Academic Profile

Statistics

Similar Authors

Papers on arXiv

Predictive posterior densities (PPDs) are of interest in approximate Bayesian inference. Typically, these are estimated by simple Monte Carlo (MC) averages using samples from the approximate posteri...

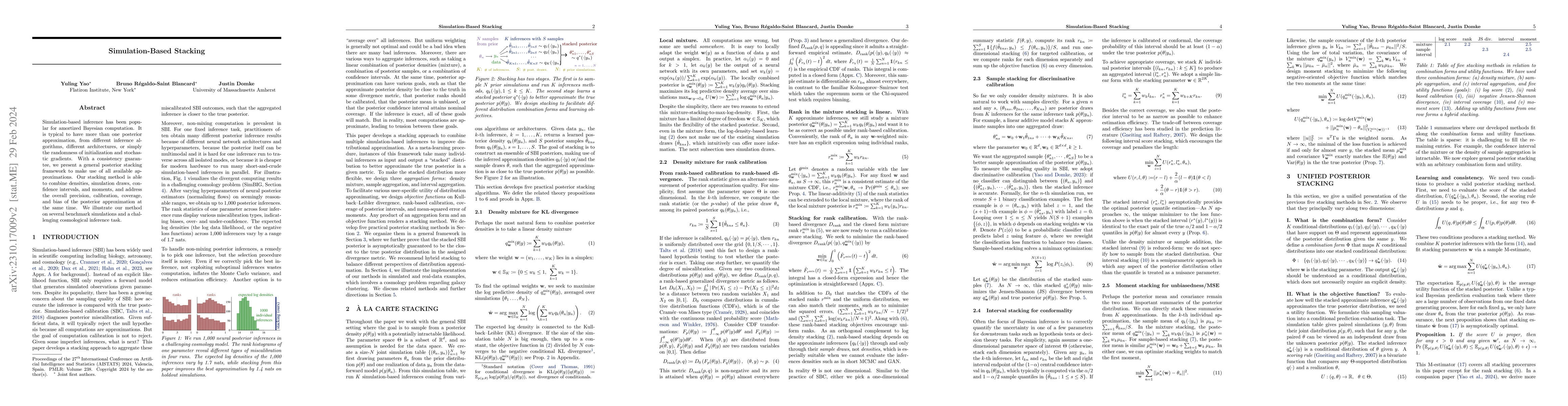

Simulation-based inference has been popular for amortized Bayesian computation. It is typical to have more than one posterior approximation, from different inference algorithms, different architectu...

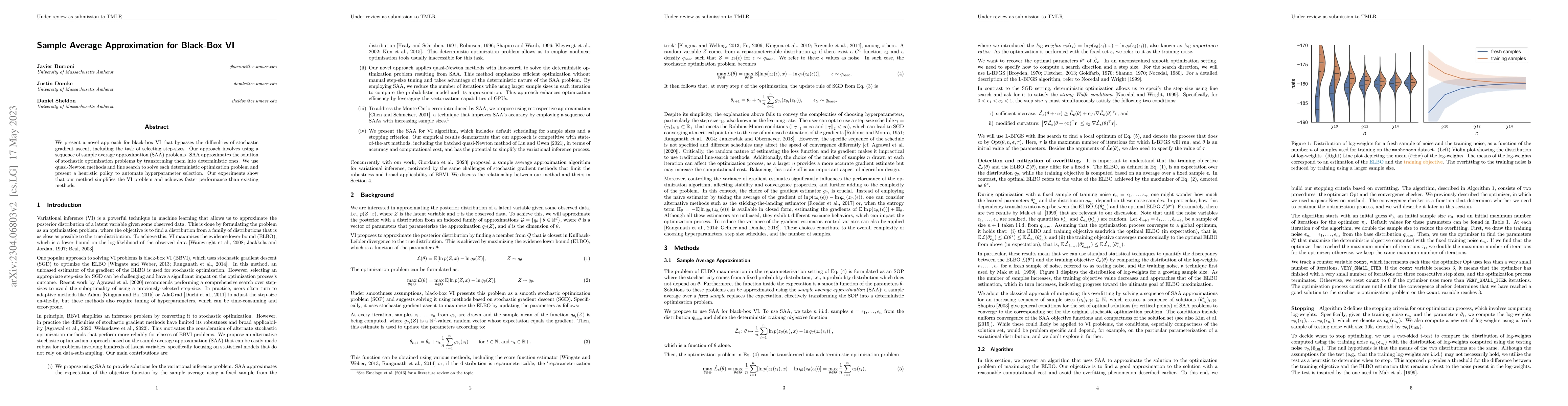

Black-box variational inference is widely used in situations where there is no proof that its stochastic optimization succeeds. We suggest this is due to a theoretical gap in existing stochastic opt...

