Academic Profile

Statistics

Similar Authors

Papers on arXiv

This paper develops a novel, fully automated forecast averaging scheme, which combines LASSO estimation method with Principal Component Averaging (PCA). LASSO-PCA (LPCA) explores a pool of predictio...

In this article, a novel identification test is proposed, which can be applied to parameteric models such as Mixture of Normal (MN) distributions, Markow Switching(MS), or Structural Autoregressive ...

The changes in electricity markets expose RES producers and electricity traders to various risks, among which the price and the volume risk play a very important role. In this research, a portfolio ...

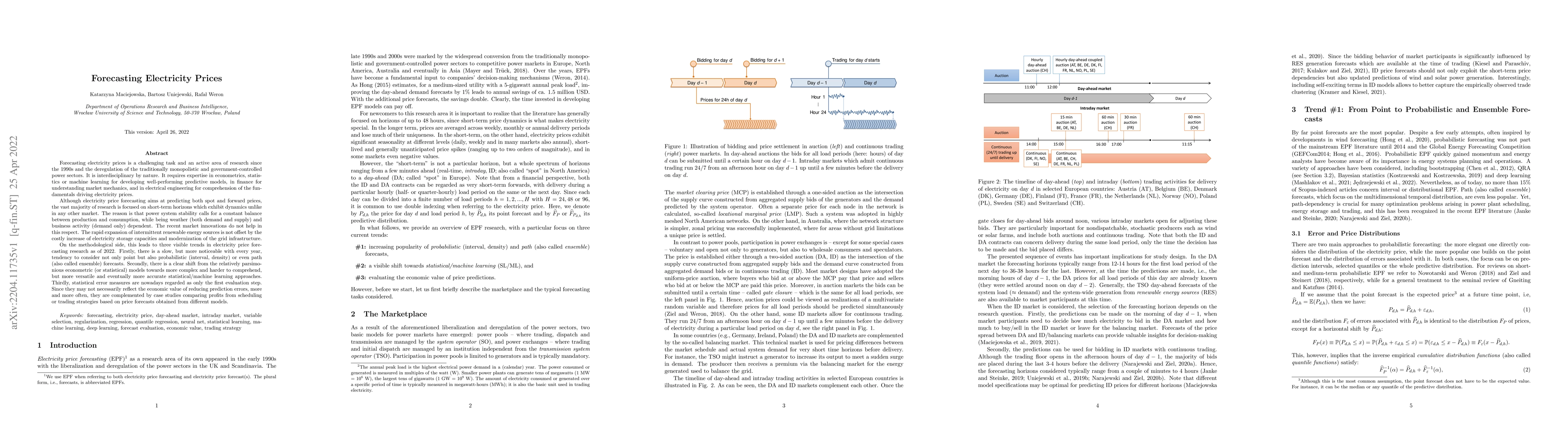

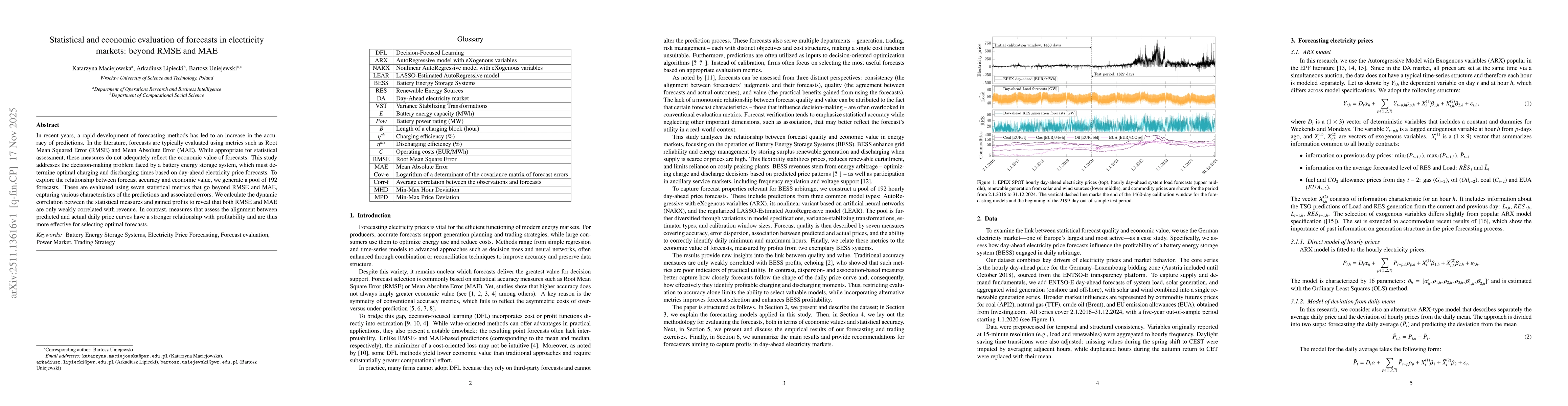

Forecasting electricity prices is a challenging task and an active area of research since the 1990s and the deregulation of the traditionally monopolistic and government-controlled power sectors. Al...

In this article, a multiple split method is proposed that enables construction of multidimensional probabilistic forecasts of a selected set of variables. The method uses repeated resampling to estima...

In recent years, a rapid development of forecasting methods has led to an increase in the accuracy of predictions. In the literature, forecasts are typically evaluated using metrics such as Root Mean ...

Battery energy storage systems (BESS) are expected to play an important role in electricity markets with increasing shares of renewable generation. While existing research has primarily focused on pri...