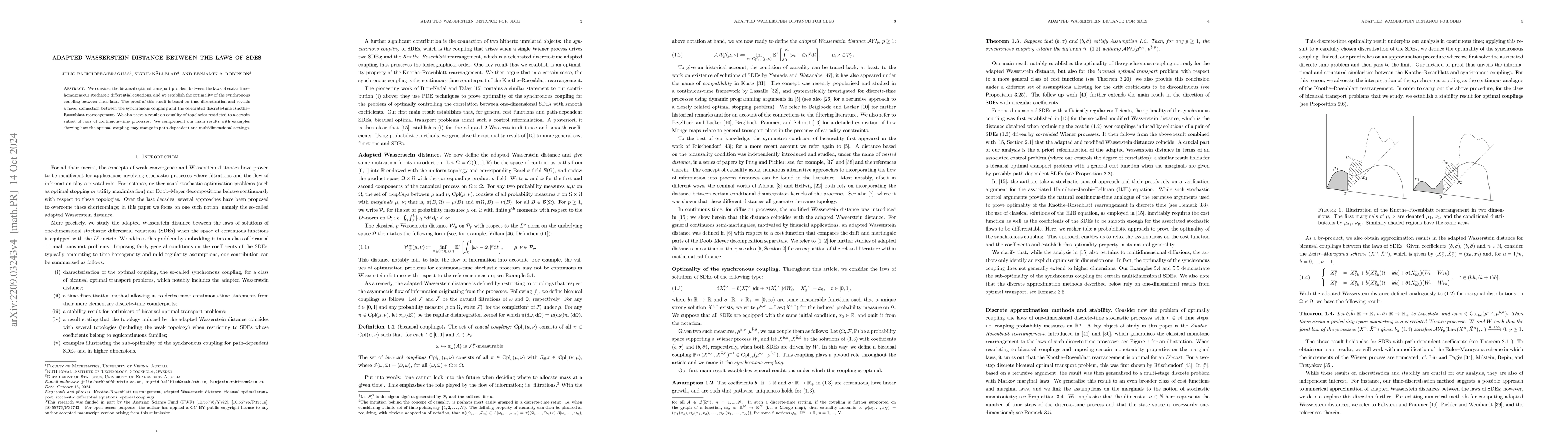

We consider the adapted optimal transport problem between the laws of Markovian stochastic differential equations (SDE) and establish the optimality of the synchronous coupling between these laws. T...

The specific relative entropy, introduced by N. Gantert, allows to quantify the discrepancy between the laws of potentially mutually singular measures. It appears naturally as the large deviations r...

We consider a large population dynamic game in discrete time where players are characterized by time-evolving types. It is a natural assumption that the players' actions cannot anticipate future val...

We present and study a novel algorithm for the computation of 2-Wasserstein population barycenters of absolutely continuous probability measures on Euclidean space. The proposed method can be seen a...

We consider the problem of minimizing a generalized relative entropy, with respect to a reference diffusion law, over the set of path-measures with fully prescribed marginal distributions. When deal...

We consider a large population dynamic game in discrete time. The peculiarity of the game is that players are characterized by time-evolving types, and so reasonably their actions should not anticip...

We consider a general framework of optimal mechanism design under adverse selection and ambiguity about the type distribution of agents. We prove the existence of optimal mechanisms under minimal as...

A number of researchers have introduced topological structures on the set of laws of stochastic processes. A unifying goal of these authors is to strengthen the usual weak topology in order to adequ...

Under mild regularity assumptions, the transport problem is stable in the following sense: if a sequence of optimal transport plans $\pi_1, \pi_2, \ldots$ converges weakly to a transport plan $\pi$,...

Assume that an agent models a financial asset through a measure Q with the goal to price / hedge some derivative or optimize some expected utility. Even if the model Q is chosen in the most skilful ...

We introduce and study a novel model-selection strategy for Bayesian learning, based on optimal transport, along with its associated predictive posterior law: the Wasserstein population barycenter o...

Given $\mu$ and $\nu$, probability measures on $\mathbb R^d$ in convex order, a Bass martingale is arguably the most natural martingale starting with law $\mu$ and finishing with law $\nu$. Indeed, th...