To check the accuracy of Bayesian computations, it is common to use rank-based simulation-based calibration (SBC). However, SBC has drawbacks: The test statistic is somewhat ad-hoc, interactions are...

We present a novel approach for black-box VI that bypasses the difficulties of stochastic gradient ascent, including the task of selecting step-sizes. Our approach involves using a sequence of sampl...

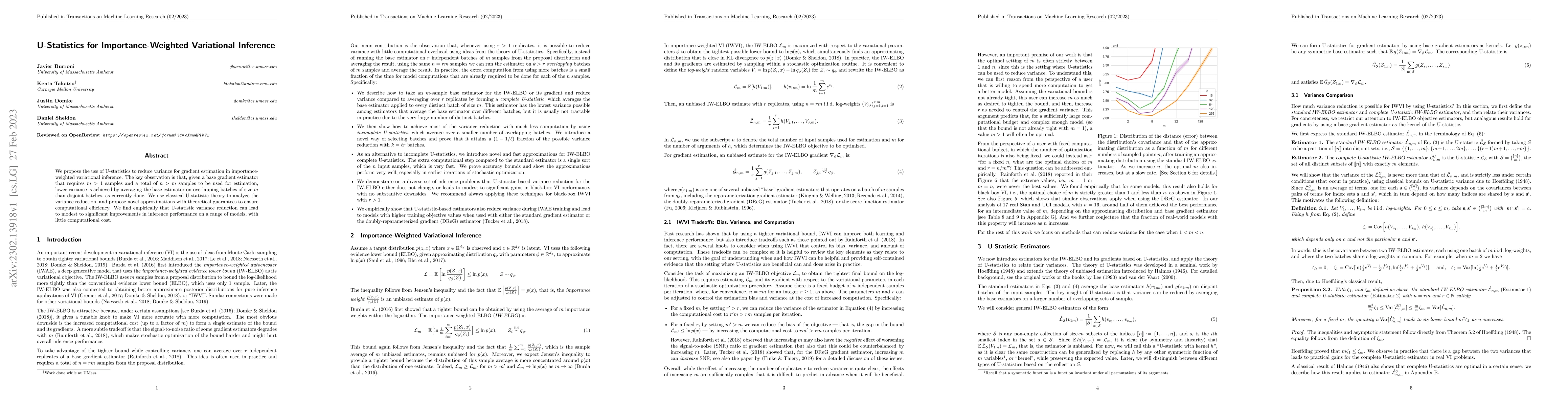

We propose the use of U-statistics to reduce variance for gradient estimation in importance-weighted variational inference. The key observation is that, given a base gradient estimator that requires...

