Academic Profile

Statistics

Similar Authors

Papers on arXiv

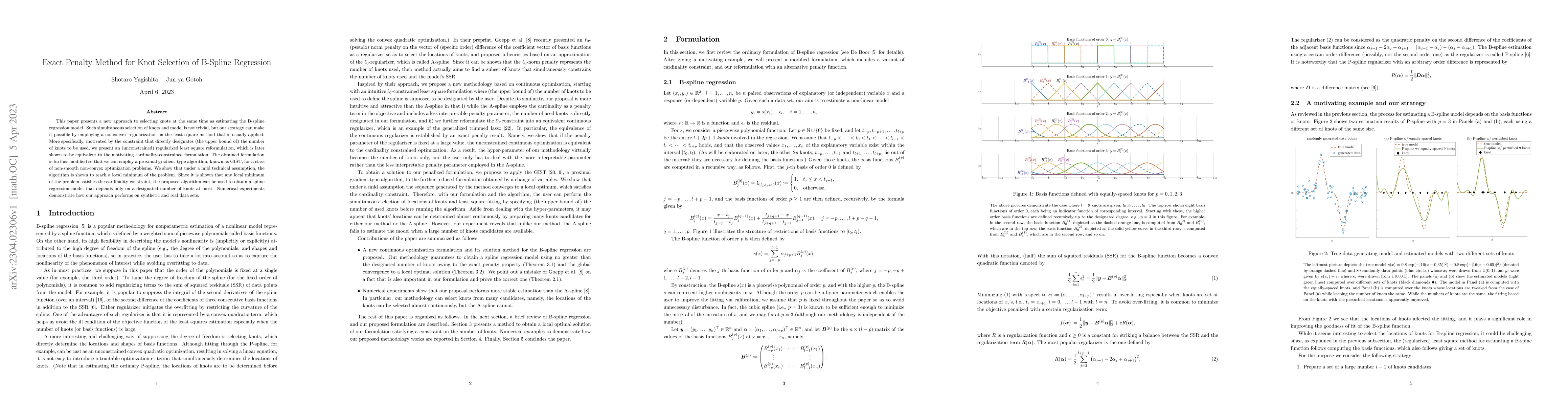

This paper presents a new approach to selecting knots at the same time as estimating the B-spline regression model. Such simultaneous selection of knots and model is not trivial, but our strategy ca...

This paper studies the properties of d-stationary points of the trimmed lasso (Luo et al., 2013, Huang et al., 2015, and Gotoh et al., 2018) and the composite optimization problem with the truncated...

While solutions of Distributionally Robust Optimization (DRO) problems can sometimes have a higher out-of-sample expected reward than the Sample Average Approximation (SAA), there is no guarantee. I...

We introduce the notion of Worst-Case Sensitivity, defined as the worst-case rate of increase in the expected cost of a Distributionally Robust Optimization (DRO) model when the size of the uncertai...

This paper conducts a comparative study of proximal gradient methods (PGMs) and proximal DC algorithms (PDCAs) for sparse regression problems which can be cast as Difference-of-two-Convex-functions ...

The EM (Expectation-Maximization) algorithm is regarded as an MM (Majorization-Minimization) algorithm for maximum likelihood estimation of statistical models. Expanding this view, this paper demonstr...

Distributionally Robust Optimization (DRO) is a worst-case approach to decision making when there is model uncertainty. Though formulated as a single-objective problem, we show that it is intrinsicall...

We introduce the notion of worst-case posterior and worst-case likelihood sensitivity. These measure, respectively, the sensitivity of the expected cost to worst-case perturbations of the posterior di...

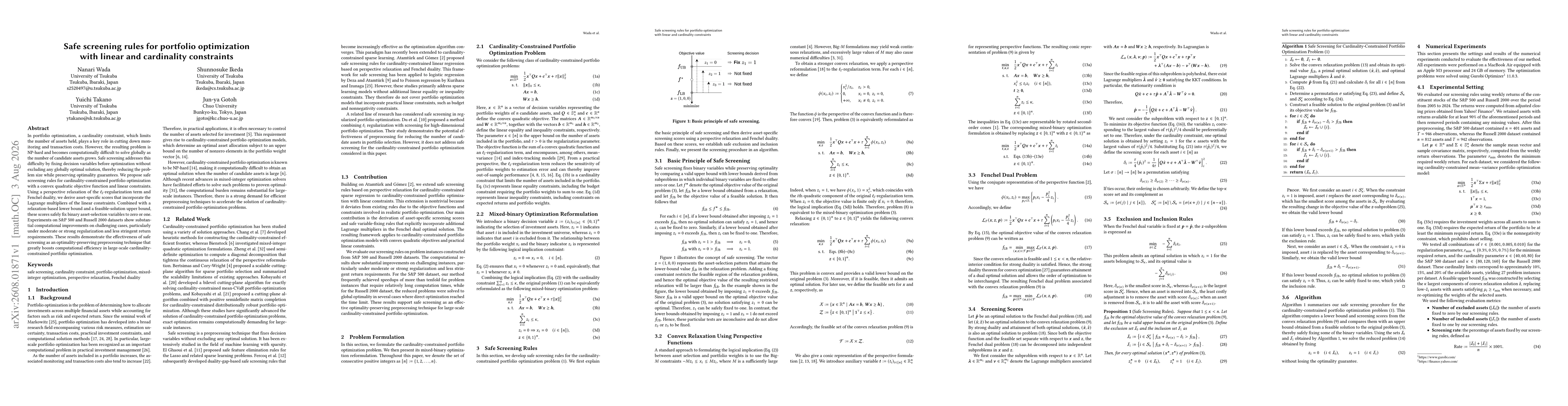

In portfolio optimization, a cardinality constraint, which limits the number of assets held, plays a key role in cutting down monitoring and transaction costs. However, the resulting problem is NP-har...