Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper provides an introductory overview of how one may employ importance sampling effectively as a tool for solving stochastic optimization formulations incorporating tail risk measures such as...

Given data on the choices made by consumers for different offer sets, a key challenge is to develop parsimonious models that describe and predict consumer choice behavior while being amenable to pre...

This paper investigates the use of retrospective approximation solution paradigm in solving risk-averse optimization problems effectively via importance sampling (IS). While IS serves as a prominent...

We consider statistical methods which invoke a min-max distributionally robust formulation to extract good out-of-sample performance in data-driven optimization and learning problems. Acknowledging ...

This paper considers Importance Sampling (IS) for the estimation of tail risks of a loss defined in terms of a sophisticated object such as a machine learning feature map or a mixed integer linear o...

We present a statistical testing framework to detect if a given machine learning classifier fails to satisfy a wide range of group fairness notions. The proposed test is a flexible, interpretable, a...

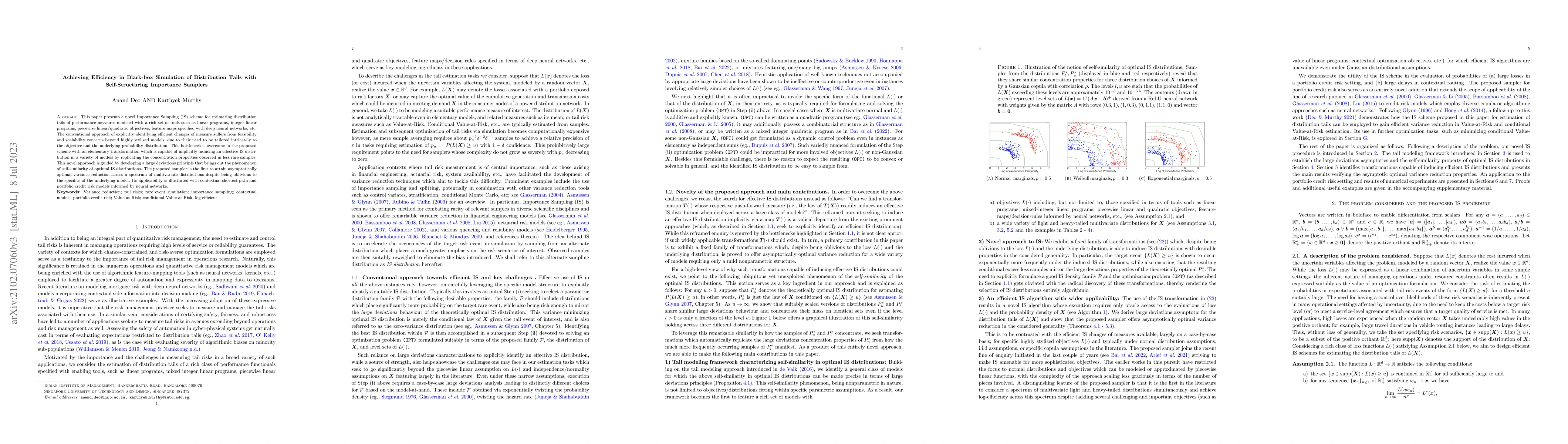

This paper presents a novel Importance Sampling (IS) scheme for estimating distribution tails of performance measures modeled with a rich set of tools such as linear programs, integer linear program...

Motivated by the prominence of Conditional Value-at-Risk (CVaR) as a measure for tail risk in settings affected by uncertainty, we develop a new formula for approximating CVaR based optimization obj...

Wasserstein distributionally robust optimization estimators are obtained as solutions of min-max problems in which the statistician selects a parameter minimizing the worst-case loss among all proba...

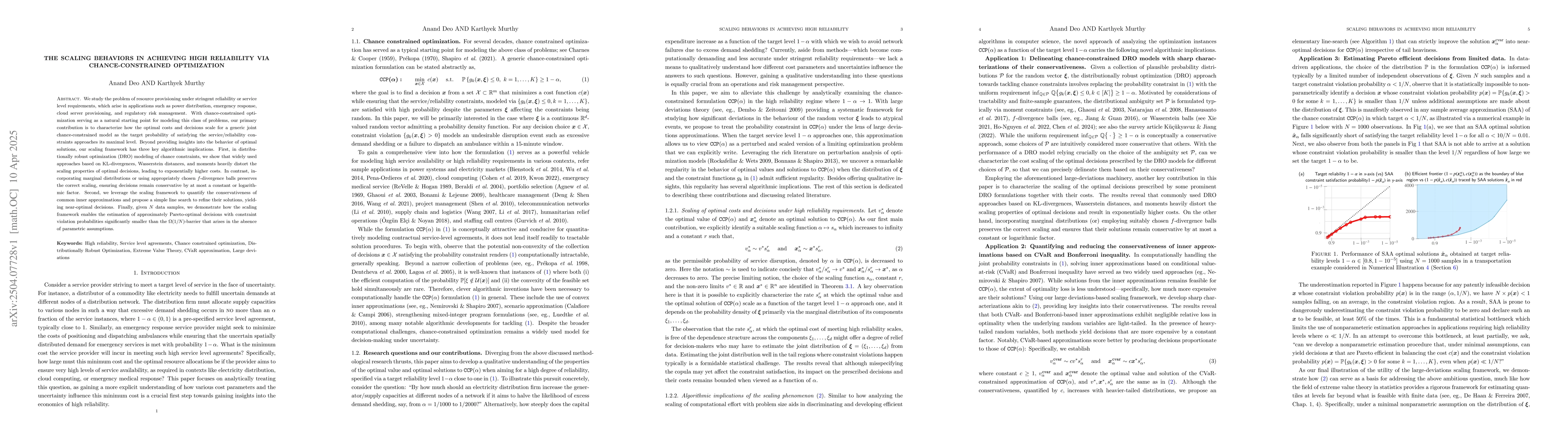

We study the problem of resource provisioning under stringent reliability or service level requirements, which arise in applications such as power distribution, emergency response, cloud server provis...

We study decision-making problems where data comprises points from a collection of binary polytopes, capturing aggregate information stemming from various combinatorial selection environments. We prop...

We study the i.i.d. $k$-selection prophet inequality problem, where a decision-maker sequentially observes $n$ independent nonnegative rewards and may accept at most $k$ of them without knowledge of f...