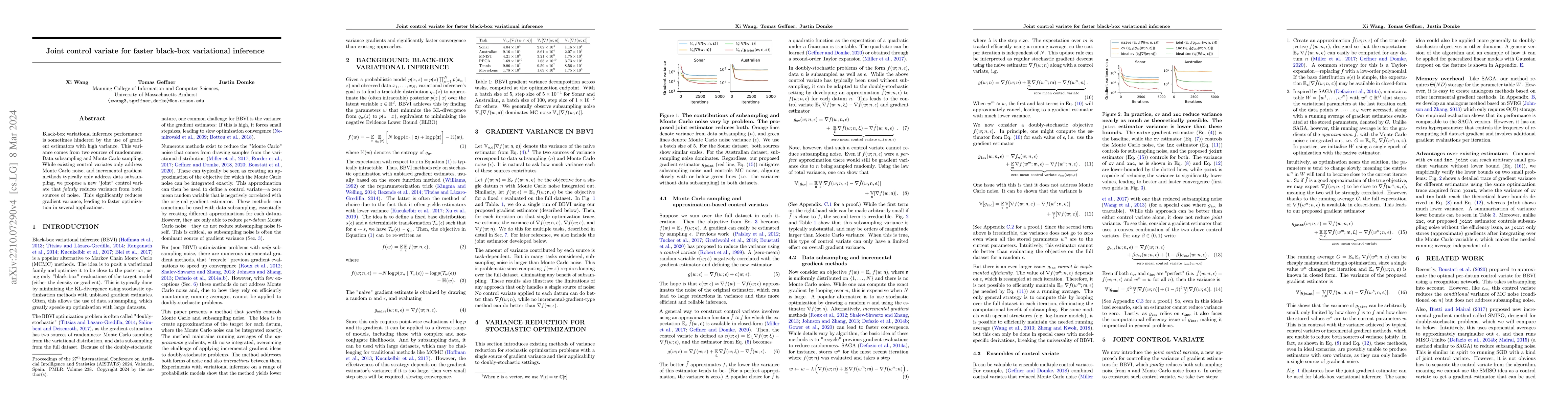

Black-box variational inference performance is sometimes hindered by the use of gradient estimators with high variance. This variance comes from two sources of randomness: Data subsampling and Monte...

Many methods that build powerful variational distributions based on unadjusted Langevin transitions exist. Most of these were developed using a wide range of different approaches and techniques. Unf...

Hierarchical models represent a challenging setting for inference algorithms. MCMC methods struggle to scale to large models with many local variables and observations, and variational inference (VI...

It is difficult to use subsampling with variational inference in hierarchical models since the number of local latent variables scales with the dataset. Thus, inference in hierarchical models remain...

Variational inference for state space models (SSMs) is known to be hard in general. Recent works focus on deriving variational objectives for SSMs from unbiased sequential Monte Carlo estimators. We...

Given an unnormalized target distribution we want to obtain approximate samples from it and a tight lower bound on its (log) normalization constant log Z. Annealed Importance Sampling (AIS) with Ham...

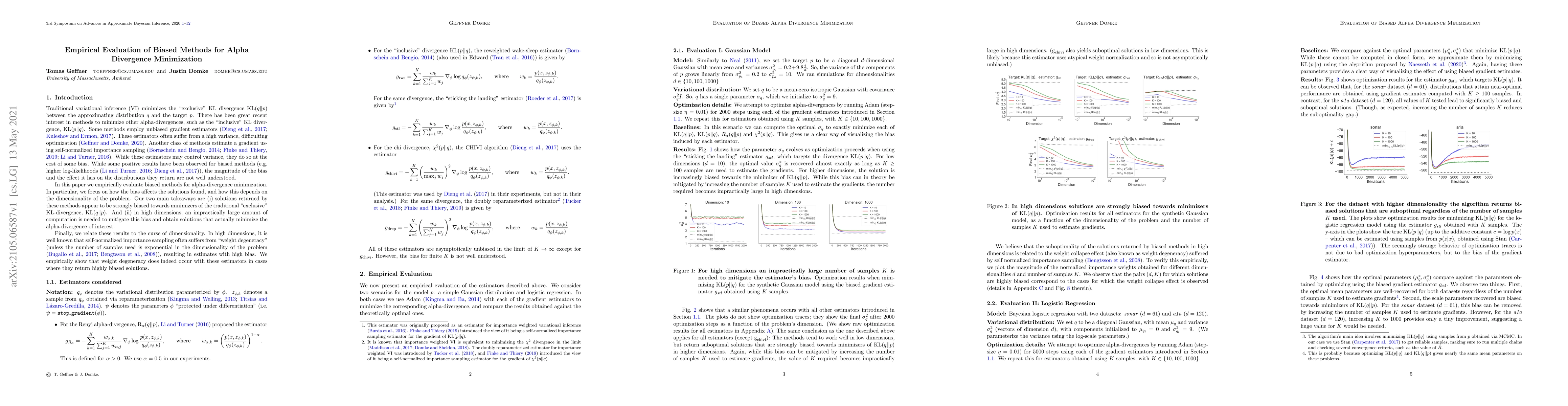

In this paper we empirically evaluate biased methods for alpha-divergence minimization. In particular, we focus on how the bias affects the final solutions found, and how this depends on the dimensi...

It is important to estimate the errors of probabilistic inference algorithms. Existing diagnostics for Markov chain Monte Carlo methods assume inference is asymptotically exact, and are not appropri...

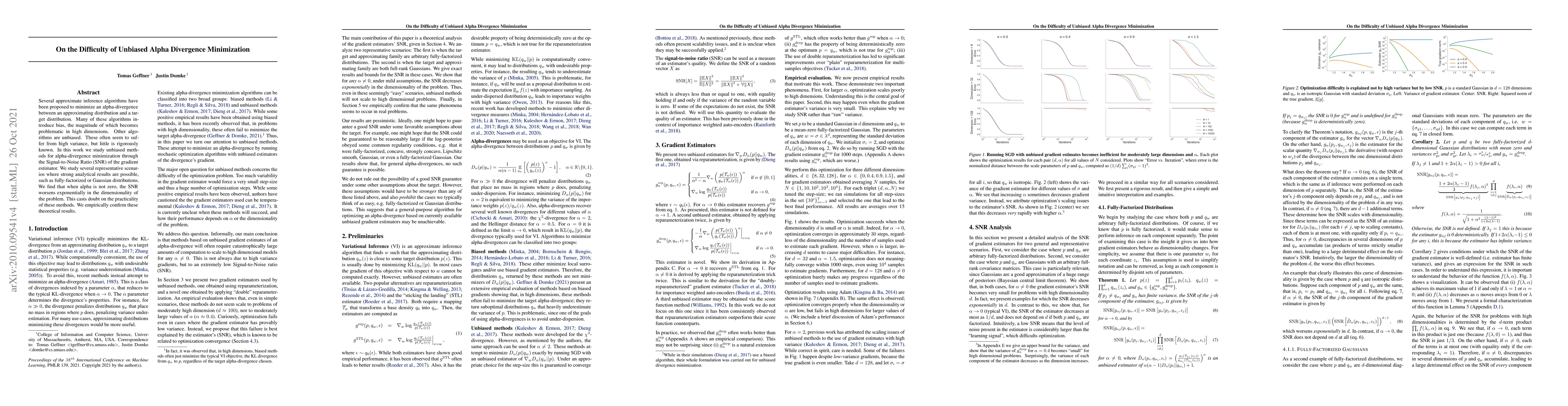

Several approximate inference algorithms have been proposed to minimize an alpha-divergence between an approximating distribution and a target distribution. Many of these algorithms introduce bias, ...

Flexible variational distributions improve variational inference but are harder to optimize. In this work we present a control variate that is applicable for any reparameterizable distribution with ...

Maximum likelihood learning with exponential families leads to moment-matching of the sufficient statistics, a classic result. This can be generalized to conditional exponential families and/or when...

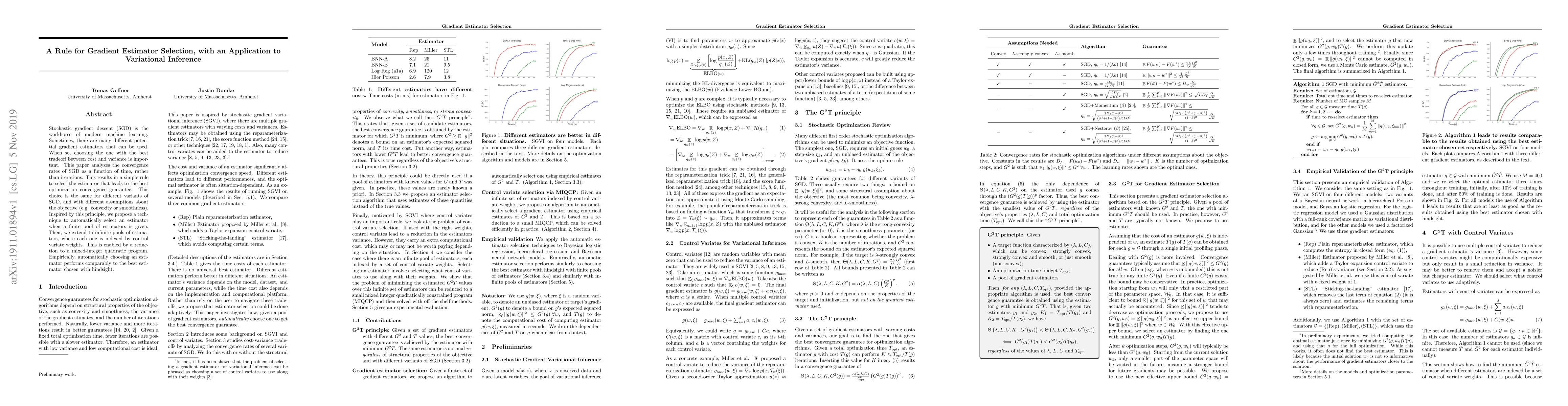

Stochastic gradient descent (SGD) is the workhorse of modern machine learning. Sometimes, there are many different potential gradient estimators that can be used. When so, choosing the one with the ...

We study the effects of approximate inference on the performance of Thompson sampling in the $k$-armed bandit problems. Thompson sampling is a successful algorithm for online decision-making but req...

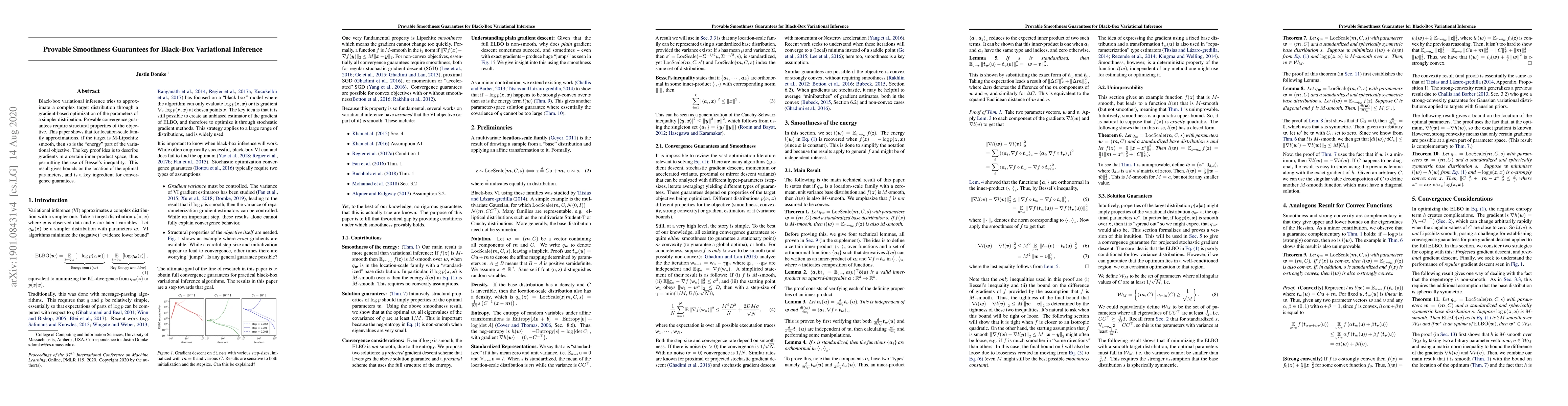

Black-box variational inference tries to approximate a complex target distribution though a gradient-based optimization of the parameters of a simpler distribution. Provable convergence guarantees r...

Variational inference is increasingly being addressed with stochastic optimization. In this setting, the gradient's variance plays a crucial role in the optimization procedure, since high variance g...

Bayesian reasoning in linear mixed-effects models (LMMs) is challenging and often requires advanced sampling techniques like Markov chain Monte Carlo (MCMC). A common approach is to write the model in...

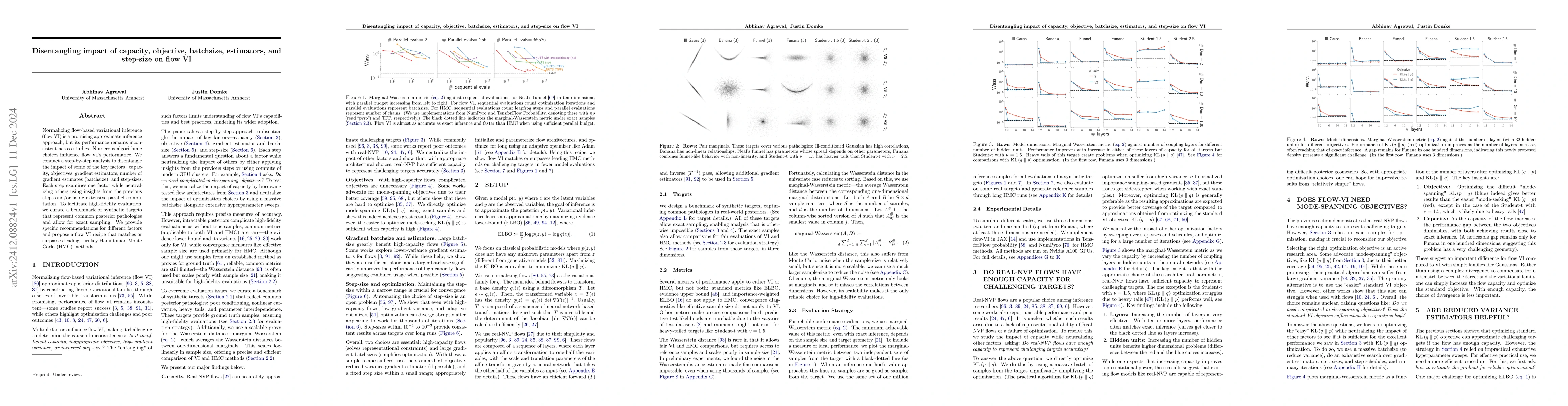

Normalizing flow-based variational inference (flow VI) is a promising approximate inference approach, but its performance remains inconsistent across studies. Numerous algorithmic choices influence fl...

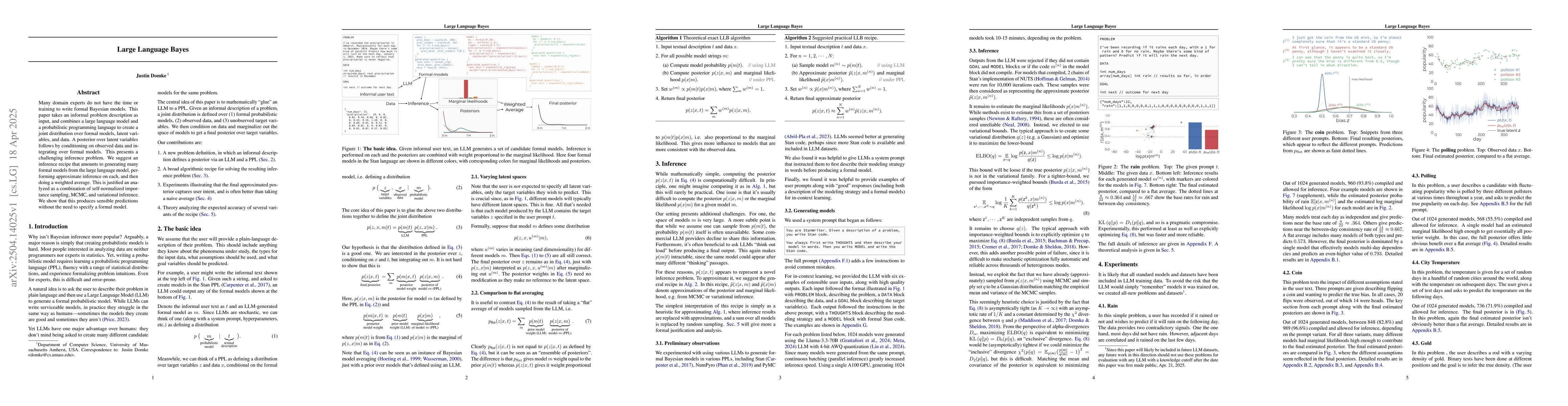

Many domain experts do not have the time or training to write formal Bayesian models. This paper takes an informal problem description as input, and combines a large language model and a probabilistic...

Variational inference often struggles with the posterior geometry exhibited by complex hierarchical Bayesian models. Recent advances in flow-based variational families and Variationally Inferred Param...

Amortized inference promises fast test-time Bayesian inference, but existing methods are inherently tied to fixed models. Extending amortization to unseen models typically requires retraining or costl...